Once Inflation Starts, It Won’t Be Contained

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

Once Inflation Starts, It Won’t Be Contained

By Gael Sanchez Smith

Posted June 12, 2020

Introduction

The mainstream media has spent decades underplaying the risks of inflation, claiming that deflation is the most perilous thing that could ever happen in an economy. Amazingly, their propaganda has succeeded and most people have come to accept the ludicrous notion that falling prices of goods and services are an economic problem— for a detailed analysis of the fallacies of deflation see Jeff Booth’s, The Price of Tomorrow. Even today, as central banks around the world implement ever more unorthodox monetary policies such as asset purchases and negative interest rates, the public remains largely oblivious of the risks of inflation.

Searches for Inflation Worldwide

Searches for Inflation Worldwide

This article isn’t an attempt to forecast the exact set of circumstances that might give rise to inflation. Instead, it argues that the chief belief that gives fiat money value — namely, the expectation that central banks are capable and willing to preserve their currency’s purchasing power — is unwarranted. In the event of inflation, central banks won’t be able to preserve the value of fiat money for three reasons: The high level of private debt, the high level of public debt and the precariousness of central bank’s balance sheet.

Markets are forward looking, hence, as people come to realize that central banks can’t preserve the purchasing power of their currencies, we should expect a repudiation of State liabilities — fiat money and government bonds — and a move towards hyperbitcoinization.

The Value of Fiat Money

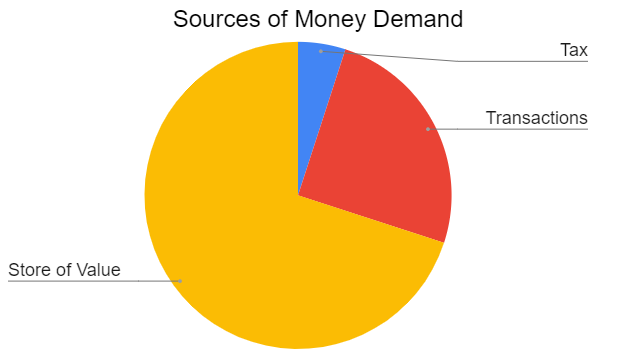

Fiat currencies are financial assets, more specifically they are liabilities issued by a nation’s central bank which we demand for three reasons:

- Tax Demand: The government mandates taxes be paid in the national currency. This is the smallest component of the total demand since it only exerts itself once a year.

- Store of Value (SOV) Demand: Fiat money is used as a highly liquid asset that promise to preserve its purchasing power — i.e. a store of value. This is the largest component of total demand and it is contingent upon the currency‘s price stability.

- Transaction Demand: We use fiat money as a medium of exchange to conduct commercial and private transactions. Transaction demand is closely tied to SOV demand; if the currency doesn’t have stable purchasing power, merchants will apply a high discount rate or will demand a more stable currency.

Illustration:Sources of Money Demand, Gael Sánchez Smith

Illustration:Sources of Money Demand, Gael Sánchez Smith

Chartalists mistakenly believe that the obligation to pay taxes a alone makes fiat money valuable. Of course, there is always a minimum level of Tax Demand since failure to comply with tax laws results in imprisonment, but most of money’s demand is derived from its use as a medium of exchange and a store of value. Consequently, the monetary powers of the State are much more limited than what Chartalists profess; a government can mandate taxes be paid in the national currency but it cannot impose its use as a store of value or a medium of exchange.

In other words, money is always and everywhere a market phenomenon. If a currency starts depreciating at a high rate, SOV demand will collapse and it won’t be used as a medium of exchange regardless of what the State decrees. We can see this reality play out today in countries like Argentina or Venezuela where, even though taxes are collected in the national currency, most transactions are conducted in dollars and value is stored in dollars, Bicoin, or gold.

The value of fiat money, like any other asset, depends not only of its demand but also of its supply. Central banks are very aware that if the supply of money exceeds its demand significantly, the currency will depreciate and its SOV demand will disappear. Hence, they present themselves as independent institutions that are are committed to fighting inflation and divorcing the supply of money from the governments financial needs. In the real world, central banks target 2% inflation and often collude with the government, but functioning monetary territories like Europe, Japan, or the U.S. have until now, shown sufficient restraint from printing their currencies to oblivion.

Central banks influence the supply of money by manipulating the interest rate: When they wish to increase supply, they lower the interest rate and when they wish to reduce the supply, the interest rate is increased (Stefanie von Jan explains the process in further detail here). If the supply of money increases above its demand or if demand falls below its supply (for example due to a loss of trust in the issuer) the currency will depreciate, its discount rate will spike — e.g. workers will sell their labor for 20 $ instead of 10$ in anticipation of inflation — and the Store of Value demand will fall creating an inflationary spiral. In this scenario, it is imperative that the central bank intervenes in order to stabilize the value of the currency and recover its SOV demand. If the central bank were unable or chose not to intervene, the self enforcing depreciation would lead to a vicious cycle of high inflation that ends with the currency’s repudiation.

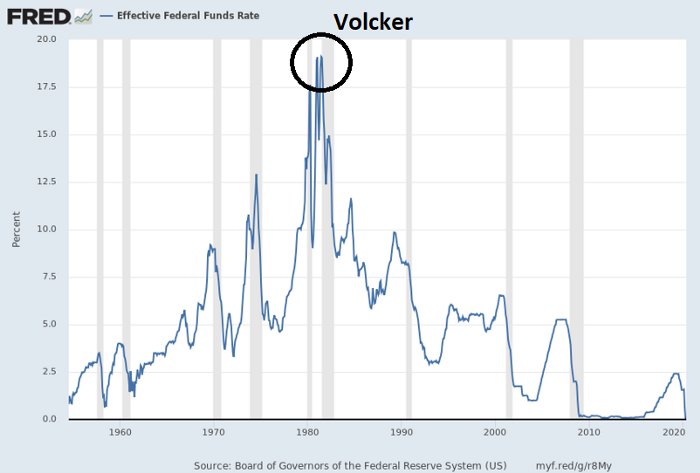

The last time there was an inflationary cycle in the United States was after Nixon closed the gold window in 1971. After 10 years of rampant inflation, Fed Chairman Paul Volcker was forced to raise the interest rate to 20% in order to stabilize the dollar’s purchasing power.

U.S. Effective Federal Funds Rate, Chart Source: FRED

U.S. Effective Federal Funds Rate, Chart Source: FRED

In conclusion, the value of fiat money depends of changes in its supply and its demand. The largest component of fiat currency’s demand is the Store of Value function, if a currency stops acting as a store of value — it starts depreciating — demand falls further and the central bank must intervene in order to reduce the supply and stabilize the currency’s purchasing power. In this regard, the expectation that the central bank will be willing and able to adjust the supply of money in the event of inflation is key to maintaining a currency’s SOV demand. Markets are forward looking, if individuals anticipate the currency will depreciate, they will sell it today. In other words, in order for fiat money to maintain its value, the market must believe that in the event of inflation, central banks are capable and committed to preserving the purchasing power of their currency.

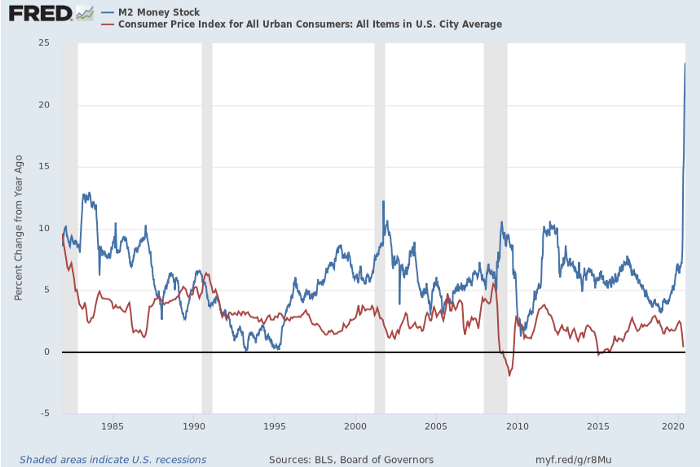

At present, the money supply in the U.S is increasing dramatically: M2 money supply — which includes money in the form of bank cash, bank deposits, and easily convertible near money — is growing at 24% per anum, its highest rate in recorded history, but inflation hasn’t increased in a meaningful manner.

U.S. Yearly Percentage Change M2 Money Supply (blue) & Inflation (Red)

U.S. Yearly Percentage Change M2 Money Supply (blue) & Inflation (Red)

This can be explained because the increase in currency supply has gone hand-in-hand with higher demand for money due to social distancing, uncertainty surrounding the Covid-19 crisis and debt repayments. The absence of inflation also tells us the market is expecting that if in the future, the increase in the money supply leads to inflation, the Fed will be able to raise interest rates in order to stabilize the dollar’s purchasing power.

In this article I argue that the market’s expectations are misplaced; the belief that the Fed can preserve the value of the dollar in the event of rising inflation is unwarranted for three reasons: Firstly, the high debt and leverage in the private sector would make it impossible to raise interest rates without unleashing a depression and a financial crisis. Secondly, balancing the budget in light of the high deficits and public sector debt would require austerity which would lead to social and inter-generational conflicts. Thirdly, the act of raising rates would render the Fed insolvent due to its high leverage and iliquidity.

1- Private Debt

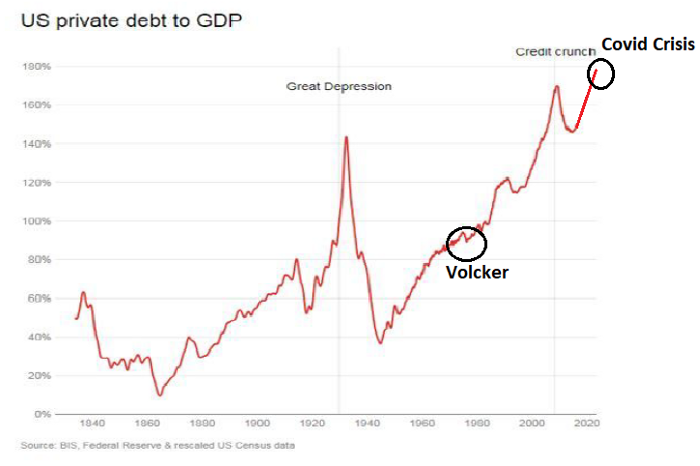

As was mentioned above, the last time there was a loss of faith in the U.S. dollar, Volcker was forced to raise rates to 20% in order to control inflation. The Fed succeeded in stabilizing the value of the currency at the cost of the 1980–1982 recession, however, the economy recovered swiftly thereafter. Back in the 70’s, private debt amounted to less than 100% of GDP but today, it is at an all time high considerably above Great Depression levels.

Total US Private Debt, Source: BIS

Total US Private Debt, Source: BIS

The extreme debt levels means rising rates would not simply cause a moderate recession but would lead to mass defaults in businesses, corporations and households and high unemployment. Austrian economists argue that this “cleansing” process is actually a desirable phenomenon since it corrects the misallocation of resources produced by the artificial credit expansion — See Ben Kaufman’s article for a detailed outline of the Austrian Business Cycle Theory — , however, we are not concerned here with what central banks should do but with what they are likely to do. In this regard, the high levels of unemployment and economic disruption that would result from higher interest rates makes it unlikely that the Fed would chose to go down that path.

To make things worse, most of these loans are issued by commercial banks, and their writing off would result in a financial crisis and a need to — yet again — bailout the banking sector. Before the Great Recession, governments around the world had relatively low debt/GDP ratios which enabled them to recapitalize the banking sector by issuing new debt. Today public debt is at its highest point in history, thus, the government’s ability to bail-out private banks is limited. This would be specially the case in an environment of higher interest rates; since the Fed wouldn’t be buying bonds in the open market, the treasury would have to pay higher interest rates in order to attract bond buyers, making it difficult to issue additional debt to bail-out private corporations. Instead, one should expect a mixture of bail-ins, depositor haircuts and nationalizations.

In conclusion, higher interest rates are unlikely to be pursued by the Central Bank since they would lead to mass insolvencies, a deep depression and a financial crisis.

2- High Deficit & Public Debt

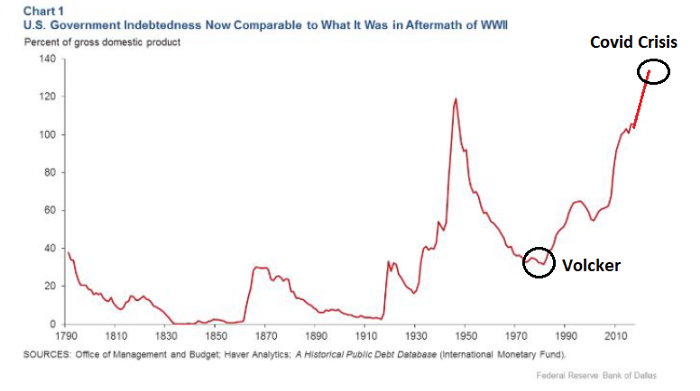

We have already touched upon the second reason why it is unlikely that the fed can keep its commitment to stabilizing the value of the dollar; the high level of public debt. During the 1980’s, government debt only amounted to 35% of GDP compared with an expected all-time high of 140% of GDP post covid-19 crisis.

U.S. Total Government Debt, Source: IMF

U.S. Total Government Debt, Source: IMF

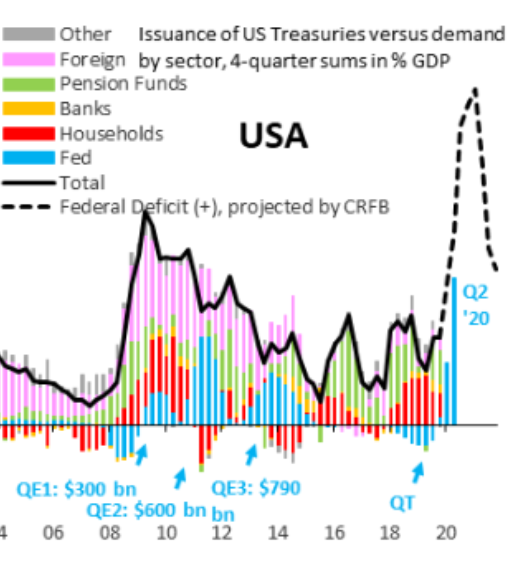

Today, debt levels are so high and yields so low that investor apetite for treasury bonds has dwindled considerably. The following chart shows how foreign investors (pink area) have been purchasing less and less of the total bond issuance every year. Up until 2019, foreign demand was replaced by Pension Funds, households and banks who are legally obliged to buy the Treasury’s bond issuance as long as they can meet their capital requirements.

Source: Federal Reserve, Bloomberg

Source: Federal Reserve, Bloomberg

Lyn Alden has pointed out how how the infamous September 2019 spike in the repo market was due to primary dealers not holding sufficient reserves to absorb the Treasury’s bond issuance and meet their post-Great Financial Crisis regulations — See Lyn’s article for a full explanation. It was at this point that the Fed (blue area) was forced to resume quantitative easing, effectively monetizing the government’s budget deficit which is expected to surpass a shocking 20% of GDP this year.

Having the Fed monetize the deficit allows the government to pursue infrastructure projects, pay extra unemployment benefits, tax cuts and other popular measures that the public is advocating in times of economic hardship and humanitarian distress. If the monetization of the deficit leads to higher inflation, and the Fed chose to raise interest rates in order to stabilize the value of the dollar, it would force the government to balance its budget which could lead to social and inter-generational conflicts. e.g. taxes would need to be raised on the younger segments of the population in order to repay bonds held by retirees.

An alternative strategy could be allowing inflation to run high for a prolonged period of time in an effort to reduce the real value of the debt — as prices go up in nominal terms the real value of the debt falls — , and raise interest rates once debt levels as a percentage of GDP have fallen. As will be discussed later, this avenue is already being proposed by the Fed and would likely lead to a complete loss of faith and repudiation of fiat money and a complete adoption of Bitcoin.

3- Precariousness of the Fed’s Balance Sheet

Even if ones believes the Fed would obliterate the banking sector, unleash a depression and force austerity on the government in order to preserve the value of the dollar, there is a third reason why I believe the central bank would be unwilling to control inflation; doing so would make the central bank insolvent.

Looking at the Fed’s balance sheet, two things stand out: Maturity mismatching and extreme leverage.

Maturity mismatching:

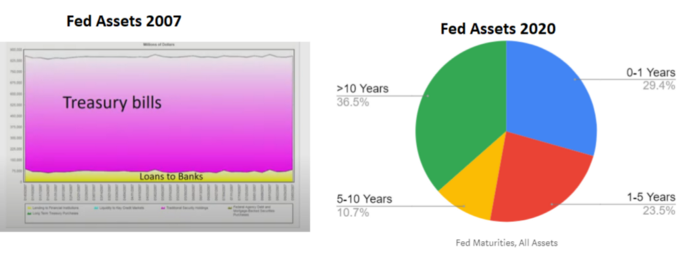

Prior to the Great Recession, monetary policy was limited to short term bills which enabled the central bank to raise rates by simply allowing its assets to mature. Today, the Fed’s holdings are mostly in the form of long dated treasuries and mortgage backed securities with an average maturity above 5 years.

Fed Assets, Source: Federal Reserve

Fed Assets, Source: Federal Reserve

The long duration of the bonds in its portfolio make it impossible for the Fed to raise interest rates by allowing its assets to matures. Hence, if the central bank wanted to raise interest rates, it would need to either sell some of its holdings or increase the interest it pays on excess reserves (IOER). The low yield on its assets and its over-leverage makes it very difficult for the Fed to implement either of these measures effectively.

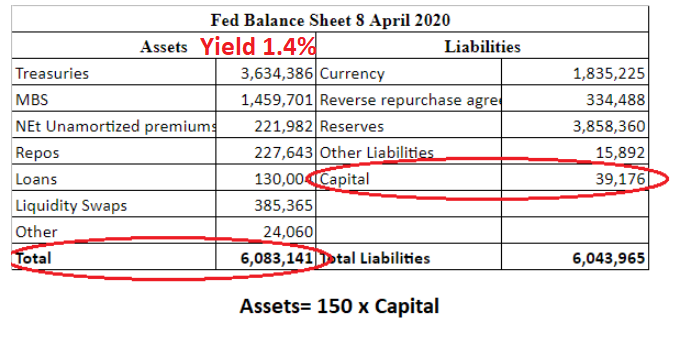

High leverage, assets= 150 x Capital

Fed Balance Sheet 8 April 2020, Source: Federal Reserve

Fed Balance Sheet 8 April 2020, Source: Federal Reserve

At present, the Fed is extremely leveraged with assets just under 151 times capital, ironically, it fails spectacularly to meet the capital requirements it imposes on commercial banks. Furthermore, the average return on its assets has continuously diminished as each round of quantitative easing has pushed bond yields lower: The interest payments it receives on its holdings has dropped from 3% in 2010 to roughly 1,4% in 2019.

These factors make it impossible for the central bank to raise interest rates without revealing its insolvency:

- If it raised rates by selling some of its treasuries, the market would front run its selling resulting in loses which — due to its high leverage — would rapidly lead to negative equity. This already happened during the last unwinding of quantitative easing, when the FED piled billions in paper losses.

- If it chose to raise rates by increasing the interest paid on excess reserves (IOER), it would quickly find itself paying more for its liabilities than the interest payments it earns on its portfolio. Not all of the Fed’s liabilities generate expenses, for example currency in circulation doesn’t pay any interest. Of the total 6 Trillion $ liabilities, 3.9 Trillion (63.4%) are in the form of reserves that the FED would have to pay interest on. The average return on the FED’s assets is circa 1,4%, which leaves them enough room to raise IOER to roughly 2,2 % before their expenditures are higher than their revenues. In today’s ultra low rates environment, 2,2 % interest rates might seem quite high but in a potential scenario of 5 or 7 % inflation — which in light of the financial history of the U.S. doesn’t appear at all outlandish — would lead to massive losses on its holdings.

Of course, the Fed already realizes that any “exit strategy” leads them down the road to insolvency, but what exactly does this mean for this unusual institution? At the end of the day, the Fed’s liabilities (fiat currency) are non-interesting-bearing and irredeemable — having a $10 Federal Reserve note provides a claim on the Fed for $10 worth of Federal Reserve notes, possibly in different denominations, but nothing else. Thus, balance sheet insolvency (assets<liabilities) is a sign of incompetence and mismanagement but the central bank need not worry about a bank run.

Equitable insolvency (failure to pay obligations as they fall due) is more worrisome since the central bank would fail to pay its expenses such as rents, salaries, entertainment services etc. The Fed must rely on the interest it receives on its holdings to fund its operations, but in an environment of higher rates, it would have negative equity. Since the Fed cannot create reserves that are unbaked by assets, it would need to be recapitalized by the Treasury with real tax dollars or new debt issuance in order to pay for its expenses. This would be extremely ironic given that the Fed is currently engaged in Quantitative Easing in order to finance the government’s deficit. It would also be politically unpalatable since the taxpayer would suffer additional austerity in order to recapitalize a central bank that has been used to bail out private corporations.

Conclusions

In the event of inflation, the high levels of public and private debt in the economy and the precariousness of the Fed’s balance sheet would make it impossible for the central bank to preserve the value of the dollar without unleashing a socio-economic and political crisis. If it tried to restore trust in its currency by raising rates, like Volcker did in the 80’s, it would cause household and corporate defaults that would result in a financial crisis and a depression. In parallel, the government would be forced to balance the budget, imposing severe austerity that would lead to inter-generational and social conflicts. Furthermore, in the process of raising rates, the Fed would become insolvent and would need to be recapitalized by the Treasury. This would result in social and political backlash, as well as undermining the central bank’s alleged independence.[1]

Centrals banks were created for the benefit of the financial services industry and the State, hence, it is unlikely that they will chose a policy path that is directly opposed to the interests of their main constituents. Instead, they will likely allow inflation to run rampant, hoping to reduce the real value of public and private debt before they can safely raise rates again — since most debts are fixed nominally, when the currency devalues significantly and prices/assets/wages go up in nominal terms, debts vs GDP goes down. This strategy is nothing new, the Fed already inflated away the debt after World War II and is openly proposing the same approach today — NBER working paper and Cleveland Fed.

Chart Source: Bridgewater Associates, Ray Dalio, Updated by Lyn Alden, Annotated by Gael Sanchez

Chart Source: Bridgewater Associates, Ray Dalio, Updated by Lyn Alden, Annotated by Gael Sanchez

Back in the 40’s, gold had been outlawed and investors didn’t have a highly liquid store of value alternative, so they accepted the losses on their currency and bond holdings and demand for the dollar returned once Volcker stabilized its purchasing power.

We can think of fiat money today as somewhat of a Ponzi scheme, it only holds value for two reasons: Firstly, there is an expectation that in the event of inflation central banks will preserve its purchasing power via contractionary monetary policy and secondly, new buyers will demand it in the future. [2] As the market realizes these two conditions won’t be met, one should expect a repudiation of State liabilities — government bonds and fiat currency — and a move towards hyperbitcoinization.[3] This outcome should come as no surprise as Austrian Economists have been warning about it for decades.

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.” Ludwig von Mises, _Human Action (_1949)

I believe Mises would agree that given today’s unsustainable debt levels and the political and social incentives, the latter option is by far the most likely outcome.

Many thanks to Stefanie von Jan, Ben Kaufman and Emil Sandstedt for proofreading the text and for their very insightful comments.

Notes:

- This article is not an argument against the U.S. dollar per se but against the sustainability of the fiat system as a whole. Major central banks around the world are going down the same road as the Fed and the analysis is aplicable to most jurisdictions . Moreover, given that the Dollar is the reserve currency, its demise would most likely breach the trust in the fiat system worldwide.

Source: Haver Analytics

Source: Haver Analytics

2. Expectations are crucial; even if the growth of the money supply is halted, the demand for a depreciating currency needn’t return instantaneously. Monetary authorities have breached the trust of investors so many times, that in my opinion, even a credible announcement by the Central Bank would not be enough to recover investors trust. They will likely need to buy and prove they hold Bitcoin in order to truly regain trust in their currencies. Of course, by that point, hyperbitcoinization will have run its course and bitcoin will already be the economy’s medium of exchange, unit of account and store of value.

3. As individuals repudiate fiat currencies, governments might try to outlaw Bitcoin like they did with gold in 1933. Whether they succeed in doing this or not will depend largely on technological factors. If the decentralization of the network is preserved and anonymity tools are readily available, banning Bitcoin will be a practical impossibility. Furthermore, as is mentioned in the article, money is always a market phenomenon. Unless fiat money is stabilized, it won’t be used as money regardless of what the State dictates. (we can see this reality today in Argentina and Venezuela)