Visions of Bitcoin

Visions of Bitcoin

How major Bitcoin narratives changed over time

By Nic Carter & Hasu

Posted July 29, 2018

Do I contradict myself? Very well then, I contradict myself I am large, I contain multitudes.

– Walt Whitman, Song of Myself

Perhaps the most enduring source of conflict within the Bitcoin community derives from incompatible visions of what Bitcoin is and should become. Businesses building on Bitcoin, believing it a cheap global payments network, eventually became nonviable when blocks filled up in 2017. They weren’t necessarily wrong, they just had a vision of the world that ended up being a minority view within the Bitcoin community, and was ultimately not expressed by the protocol on their desired timeline.

In the absence of a recognized sole leader, Bitcoiners refer to founding documents and early forum posts to attempt to decipher what Satoshi truly wanted for the currency. This is not unlike US Supreme Court justices poring over the Constitution and applying its ancient wisdom to contemporary cases. Others reject textual exegesis and focus instead on a pragmatic analysis in context.

Conflicts within Bitcoin thus arise from entities who hold visions of the protocol that are mutually exclusive — and this leads to friction when these visions cannot be reconciled. Visions of Bitcoin are not static. Technological developments, practical realities and real-world events have shaped collective views. This post is an attempt to aggregate the various dominant narratives that have characterized Bitcoin throughout its 9-year history. This post builds on excellent prior work by Murad Mahmudov and Adam Taché, and we suggest you add that to your reading list.

Changing narratives

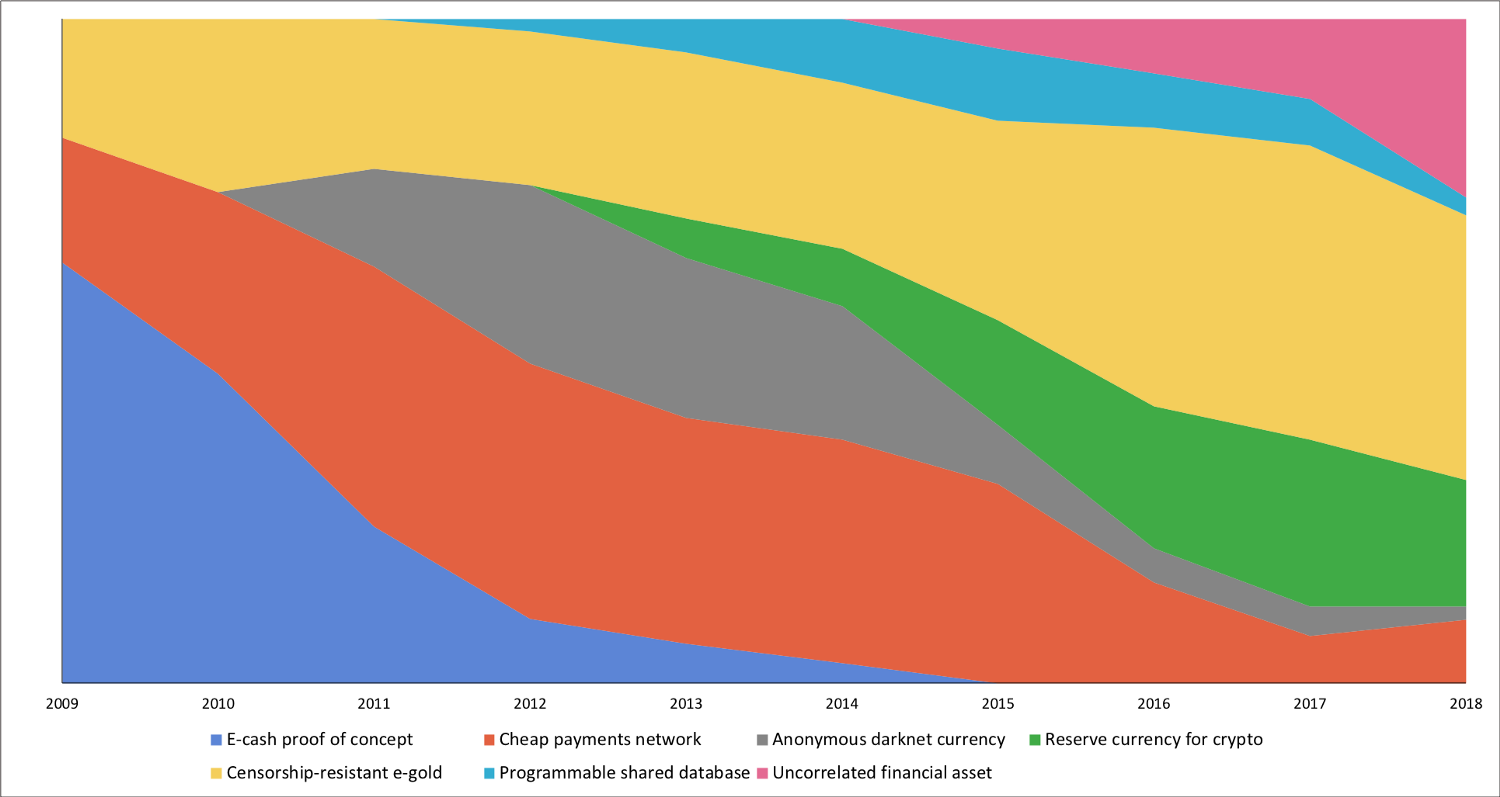

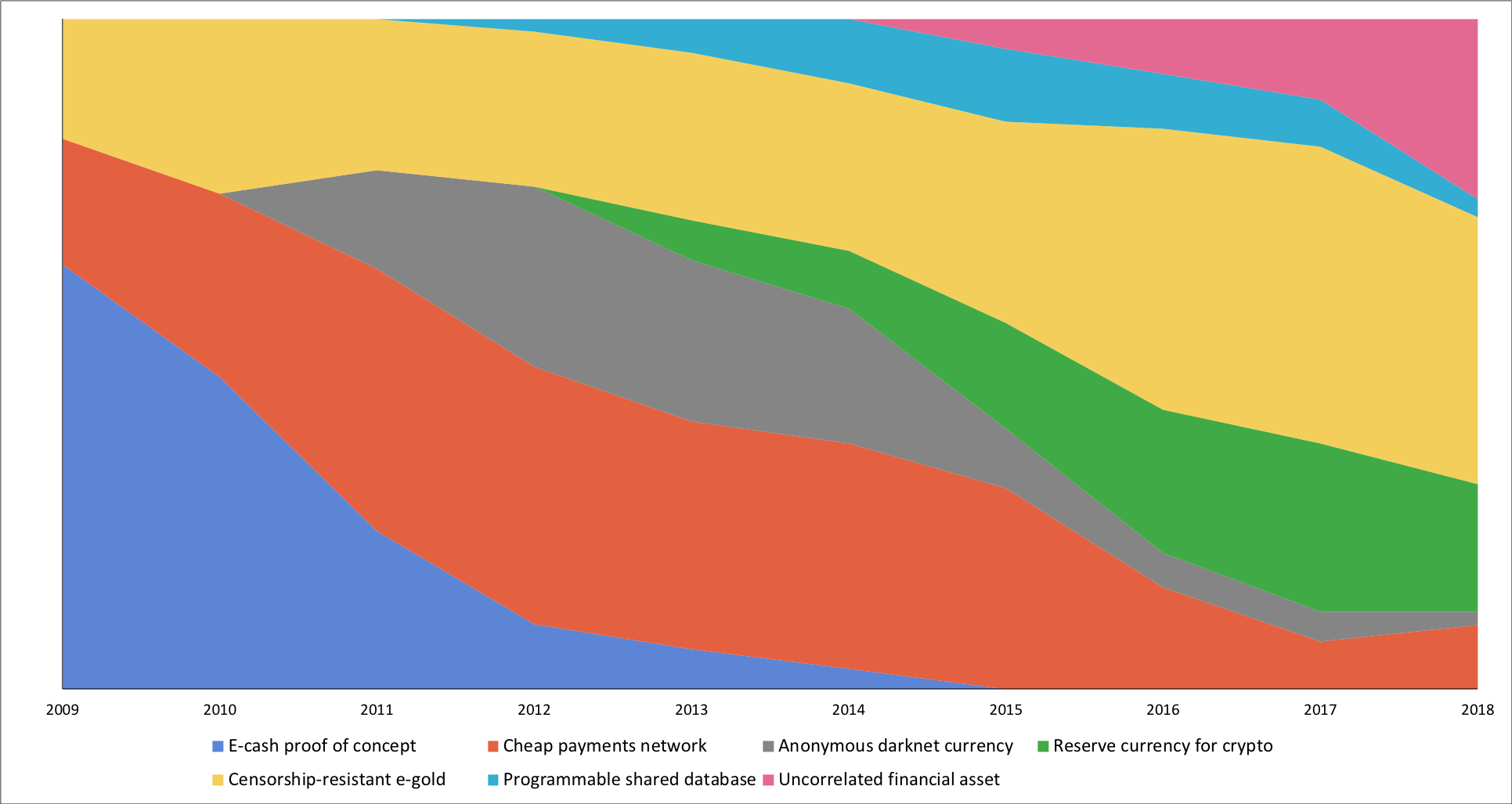

Here, we want to more granularly explore the prevalence of key narratives. We identify seven distinct major themes that have held positions of prominence among Bitcoiners throughout its history. Note that these do not necessarily have to be the most influential narratives — we are instead focusing on major strains of thought that have characterized Bitcoin users.

In rough order of appearance, these are:

- E-cash proof of concept: the first major narrative, this was the general view of Bitcoin in its earliest days. Back then, cypherpunks and cryptographers were still appraising the nascent project and determining whether it worked, if at all. Since all prior e-cash schemes had failed, it took a while for people to be convinced of its technical and economic viability and move on to more expansive conceptions of the protocol.

- Cheap p2p payments network: an extremely popular and pervasive narrative. Some believe this is what Satoshi had in mind — a straightforward currency for peer to peer internet transactions. A decentralized Paypal or Venmo, if you will. Since microtransactions are a key component of internet commerce, proponents of this view generally believe that low fees and convenience are an essential characteristic of such a currency.

- Censorship-resistant digital gold: the counterpoint to the p2p payments narrative, this is the view that Bitcoin primarily represents an untamperable, uninflatable, largely unseizable, intergenerational wealth store which cannot be interfered with by banks or the State. Proponents of this view de-emphasize Bitcoin’s use for everyday transactions, arguing that security, predictability, and conservatism in development are more important. We’re callously lumping in sound money believers into this camp.

- Private and anonymous darknet currency: the view that Bitcoin is useful for anonymous online transactions, in particular to facilitate black market online commerce. This is not necessarily mutually exclusive with the e-gold position, as many proponents of the digital gold view believe that fungibility and privacy are important attributes. This was a popular narrative before the chain analysis companies had success de-anonymizing Bitcoin users.

- Reserve currency for the cryptocurrency industry: this is the view that Bitcoin serves an essential purpose as the native currency for the cryptocurrency/cryptoasset industry more generally. This is a view espoused by traders for whom BTC is the numeraire — the currency in which the prices of other assets are quoted. Additionally, traders, businesses, and distributed networks that hold reserves in BTC de-facto endorse this view.

- Programmable shared database: this is a slightly more niche view, and generally involves the understanding that Bitcoin can embed arbitrary data, not just currency transactions. Individuals holding this view tend to see Bitcoin as a programmable, expressive protocol, which can facilitate broader use-cases. In 2015–16, it was popular to express the notion that Bitcoin would eventually absorb a diverse set of functionalities through sidechains. Projects like Namecoin, Blockstack, DeOS, Rootstock, and some of the timestamping services rely on this view of the protocol.

- Uncorrelated financial asset: this is a view of Bitcoin that treats it strictly like a financial asset and finds its most important feature to be its return distribution. In particular, its tendency to have a low or nonexistent correlation to all manner of indexes, currencies, or commodities makes it an attractive portfolio diversifier. Proponents of the view are generally not too concerned about owning spot Bitcoin; they are interested in exposure to the asset. Put another way, they want to buy Bitcoin-flavored risk, not necessarily Bitcoin itself. As Bitcoin has become more financialized, this conception has gained steam.

In the chart below, we’ve weighted these various narratives according to their popularity at the time.

This isn’t modern art — it’s our representation of Bitcoin’s changing tides

This isn’t modern art — it’s our representation of Bitcoin’s changing tides

In this chart, we lay out the relative influence of the seven narratives we identified above. As you can see, the e-cash proof of concept was the dominant view at the start, although the p2p payments network and digital gold views were also espoused at the time. Later, Bitcoin as an anonymous darknet currency gained steam with the Silk Road. The idea never really died off, and Bitcoin is still used on the darknet today, even though other privacy-oriented alternatives exist.

As ICOs were invented and a broader market of altcoins began to proliferate, BTC became the reserve asset for that larger economy. This grew to become a significant feature of Bitcoin, especially in the bull markets of 2014 and 2017. We note that the p2p payments contingent remained influential until mid 2017, when they largely migrated to Bitcoin Cash (some had already left for Litecoin and Dash). However, with the emergence of Lightning in 2018, there has been an upswing of enthusiasm for online microtransactions and fee-less internet payments.

In 2015 and 2016, sidechains became a popular talking point, and it was assumed that Bitcoin would soon boast a much-expanded functionality, obsoleting most altcoins. Related functionality-extending projects like Mastercoin (now Omni), colored coins, Namecoin, Rootstock, Blockstack, and Open Timestamps, contributed to this general view. However, as sidechains proved complicated to implement, non-money uses of Bitcoin fell out of favor.

As Bitcoin emerged from the 2014–15 bear market, analysts began to contemplate its status as a differentiated commodity-money. In November 2015, Tuur Demeester published an investment note entitled “How to Position for the Rally in Bitcoin,” arguing that it had unique characteristics as a portfolio asset. In mid-2016, Burniske and White influentially argued that Bitcoin represented an entirely new asset class. These analysts noticed Bitcoin’s stubbornly low correlations with traditional assets, and as this persisted, Bitcoin as a portfolio diversifier gained steam among certain forward-looking corners of the asset management industry. Today this is a popular view, driving much of the demand for financial products which would give traditional investors exposure to Bitcoin.

Throughout all these regimes, the digital gold conception has remained influential, and now is the consensus view, predominating over the p2p petty cash faction, which largely departed with Bitcoin Cash. Today, after years of strife and infighting, this is the majority view. However, not all Bitcoin users are ideological bitcoiners, and wanted to reflect this in the chart. Many Bitcoin holders hold it as a portfolio diversifier, some still use it for anonymous darknet transactions, and the p2p cash contingent has re-emerged alongside Lightning.

Tension and release

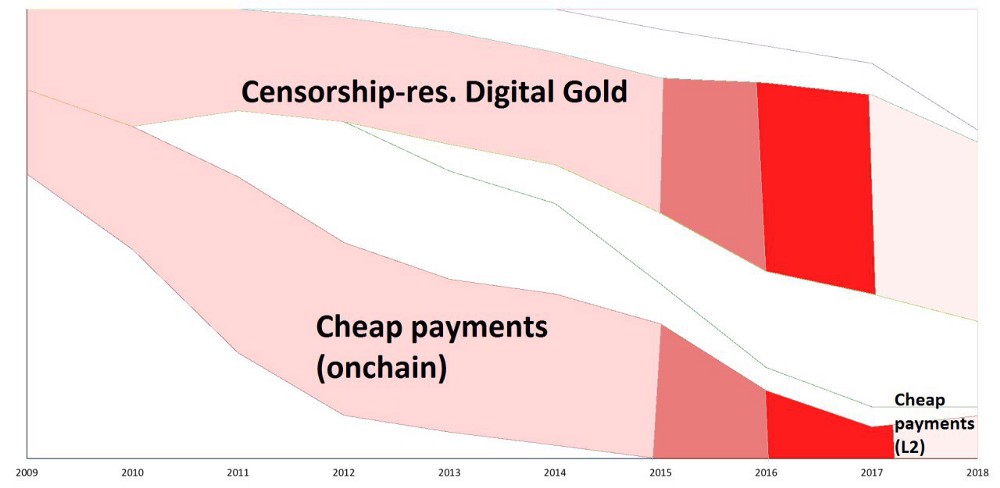

If you scrutinize the above chart, you’ll notice that some of the visions of Bitcoin are entirely incompatible. For instance, a move to a global on-chain payments network conflicts with the digital gold view, as emphasized by Spencer Bogart. We’ve depicted the conflict between these views of the world by isolating them on this chart.

The conflict really began to be fought seriously with the release of BitcoinXT in 2015, although rancorous discussions had long preceded that. Further provocations including Bitcoin Classic, Unlimited intensified the conflict. It reached its peak in mid 2017 when Bitcoin Cash finally forked. During the bull run of late 2017, Bitcoin fees reached extreme levels, leading to defections to the Bitcoin Cash camp. However, since then, fees have settled down and the need for big blocks appears less urgent.

Additionally, in early 2018, Lightning implementations became viable, and micropayments with Bitcoin emerged. Thus, the tension dissipated, as both camps were able to pursue their own objectives. We noted an uptick in the cheap payments school of thought from within the Bitcoin crowd in 2018, as there has been a resurgence of optimism for payments through second-layer solutions.

An interesting conclusion that we think can be drawn from the analysis is that Bitcoin is currently benefiting from a rare period of relative harmony. While there is no single view that entirely dominates, the digital gold narrative is certainly most prevalent right now. The civil wars of 2015–17 ended with the Bitcoin Cash fork, and migrations to other p2p payment factions like Litecoin, Dash, and Nano. For now, the tension seems to be largely resolved, and we find ourselves in an unusually placid era in Bitcoin’s history. Subjectively, it appears that under this comparatively peaceful regime, development seems to be progressing more rapidly. Endless social media battles, conference-driven agreements, and positioning for contention forks certainly created a drag on developer efforts. There is another battle looming, however.

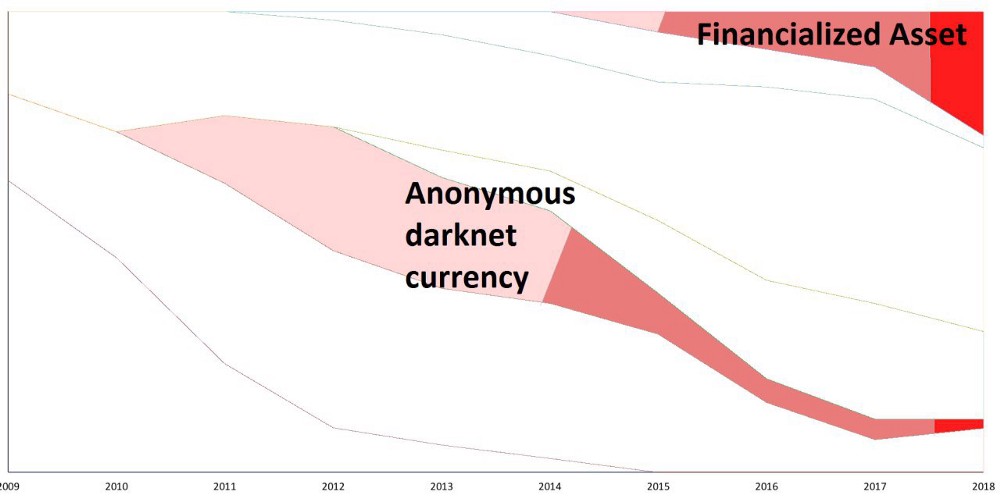

As depicted in this chart, the anonymous and fungible vision of Bitcoin (generally preferred by the digital gold camp) is somewhat at odds with the financialised, transparent version which is growing in popularity. Individuals that want exposure to Bitcoin the financial asset tend to prefer a Bitcoin which is compatible with AML/KYC and tend to put a lesser emphasis on privacy or fungibility. Many pundits believe this will be the next bitter fight for the soul of Bitcoin.

Ultimately, both the conflict and the peacetime phases are important. Conflicts reveal where power structures reside, and tend to yield informative signals about how key stakeholders truly feel. Under duress, business, individuals, and developers are forced to take sides, revealing their genuine preferences for the development of the protocol.

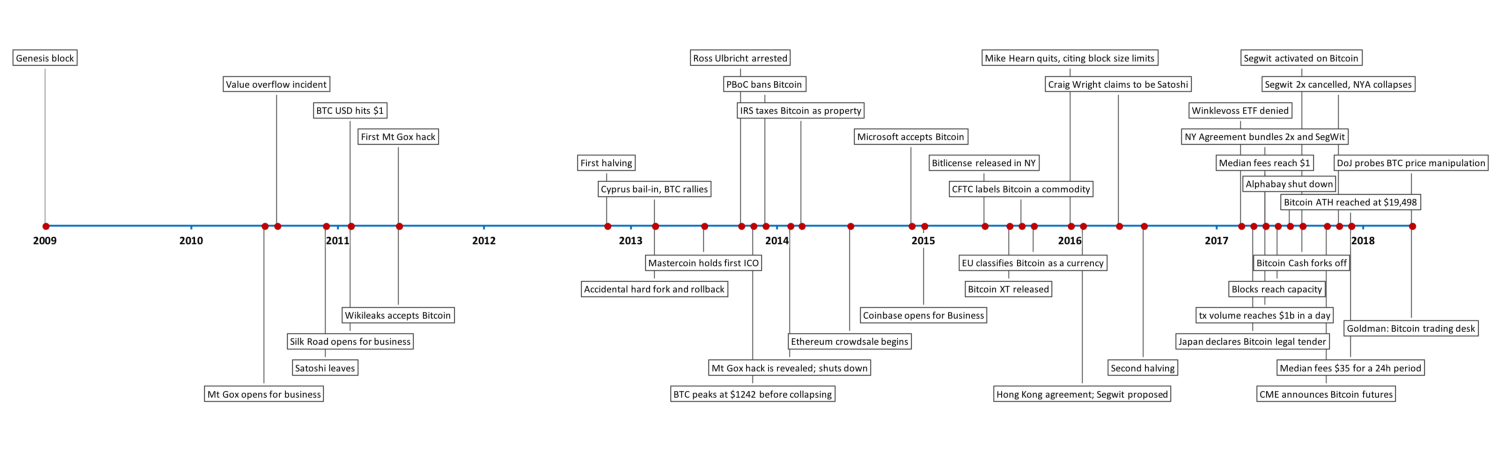

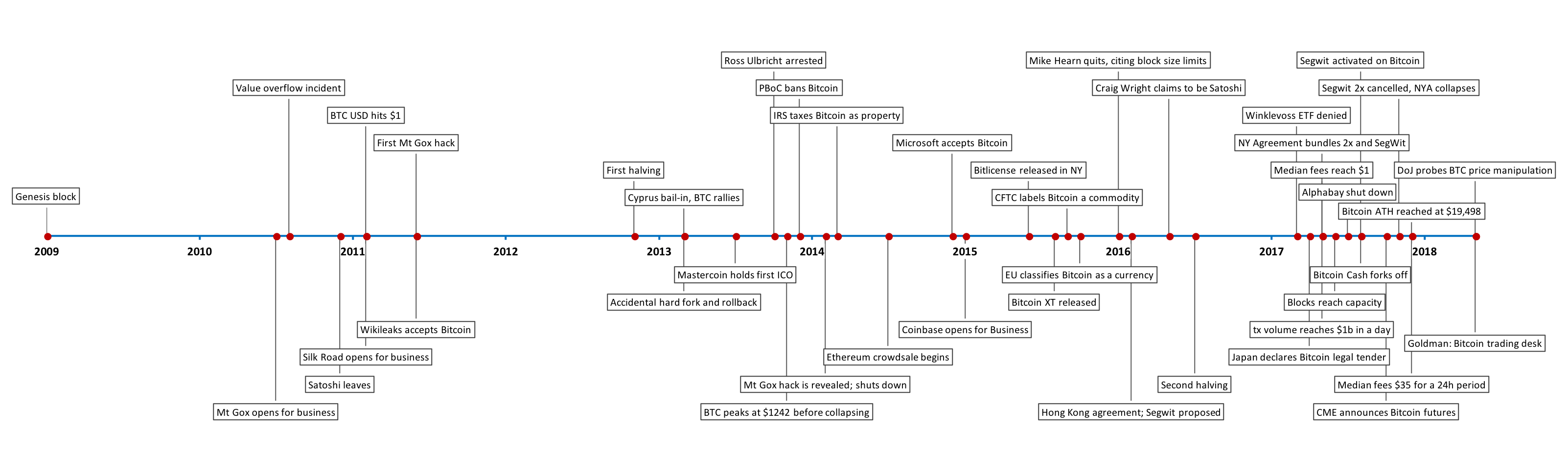

Timeline of events

We are aware that much of our analysis relies on our subjective interpretation of old BitcoinTalk posts. If you disagree, we welcome you to suggest an alternative. To make subsequent analyses easier, we’ve put together a timeline of key Bitcoin events, tracking its entire history. (We drew heavily on the 99bitcoins annotated price chart to make this.) We recommend considering our colorful ‘changing tides’ chart alongside the below timeline. The juxtaposition should help elucidate why exactly we made the decisions that we did.

(

({kind=link}

{kind=link}

Conclusion

We put together the changing narratives chart through an analysis of BitcoinTalk posts, a set of discussions with Bitcoiners who had been there from the very start, a healthy respect for Bitcoin history, and a recollection of major attitudes over the years. Anyone who has been around Bitcoin long enough should be able to perform a similar analysis.

We’re not positing our analysis as the absolute truth. Instead, we want to nudge Bitcoiners away from absolutism and acknowledge that major narratives within the Bitcoin community have changed over time. And that’s ok — it’s appropriate to change your mind in response to new data. Purity tests are generally weak, since they tend to require that individuals do not evolve. But if most Bitcoiners went back and contemplated their own past histories, they would probably find that they evolved over time, too. Both of the authors have certainly been through the cycle.

In the end, a healthy respect for Bitcoin history is a necessary starting point of any attempt to define it. It is not unitary, and Bitcoiners are not ideologically homogenous. Bitcoin contains multitudes, and it’s important to remind ourselves of that.

Thanks to Dan McArdle and Murad Mahmudov for the input.