WORDS is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

WORDS is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

Donate & Download the March 2020 Journal PDF

Remember, if you see something, say something. Send us your favorite Bitcoin commentary.

A Cover Letter to Ray Dalio

By Hass McCook

Posted February 22, 2020

That said, it’s not always easy to get the very busy (and skeptical) Ray Dalio’s of the world to sit down for a few hours, so I hope this cover letter can encourage him to have an open mind, and give Bitcoin a few hours of his time. ROI on those few hours could be bigger than any return he’s witnessed in his highly illustrious and successful career.

Bitcoin is most definitely not an “easy get”. Most ultra-bullish Bitcoiners only become that way due to a deep understanding of the history and properties of money-as-we-know-it, the technology behind Bitcoin, macro, micro and behavioural economics, as well as the dynamics of start-up companies and technologies in bootstrapping themselves and realising network effects. Less technical people observe the IQ density of the space, through its industry leaders and broader development community, which allows for a high level of believability-weighted decision making. I believe you have one of the best grasps of these concepts in the world, so I ask that you humour me for a few minutes to allow me to demonstrate just how much Bitcoin aligns with your personal views and fundamentals. This journey isn’t quick — the most dedicated Bitcoiners have put in thousands of hours of research and knowledge development, as well as many hundreds of days “in the saddle” with exposure to the whims of the Bitcoin Rollercoaster. I hope that by the end of this letter you will at least consider revisiting the topic of Bitcoin with a bit more depth.

Bitcoin has been likened by some to be reflective of a startup organisation; currently heading into its Series B fund raise. Bitcoin is a well-oiled “un-organization” with founders but no CEOs, many volunteers but no employees, where the best ideas are developed and implemented by consensus regardless of who proposed the idea, and provably non-diluting equity available to anyone who is willing to trade their energy for it. This is all baked into the code, and it is radically transparent for anyone wishing to participate in the ecosystem. So transparent, that an individual can verify anything they need to about the Bitcoin network by simply running some software on a very basic computer setup in the order of $200 and with the most basic of internet connections. It may likely be one of the best real-life examples of an Idea Meritocracy at play — the cultural paradigm that you originated at Bridgewater.

Idea Meritocracies are microcosms of what a “truly free” market should be. There aren’t many, if any, examples of free markets in the wild; except of course, Bitcoin. The competition in the Bitcoin space is merciless, where the best products having a shelf-life of months before being made redundant by superior products. Most industry leading service providers will find themselves competing with a free product not long after establishing themselves. As at date of writing, the Bitcoin space even meets several criteria of the “theoretical” perfectly competitive market. Bitcoin’s nature as an open-source, public, encrypted, distributed ledger means that the blockchain guarantees radical transparency, property rights and homogeneity of product, at zero or near-zero transaction and storage cost. The factors of production (labour, equipment, and capital) are mobile to the extent that only a communication link and a power source is required to participate in the ecosystem. Developing on top of Bitcoin requires no permission, and if entrepreneurs have a good enough idea, securing start-up capital is not a difficult barrier to entry to overcome. Information asymmetry, low number of market participants, and externalities from use of non-renewable energy to mine will all be resolved in time, most likely by the end of this decade. The critical thing to note is, although there are relatively few people who own the majority of Bitcoin now, once Bitcoin is spent in the future during the redistribution phase, it is spent forever — there are no reprints. If you want your Bitcoin balance to stay the same or increase, you must be creating value for someone. There is no free lunch with Bitcoin.

A central tenet of your school of thought is open-mindedness, and I encourage you to suspend disbelief and allow yourself to be immersed in high quality Bitcoin content; whether through attending a Bitcoin-only conference, books, podcasts, or even attending your local casual Bitcoin meetup. When meeting Bitcoiners in the real world, you are guaranteed to witness more IQ packed into one small place than you have ever witnessed in your life. Bitcoin was created and fostered by the most radically open-minded, and the development of its technology over time was only possible through radical open-mindedness in the developer community, and of the wider user community once improvements were thoroughly scrutinised and ready to be implemented.

I’m sure that a lot of these arguments have hit home — after all, you personally coined the majority of the arguments I used to present The Case for Bitcoin. It is daunting and confusing to step into such a revolutionary realm, but you will find that if you are willing to radically open your mind, your fundamentals are 100% aligned with Bitcoin’s.

Bitcoin Price Will Always Be Too Expensive if You Don’t Believe in Its Revolution

You need to be able to make a decision, and then take action.

By Sylvain Saurel

Posted March 1, 2020

Inlife, there is nothing worse than hesitation. I often see people spend a lot of time hesitating before they finally never take action. These people always imagine that there might be a better time. They wait for the perfect moment, which never comes.

These people somehow make the choice to live with regrets about the actions they might have taken.

With Bitcoin, I have a feeling that a lot of people have been going through the same thing for several years now. When Bitcoin price was $1K, they were reluctant to buy it because they thought Bitcoin was too expensive.

It was the same thing when Bitcoin reached $2K, then $3K, and finally $5K. Many of these people then literally jumped on Bitcoin when it reached $20K at the end of 2017.

Today, Bitcoin is around $8.5K after reaching $10K in early February 2020. This sudden drop in price is once again questioning these hesitant people. At the heart of their hesitation is the same question that comes up again and again:

Is this a good time to buy Bitcoin? Is its price too expensive?

I’m going to disappoint some people, but the reality is that Bitcoin will always be too expensive if you’re one of those people who don’t fundamentally believe in it.

I will explain why in this story.

A Lot of People Are Thinking About Buying Bitcoin

With the approach of the third Bitcoin Halving, and an excellent beginning of the year for Bitcoin price, many people began to wonder if they were missing the Bitcoin train.

When Bitcoin surpassed $10K on February 9, 2020, many people began inquiring about buying Bitcoin.

The same people who weren’t interested in Bitcoin when it was $3.3K at the end of 2018, became interested in Bitcoin when it reached $10K.

How do you explain this strange psychological phenomenon? Quite simply by the feeling of FOMO (Fear of Missing Out).

These people are non-believers who are simply afraid of missing out on the Bitcoin opportunity. They’ve been thinking about buying Bitcoin for months, even years, but never dare to take action.

Any excuse is good for not taking action now by buying Bitcoin.

Bitcoin would be too complicated if you listen to them. There are risks of losing what you own. There are no guarantees on your Bitcoin like you can have guarantees with your fiat currency stored in a bank account.

This list is far from exhaustive, but is representative of what many people will tell you to justify not taking action by buying Bitcoin.

These People Are Always Waiting for the Best Time to Buy Bitcoin

In addition to these justifications, people who hesitate will tell you that Bitcoin is too expensive. They are waiting for the best time to buy Bitcoin. To these people, I often say the following:

On what do you base your opinion that Bitcoin is too expensive?

When Bitcoin price is $10K, and you choose not to buy Bitcoin, what criteria do you think it is too expensive based on?

Generally, you think Bitcoin is too expensive because its price was $3.3K at the end of 2018. At the end of 2018, you had doubts about the $3.3K price because Bitcoin was in the middle of a very strong and prolonged bear market.

In 2017, when Bitcoin started the year at $900, you weren’t even paying interest on it.

Indeed, Bitcoin seemed to you at that time to be simply a system for geeks who dreamed of revolutionizing the current monetary and financial system.

You became interested in Bitcoin when the media started talking about it when its price exceeded $2K in June 2017.

Rather than trying to understand why Bitcoin was a revolution, and how it worked, you simply told yourself at the time that you were going to wait until it dropped below $1,000 to buy it.

And then, Bitcoin’s price soared to $10K by the end of November 2017.

At each additional step up, you have been psychologically blocked by thinking that if Bitcoin was worth $900 at the beginning of the year, it was too expensive today when its price was $10K.

When Bitcoin surpassed $15K in December 2017, you finally took the plunge for fear of missing the train. Bitcoin quickly reached $20K in a hurry, and you felt reassured.

The speculative bubble that formed around Bitcoin price as a result of this widespread euphoria burst throughout 2018, and you panicked.

You capitulated and sold your Bitcoin in early February 2018 when its price fell below $10K.

You lost a lot of money. This prevented you from buying Bitcoin again when it was at $3.3K.

There’s No Such Thing As the Best Time

Generally speaking, there is no such thing as the best time to take action in life. You will always find a reason to wait. And by the time you do, it will really be too late.

You will take action because you will be affected by what happens, not because you have decided to.

Then you will be in a worse position than if you had taken action right away when you were offensive.

Since there is no such thing as the best time, it is up to you to create the perfect conditions. These conditions are created when you take direct action with a positive mindset.

With Bitcoin, it’s exactly the same thing.

There is no better time to buy Bitcoin. Bitcoin wasn’t too expensive at $3K, just as it wasn’t too expensive at $10K or $20K.

Bitcoin Will Always Be Too Expensive if You Don’t Believe in It

In order to be able to judge what a correct price for Bitcoin might be, you need to understand what Bitcoin is. Once you understand how Bitcoin works, and how it is a complete paradigm shift from the current monetary and financial system, you will be better able to judge its price.

You still won’t be able to say whether its price is too expensive or not, because no one really can, but you will understand that all your questions about its price are useless at the moment.

Bitcoin is limited to 21 million units. This is true today, and will still be true in 10, 25 or 50 years from now.

There are currently 7.8 billion people on Earth. When there are 10 billion people on Earth around 2050, there will still be 21 million Bitcoins available.

If you believe in the Bitcoin revolution, then you will realize that this is at most 1 Bitcoin for every 476 people on Earth.

That is very small. So the demand for Bitcoin is going to explode. With the extreme scarcity of Bitcoin, you don’t have to be an expert in the law of supply and demand to understand that Bitcoin price will literally explode.

An interesting exercise then consists in comparing Bitcoin and its $160 billion capitalization with the valuation of other markets:

- The world’s gold stock is the equivalent of $8T

- The global capitalization of the stock market, which reached $73T

- The global money supply that reaches $90T

- The global real estate market reaching $228T as a whole

- The global debt which is astronomically high at $246T

The first thing that stands out is that the capitalization of Bitcoin is currently negligible in comparison to these other markets.

Then, let’s imagine for a moment that the capitalization of Bitcoin reaches the equivalent of the global amount of money in circulation, that is $90T.

Applying a simple rule of three, this would give us a price of about $4.2 million for one Bitcoin.

This figure may sound crazy to you, but it clearly isn’t if you have complete confidence in Bitcoin and what it is trying to build for the future.

With such a level of confidence in Bitcoin, you will easily be able to take action whether Bitcoin price is $3K or $10K.

On the other hand, if you don’t believe in Bitcoin, its price will always be too high, and you will never take action.

Bitcoin Rewards Those Who Truly Believe in It and Take Action

Bitcoin has been advancing at its own pace since its creation by Satoshi Nakamoto on January 3, 2009. It has proven to be a special case since its price is not correlated to any other asset.

Day after day, block after block, Bitcoin continues to move forward in building a fairer and freer world for all in the future.

Launched in complete anonymity, Bitcoin has become in just over 11 years the only credible alternative to the current monetary and financial system.

Bitcoiners are growing in numbers, and even its fiercest opponents are really starting to fear it. This is the ultimate proof that Bitcoin continues to move in the right direction.

Once you’ve taken the time to understand what Bitcoin is, and why the total paradigm shift it proposes is a revolution, you will clearly no longer have any doubts. You will be able to truly believe in Bitcoin.

If you have complete confidence in Bitcoin, you won’t find its price too expensive, and you’ll be able to take action to buy it whether its price is $3K, $10K, or even $20K.

If you don’t trust Bitcoin, and that is your right, it will always seem too expensive to you.

A psychological brake will always prevent you from taking action, and you may have regrets in the future when you realize that you missed the Bitcoin train.

It’s up to you to know what you want to do for your future with full knowledge of the causes.

Bitcoin’s Habitats

How Bitcoin is surviving and thriving between worlds

By Gigi

Posted March 1, 2020

As I have argued previously, Bitcoin is a living organism. But where does this organism live, exactly? As with many questions in the world of Bitcoin, exact answers are hard to come by. Living things have fuzzy edges: beginnings and endings are hard to pin-point, differentiation is more-or-less arbitrary, and what was classified as a wolf today might evolve to be a dog tomorrow.

Bitcoin has no rigid specification, no absolute finality, no fixed development team, no final security guarantees, no scheduled updates, no central brain, no central vision, no kings, and no rulers. It is a decentralized organism, organically evolving without central planners. The lack of any centralization is the source of Bitcoin’s beauty, it’s organic behavior, and it’s resilience.

Bitcoin is everywhere and nowhere, which makes figuring out where this thing lives a daunting task. However, it turns out that there is a space it lives in. Multiple spaces, as we shall see.

The Habitats of Bitcoin

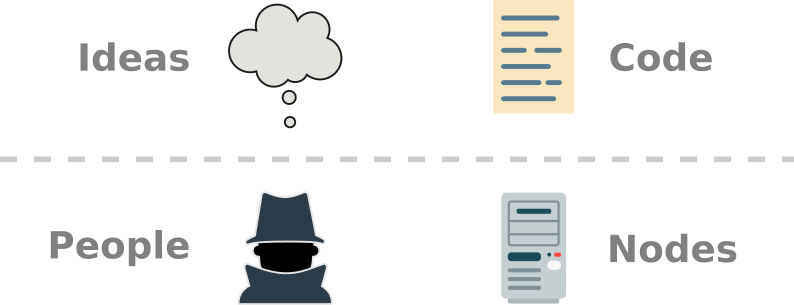

While classifying the habitat of a decentralized organism isn’t trivial, we can look at the constituents of Bitcoin to make the task a bit easier. As outlined in the last article of this series, Bitcoin lives across domains, with one foot in the purely informational realm (ideas and code) and one foot in the physical realm (people and nodes).

An awareness of Bitcoin’s environment(s) might help to better understand this new form of life. No organism can be meaningfully studied in isolation, and Bitcoin is no exception. As Alan Watts pointed out, one has to be aware of the basic unity every organism forms with its environment.

“For the ecologist, the biologist, and the physicist know (but seldom feel) that every organism constitutes a single field of behavior, or process, with its environment. There is no way of separating what any given organism is doing from what its environment is doing, for which reason ecologists speak not of organisms in environments but of organism-environments.” Alan Watts

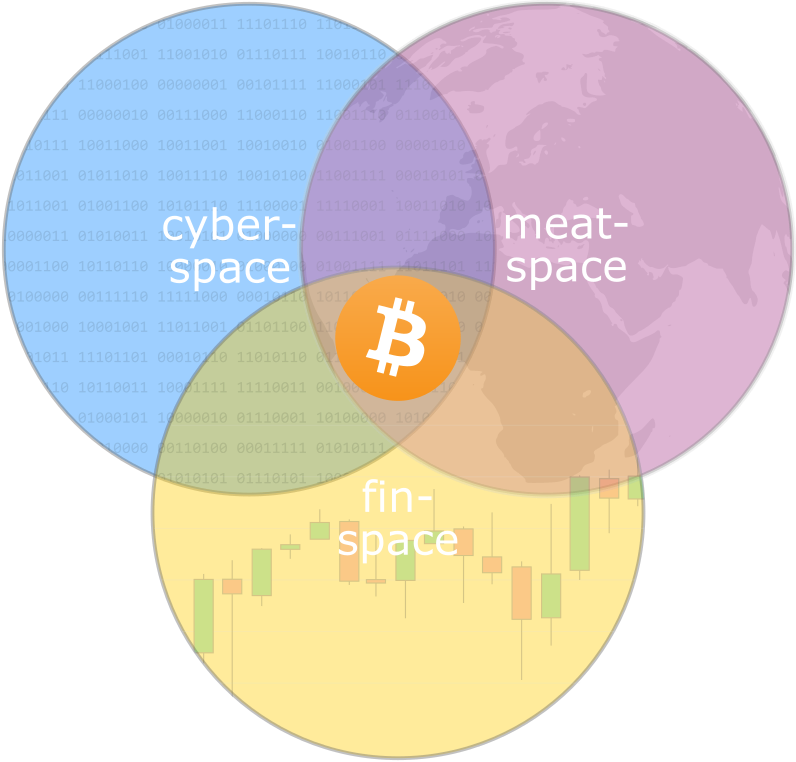

With that in mind, let’s take a closer look at the organism-environment(s) we are dealing with. As outlined above, Bitcoin’s ideas and code inhabit one realm, and Bitcoin’s people and nodes inhabit another. To stick with tradition, let’s call the physical realm “meatspace” and the purely informational realm “cyberspace” — even if, as always, the lines might be fuzzy around the edges.

The “soul” of Bitcoin, so to speak, lives in cyberspace. There, Bitcoin absorbs useful ideas and incorporates them into its code. As with all living things, something is useful if it helps an organism to survive. While Bitcoin has various self-regulatory mechanisms to react to the environment, new ideas may be necessary for survival if changes are drastic enough.

The “body” of Bitcoin, like all bodies, is living in meatspace. Nodes, hard drives, cables, and other things come together in an intricate dance, pushing around electrons, changing zeros to ones and vice-versa, making sure that Bitcoin’s heart beats about a thousand times a week.

Living things have an interest in staying alive, and the Bitcoin organism is no exception. Bitcoin found an ingenious way to ensure that it stays alive: it pays people, as Ralph Merkle pointed out. People — and increasingly, organizations — are incentivized to keep it alive. They shape the physical world to Bitcoin’s liking, feed it energy, renew its hardware, and update its software to keep it alive.

The fact that Bitcoin pays us to keep it alive opens up a third space: a space of financial transactions, value, and mutual beneficial exchange. Let’s call this space “finspace.”

To understand finspace, we will have to examine the other side of this coin. So far, we only examined the side with an uppercase B: the Bitcoin network. But there is also bitcoin — with a lowercase b — which is the unit of value itself, brought into existence by every copy of the ledger.

These bitcoins, while deeply embedded in the amber of the ledger, are traded worldwide on various markets and marketplaces. And since these bitcoins — and their value — are critical for Bitcoin’s survival, we will have to recognize finspace as the third space this strange beast lives in. Note that finspace, strangely enough, is solely inhabited by bitcoin with a lowercase b.

In total, we can identify three distinct environments which the Bitcoin organism inhabits:

- Cyberspace: the world of ideas and code.

- Meatspace: the world of people and nodes.

- Finspace: the world of value and markets; the world of dollars and sats.

Understanding these habitats becomes increasingly important, especially as the climate in one — or more — heats up.

The Climates They Are A-Changin’

The three spaces outlined above — cyberspace, meatspace, and finspace — have different restrictions; different climates, so to speak. In short: they operate under different rules. Once these rules change drastically enough, people will say that “the political climate is heating up” and reports on “the coming financial climate” will be written. Citizens will be unable to speak and act freely. If things change drastically enough, people will rise up in protest, or, if all else fails, flee.

Cyberspace: While we don’t have precise words for it, it is obvious that the climate in cyberspace has changed quite drastically in the last two decades or so. The idealistic, utopian ideas which were the foundation of most of the internet were perverted by the advertisement-driven surveillance companies which are the giants of today.

People and politicians are slowly waking up to the strange reality we are living in: the fact that Facebook can manipulate moods and sway elections is as disturbing as the fact that Google knows you better than you know yourself. Edward Snowden showed that the most paranoid netizens were right all along: everyone in cyberspace is under constant surveillance, without suspicion, by default.

While the western world does not immediately feel the repercussions that come with living in a constant state of surveillance, Chinese citizens are gathering first-hand experience with each passing day.

In the western world, the consequences are advertisements which range from annoying to spooky. In China, the consequences are frozen bank accounts, an inability to buy train or plane tickets, elimination of creditworthiness, automated fines for trivial offenses, and more. Voicing the “wrong” opinion — online or not — can lead to restricted access to schools, hotels, and jobs. And after ruining your life with the flip of a bit you will be publicly named as a bad citizen and the government will take away your dog. If that doesn’t sound dystopian enough for your taste I bet that it will be in a couple of years. Remind yourself that this is only the beginning.

In the “free” world, things are more subtle. Multiple efforts are underway to curb net neutrality, the very cornerstone of the internet. Legislation is being passed which is inherently incompatible with the laws of cyberspace. It seems like the last battle of the Crypto Wars is yet to be fought as politicians are calling for “responsible encryption” and the ban of certain CAD files. Companies are in charge of the speaker’s corners of cyberspace and are making arbitrary decisions on what can be uttered by whom and what is off-limits.

Bitcoin knows no borders, no jurisdictions. However, it has to conform to the laws of cyberspace — and if these laws change, e.g. if large parts of the world block Bitcoin traffic and/or the usage of TOR, the Bitcoin organism will have to adapt.

Meatspace: Meatspace climate differs wildly from jurisdiction to jurisdiction. Some bastions of freedom still exist, but once you try to board an international flight it becomes obvious that your right to privacy and your freedom to bring a bottle of water with you are null and void.

Protests across the globe indicate that the powerless are fed up with the powerful, who do everything they can to stay in control and solidify their positions of influence.

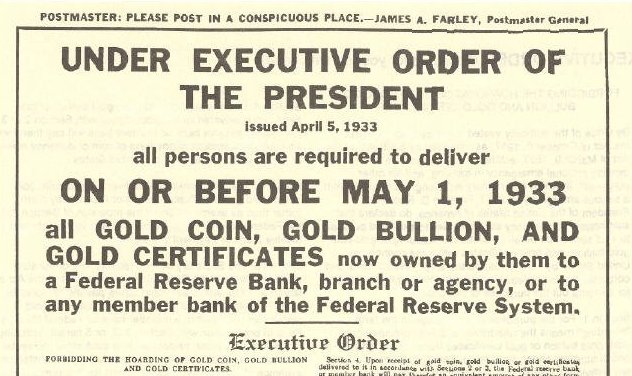

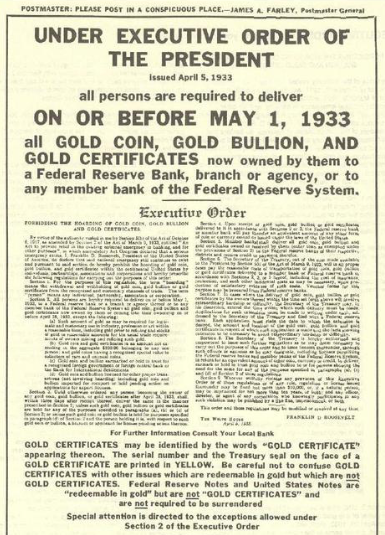

History shows that governments do not shy away from using their power. In 1933, Executive Order 6102 was signed, effectively forcing the whole population of the United States to hand over their gold and gold certificates to the government.

Yes, seizing bitcoin is way harder than seizing gold — in some cases even impossible. But it would surprise me if those who currently control our money — the governments and central banks of this world — would simply roll over and let Bitcoin march on unhindered. Governments have a monopoly on violence, and they are able and willing to abuse this violence in their own interest.

With Bitcoin, however, people can flee a country with their wealth intact. While this is definitely not easy, and not something I would wish on anyone, it is now possible.

Finspace: Where should I even begin? The current, debt-based financial system has an appetite for printing money which is beyond belief. Quantitative Easing (QE), Negative Interest Rate Policies (NIRPs), currency wars, hyperinflations, and a looming recession are just a few of the recipes of the global instability soup which is currently brewing.

The current financial system seems so far removed from common sense and reality, that all the jargon in the world won’t be able to stabilize this house of cards. People know that our money is broken, which is why they flee to buying real estate, stocks, and all kinds of complicated financial constructs to preserve their wealth. In the current system, you have to be an investment expert just to hold your value.

And we haven’t even talked about the looming recession, and the virtual inevitability of the next financial crisis yet. Yes, governments might be able to kick the can down the road by printing ever more money. But no road is endless, and the experiment which is fiat money will come to an end, one way or the other.

How bitcoin will react to a catastrophe in finspace is anyone’s guess. Some people might flee from their failing fiat currency into bitcoin, using it as a risk-off asset. Others might sell bitcoin to buy something they consider more stable, such as real estate or land. A rising number of people will identify bitcoin as the best money we ever had, shunning other assets and other monies on the quest to stack as many sats as they can.

However it might play out, Bitcoin is the cure for many of the current system’s ills. It is hard money which doesn’t devalue over time. It is an incorruptible system which forms the basis of a new financial reality.

“It can’t be changed. It can’t be argued with. It can’t be tampered with. It can’t be corrupted. It can’t be stopped. It can’t even be interrupted.” Ralph Merkle

In addition to the above, it seems to have many indirect effects. It lowers the time preference of those who use it. It incentives users to have better personal and operational security. It incentives individuals and companies to have better digital hygiene. It propels the development of chip manufacturing and encryption technology.

While Bitcoin definitely influences its environments and vice-versa, how Bitcoin reacts to drastic changes is yet to be seen.

Migration

Bitcoin lives on the internet, as Ralph Merkle points out. The internet, however, is not a necessary requirement for Bitcoin to work. Bitcoin is text — pure information — and every system capable of transmitting (and storing) information is a potential habitat for the Bitcoin organism. The internet just happens to be the most suitable habitat which currently exists, since it is the most efficient system to transmit information we have to date.

Cyberspace: The Bitcoin organism could migrate to other environments, and multiple efforts are underway which enable Bitcoin to spread to places where access to Internet infrastructure is limited or non-existent. As of this writing, Bitcoin transactions (and LN invoices) have been sent via radio waves, mesh, and satellite networks — just to name a few. All of these can be seen as Bitcoin conservation efforts, so to speak.

Whether we will see the migration of Bitcoin to another system in the decades and centuries to come depends, in essence, on whether the internet will remain a suitable habitat or not. If the online climate changes drastically enough, we might see the migration to even more resilient, less restrictive environments.

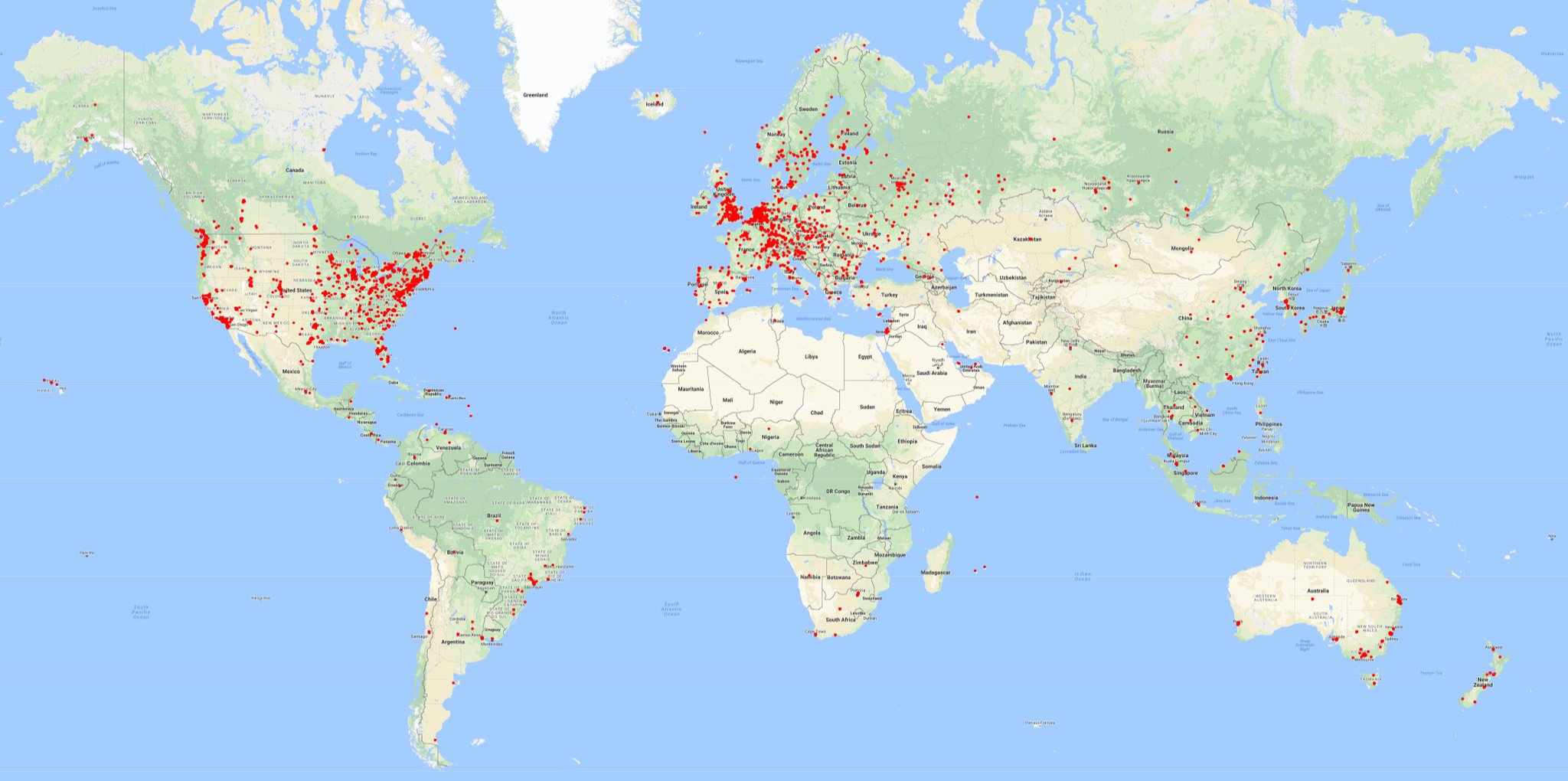

Meatspace: We can already see that mining facilities pop up where energy is cheapest or even stranded. In essence, mining is done where it makes the most sense — economically speaking. The same is true for running nodes. If people can run nodes at low risk and near zero marginal cost, they will. Thus, visualizing Bitcoin on a map, nodes and mining facilities migrate geographically from unfriendly places to friendlier places over time. Unprofitable mining facilities will shut down, profitable mining facilities will go online. The same, again, is true for nodes.

Public bitcoin nodes. Source: /u/SondreB

Public bitcoin nodes. Source: /u/SondreB

Increasingly, people will migrate to jurisdictions which are more favorable to their bitcoin holdings. And if you want to start a Bitcoin company, you might also move to a jurisdiction which is more favorable to you and your future business.

Finspace: In the last 10 years, many people decided to buy bitcoin, effectively feeding the Bitcoin organism by investing in it. This capital allocation will continue as more people understand the nature of this beast, and the ultimate goal of Bitcoin: the separation of money and state.

What investors describe as portfolio balancing and allocation of capital can be seen as a migration of value from worse assets to better assets; from bad stores of value to better stores of value. Bitcoin, being the ultimate asset in terms of portability, verifiability, divisibility, scarcity, and unseizability, will continue to suck up value and grow in the process.

Conclusion

Bitcoin lives at the intersection of three spaces: meatspace, cyberspace, and finspace. These spaces have different laws, different rules, and different climates. To fully understand any organism, we must not only look at the organism itself, but examine the organism-environment holistically.

Because of its decentralized nature, Bitcoin is able to overcome many, if not all obstacles in its environments. It can migrate to favorable jurisdictions in meatspace, use different transportation and storage media in cyberspace, and feed on the instability of other asset classes in finspace.

Whatever the future may bring, Bitcoin is equipped to survive and thrive in the various environments it lives in. It is remarkably resilient — well adapted to survive any coming storm, however perfect it may be.

Further Reading

- Proof of Life by Gigi

- The Sovereign Individual by James Dale Davidson and William Rees-Mogg

Acknowledgments

Bitcoin’s Social Antifragility

By Sven Schnieders

March 1, 2020

Secure Rules

I have argued in the past that the difficulty of changing the rules is one of the most important properties of Bitcoin. Without this security, which is in large part a consequence of decentralization, Bitcoin cannot function as a store of value. For a more detailed argumentation, I recommend reading my essay Mass Adoption of Bitcoin’s Values and this Twitter thread:

In this essay, we will take a look at why it is becoming less and less likely that these rules, e.g. monetary policy, are going to change in the future—even though it is already extremely unlikely. The reason is Bitcoin’s social antifragility. Unlike some other articles that cover the same topic, we will focus on the community and developers to find out why the social part of bitcoin’s antifragility is the most important one.

Antifragility

The term antifragility was coined by Nassim Nicholas Taleb and is used to describe the property of something that benefits from volatility and randomness. If you ship something which breaks easily, you label it “Fragile, handle with care!”. If on the other hand, you ship something robust—a large brick—you do not label it at all. In other words, the brick does not care about volatility. Most people assume therefore that robustness is the opposite of fragility. That is false, the opposite is antifragility. If you ship something antifragile, you label it “Antifragile, handle without care!”. The difference is that the robust—the large brick—does not care if it is thrown around; the antifragile wants to be thrown around—it benefits from volatility. Unfortunately, there is no concrete example of something that gets better by putting it in a box and “mishandling” it; there are however many things in socioeconomic life that work this way.

How the Coronavirus Strengthens the Restaurant Business

Let’s imagine that as a consequence of the recent Coronavirus outbreak, a lot more people eat at home and do not go out (I am oversimplifying the impact here but it is useful to illustrate the point). For this example, we will assume that the revenue of the restaurant business in NYC—all restaurants combined—suffers a decline of 50%. This is obviously bad for individual restaurants; they are fragile and do not like volatility—some of them will go bankrupt. It is however beneficial for the restaurant business as a whole. Why? Because of the survival of the “fittest”; the restaurants that do go bankrupt are the “weakest.” They are the ones that are struggling to survive even under normal conditions; the ones with few costumers, too high prices and bad food. After these bad restaurants have gone bankrupt, the average quality of the remaining restaurants is better and there is room for new ones. The reader should be aware that this distinction between “good” and “bad” restaurants is not objective; it is about being well adapted to the local market—delivering what the consumers want. Conclusion: the restaurant business as a whole is antifragile because the individual restaurants are fragile. (For more implications of antifragility and other great ideas, I highly recommend reading all books by Nassim Nicholas Taleb.)

Antifragility of Bitcoin’s Community

Bitcoin is profiting from the same antifragility as the restaurant business and NO2X is a great example of this effect. There was a heated debate in 2017 about doubling the block size of Bitcoin which ended in the BCash fork. Those who—wrongly—thought that increasing the block size is a great idea left Bitcoin for their own chain and most users who thought the same way switched as well. The fact that those people left made Bitcoin stronger as a whole. But what do we mean by saying it is now “stronger”? It means that after the BCash fork, the average commitment of the remaining community to the core values of Bitcoin was stronger. Those who understood the value proposition of Bitcoin—securing monetary sovereignty and liberty—stayed in Bitcoin and this understanding became the new baseline. Everyone who fundamentally disagreed with this value proposition, thinking—wrongly—it is about cheap and fast payments, left Bitcoin.

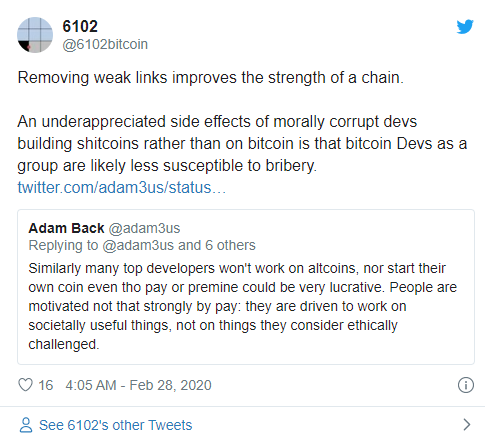

“6102” and Adam Back have pointed out that the same effect is responsible for making the current Bitcoin Core developers less susceptible to corruption and bribery; because if they were, they would have already switched to more lucrative “Altcoin” development. The developer community got stronger because the “weak links” left.

Stronger Bitcoin

Bitcoin became stronger through the 2X attack and the community is now more committed to its core values than ever before. As a consequence, a change in the rules that secure the core values is becoming increasingly unlikely.

As always, keep stacking Sats and hodling Bitcoin.

Ten Million Bitcoiners: The Intransigent Minority

By Cory Klippsten

Posted February 21, 2020

Not too many years from now, the number of Bitcoiners in the United States of America will cross ten million. When we hit that milestone, it’s game over: Bitcoin wins.

My favorite writer and thinker, Nassim Nicholas Taleb, wrote about “the intransigent minority” in his book Skin in the Game. Here’s the concept at work: almost every packaged food product for sale in the U.S. has a tiny U inside a circle printed outside. Very few U.S. residents require the kosher certification indicated by that U, but it’s easier for food companies not to have to make two separate lines for every product, so they generally make everything kosher. The rule, per Taleb: “A Kosher eater will never eat nonkosher food, but a nonkosher eater isn’t banned from eating kosher.”

For most observed complex systems, the minority contingent required to flip a population to comply with their intransigent view is in the 3 – 4% range. With a U.S. population of 325 million, 3% is 10 million.

For most observed complex systems, the minority contingent required to flip a population to comply with their intransigent view is in the 3 – 4% range. With a U.S. population of 325 million, 3% is 10 million.

A fintech fund that’s been in the Bitcoin space since 2012 recently ran intense analysis resulting in the best estimate I’ve seen for Bitcoin ownership. Just 7 million people globally are storing $100 of value or more in the Bitcoin protocol. For round numbers, let’s assume half of those people are in the U.S., and that one-seventh of those are above a more significant threshold like $2500. That’s just 500,000 U.S. citizens with a meaningful amount of Bitcoin. And of those, what percentage actually understand and care about Bitcoin to the point where they would fight for it? Let’s be generous and say 20%.

There are approximately 100,000 Bitcoiners in the United States. This means that just to get to “intransigent minority” levels, we need a 100x increase. This is why adoption dominates all other priorities for Bitcoin.

Bitcoiners have already knocked out so many potential attack vectors and handled so much FUD that there’s not much downside risk.

Another concept Taleb references throughout the five volumes of his Incerto is: Protect Your Downside. Bitcoiners have already knocked out so many potential attack vectors and handled so much FUD that there’s not much downside risk left for Bitcoin. But there is some, whether you handicap it at sub‑1%, sub-10%, or more. And by far the most threatening attack vector, in my opinion, would be a concerted effort of the U.S. government at many levels attempting to stamp out Bitcoin in an effort to maintain dollar hegemony across the globe.

Let’s be clear: Bitcoin would survive even the most concerted and vicious attack by the U.S. government. It might even thrive, Antifragile-style (another Taleb book), with people around the globe snapping up sats en masse as they witness the erstwhile hegemon lash out. But it could also play out differently, with a massive drop in network activity and value, thousands of individual lives irreparably disrupted, and the delay of our bright orange future by decades or longer.

This, to me, is unacceptable. That is why I have dedicated my life to recruiting the other 99% of our intransigent Bitcoiner minority here in the United States. There are 100,000 of us already. Help us recruit the other 9.9 million.

The Many Angles of Bitcoin Adoption

By Phil Bonello

Posted February 12, 2020

It might make sense just to get some in case it catches on. If enough people think the same way, that becomes a self fulfilling prophecy. – Satoshi Nakamoto, 2009

The data indicates that Bitcoin is catching on from a number of angles. As Satoshi pointed out in 2009, this creates a positive feedback loop.

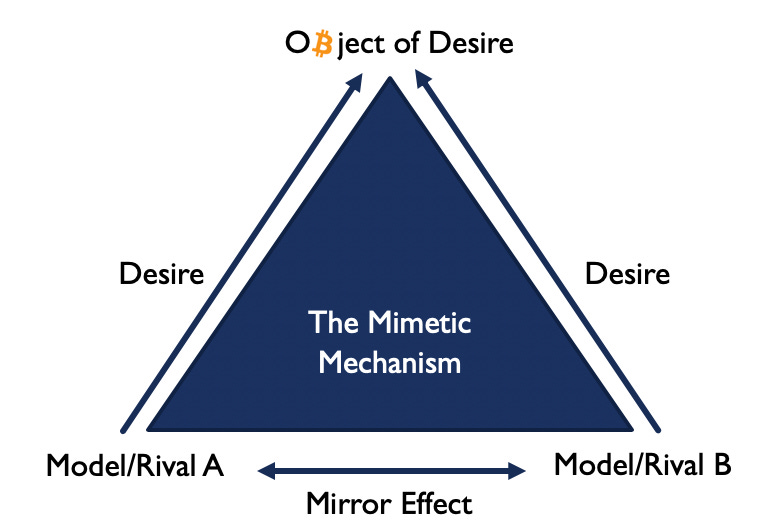

The acceptance and value of Bitcoin is largely based on imitation which can be explored through Rene Girard’s mimetic theory. We usually explain why we want something because it fits our unique preferences, or we highlight the objective good qualities something has. But in reality, we are frequently imitating others. We pattern our choices based on another’s example. This is also the nature of the monetization process.

This idea of imitation is key to Bitcoin’s value. Absent agreed upon frameworks to value Bitcoin, the price someone else is willing to pay is often the best signal one has to know what to pay. It’s self-referential and what makes Bitcoin’s price exceptionally reflexive. Following the picture above, when price rises, Rival A buys Bitcoin. Rival B is imitating Rival A, so Rival B also buys Bitcoin which then leads to Rival A buying more Bitcoin. This also works in reverse. As price falls, Rival A sells which triggers Rival B to sell and so on. This crowd mentality exists everywhere and has been especially true for Bitcoin. Crowds need a reason to exist.

For the Bitcoin crowd, there are many reasons.

Bitcoin is:

- A prisoner’s dilemma for nation states

- Digital gold - a money outside the reach of central banking

- An uncorrelated alternative investment with asymmetric upside

- A generational movement

- A tool for survival, social good, and dissidence, especially in autocratic regimes and hyper-inflationary economies

- A network that is driving the profitability of renewable energy initiatives

- The best performing asset of the decade

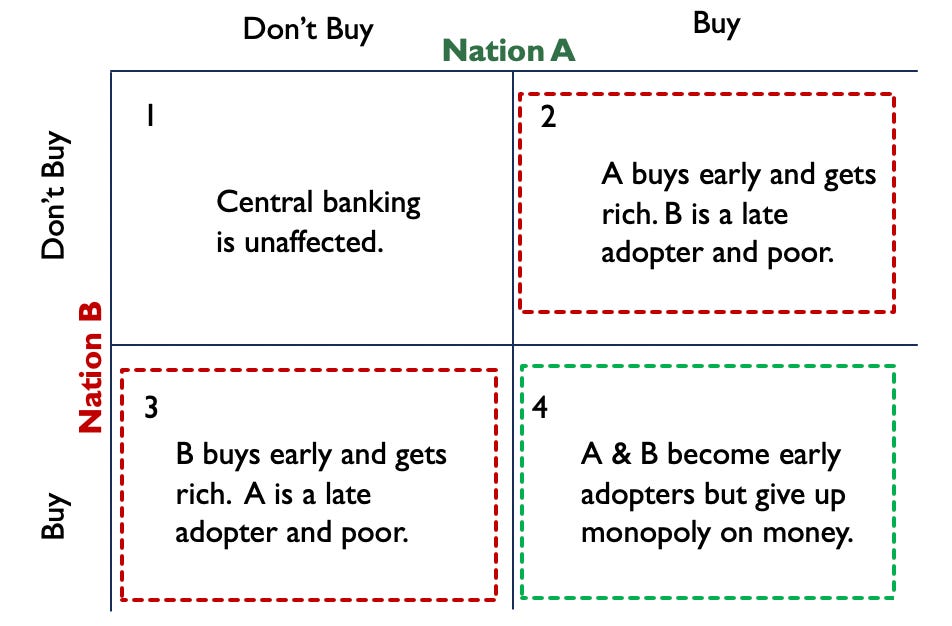

Bitcoin Presents a Prisoner’s Dilemma for Nation States

To start with the most controversial and least talked about adoption vector, Bitcoin presents a prisoner’s dilemma for nation states and their sovereign wealth funds. Of course, nation states would like to maintain control of monetary policy. But they have to participate in the Bitcoin game whether they want to or not.

- Quadrant 1: All nations agree not to buy Bitcoin. They can maintain the status quo – central banking.

- Quadrant 4: All nations buy Bitcoin. They benefit from price appreciation but lose control of money supply.

- Quadrants 2 & 3: Any nation buys Bitcoin, while others abstain. Those that abstain may be forced to buy later - the worst case scenario.

This is a forcing function. It only takes one sovereign wealth fund to set this in motion. Once a fund has accumulated its target amount, it simply has to make it known. Not only would this immediately put the fund in profit by initiating a cascade of buying from others, it would force other nations to consider making the same purchase. Nation states will experience intense fear of missing out.

This is a forcing function. It only takes one sovereign wealth fund to set this in motion. Once a fund has accumulated its target amount, it simply has to make it known. Not only would this immediately put the fund in profit by initiating a cascade of buying from others, it would force other nations to consider making the same purchase. Nation states will experience intense fear of missing out.

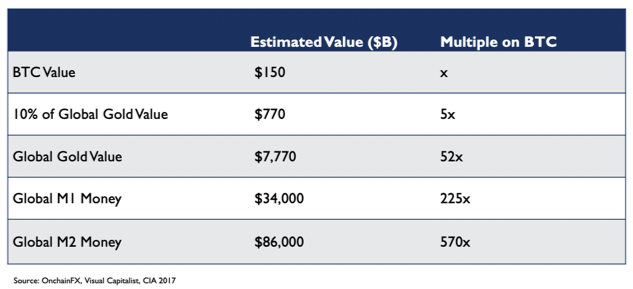

Bitcoin is Digital Gold

Bitcoin is money, a digital gold. As such, the target market is massive. If Bitcoin can achieve the market capitalization of gold, it would see over 50x return on investment. Bitcoin’s scarcity, acceptance, and portability make it an object of desire to gold bugs and central banking skeptics.

Scarce

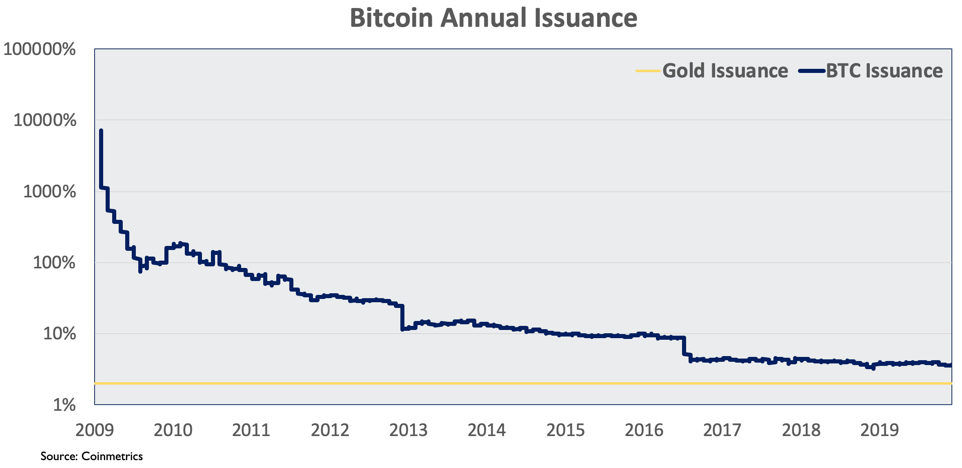

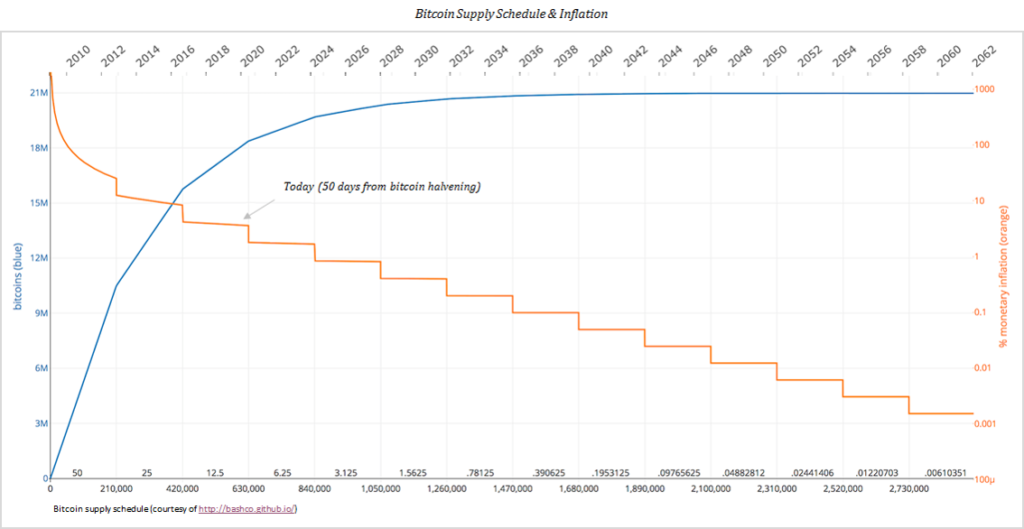

Bitcoin is compared to gold because it’s scarce. For thousands of years, gold has been used as a money and store of value because consistently, its annual issuance has hovered around 2-3%. It has maintained its purchasing power. Meanwhile, failed currencies range from Rai stones, to seashells, to copper, to countless attempts at paper money. If a money supply can be increased, it will be increased. Bitcoin has a capped supply of 21 million. The Bitcoin issuance decreases approximately every four years. Symbolically, 2020 is important because for the first time, we will see the annual issuance be less than that of gold.

Accepted

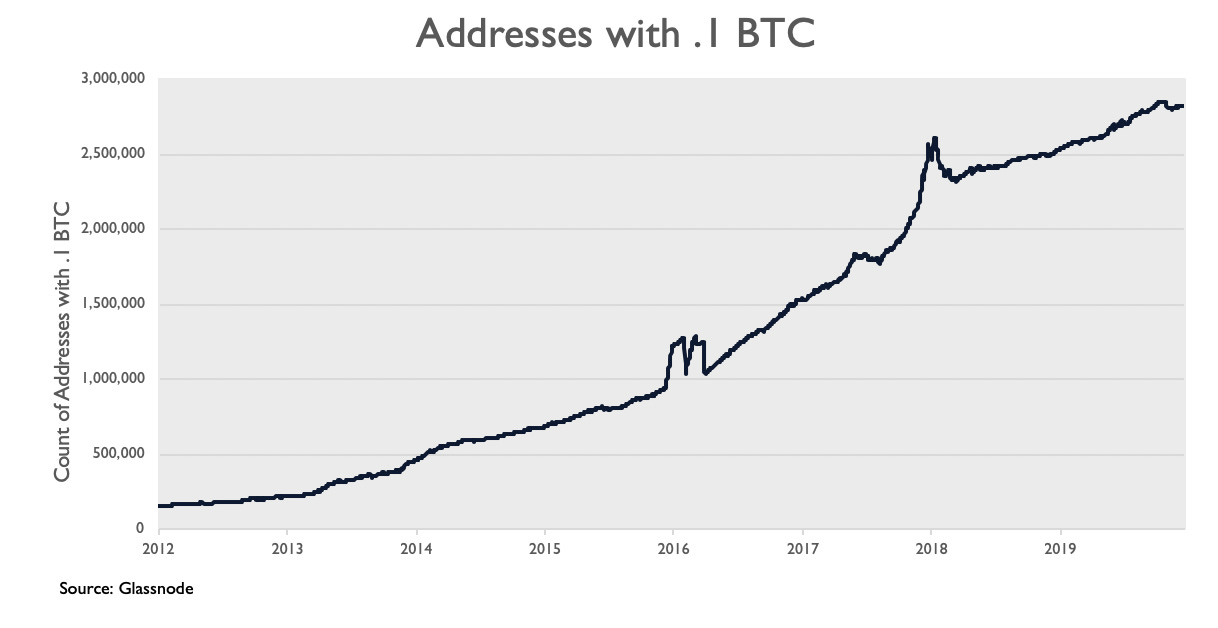

Data indicates that Bitcoin that more people than ever are using Bitcoin. This chart illustrates the number of addresses that hold a non-trivial amount of Bitcoin (.1 BTC). This measure allows us to filter out addresses with so-called dust balances. More people than ever are holding Bitcoin, and infrastructure is in place to make it easier for merchants to accept it as payment.

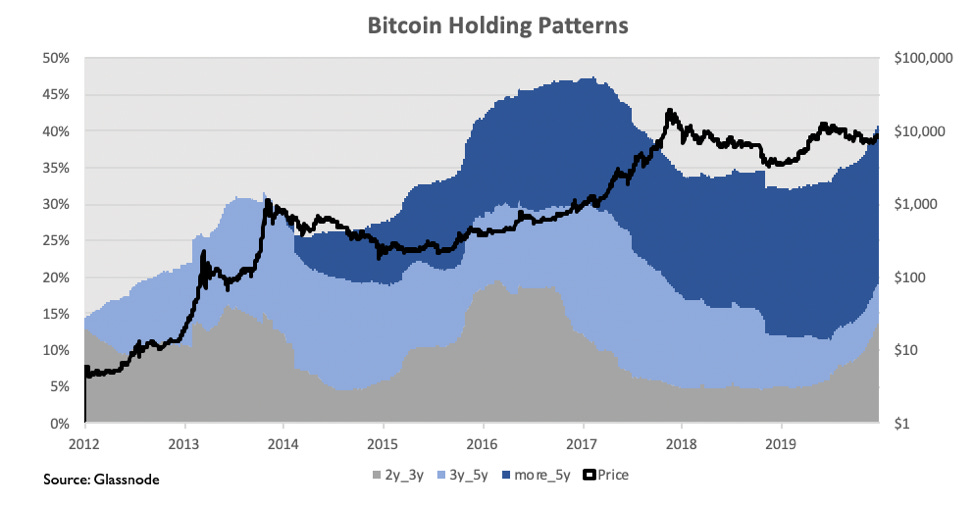

This chart shows Bitcoin holding patterns. Over 40% of Bitcoin has been held for two years or more, and that number is increasing rapidly. We can observe a similar patterns of accumulation before previous bull runs.

Portable

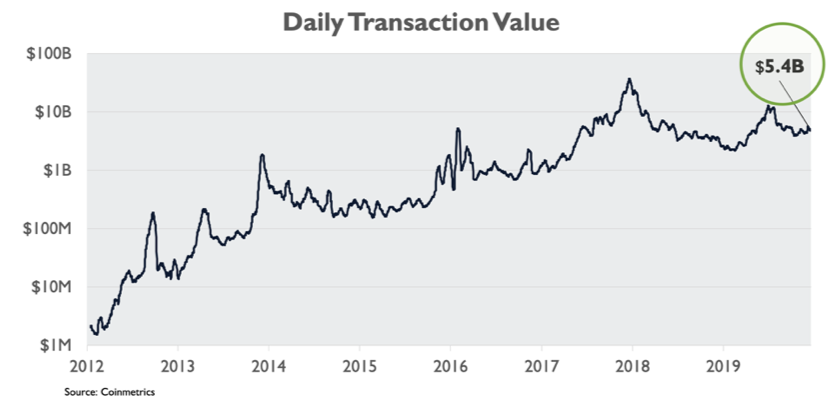

One of the biggest pitfalls for gold is its portability. It’s inconvenient for daily use but also expensive to move large quantities. In November of 2019, Poland repatriated 100 tons of gold, about $5 billion. Poland conducted a top-secret mission with a police escort, a helicopter, and a freighter plane for only $5 billion of gold. In a world that’s increasingly digital, we need a money that is digital and portable. Not only would the same transaction cost less than $1 and be completed in an hour, but the Bitcoin network handles over $5 billion each day! Over $7.5 trillion has been transferred throughout Bitcoin’s history. Bitcoin is portable in a time of rapid globalization.

Bitcoin is an Uncorrelated Alternative Investment

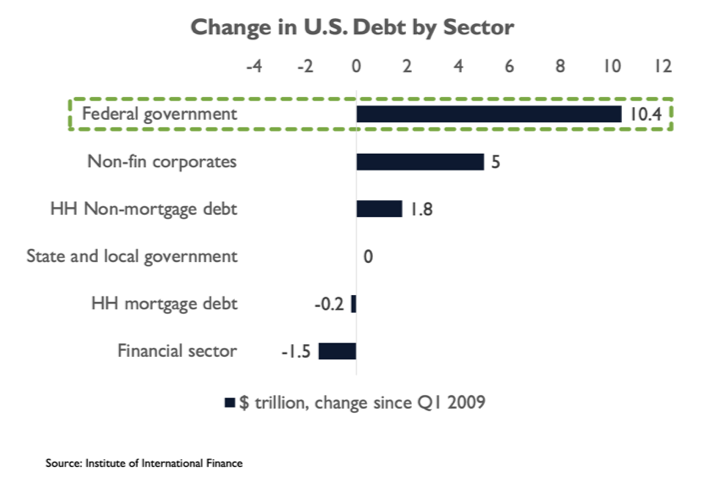

There’s $250 trillion in global debt and that trend seems unlikely to reverse. The United States federal government alone has added $10.4 trillion of debt since 2009. Central banks are forced to implement accommodative monetary and fiscal policy in hopes of tempering the debt bubble - $17 trillion in negative yielding bonds and counting. Investors are using Bitcoin as a hedge against currency devaluation while also decreasing the overall correlation within their portfolios.

Uncorrelated return streams are hard to come by. Bitcoin has been completely uncorrelated in the last five years. Investors have noted this as an intriguing characteristic of Bitcoin. Not only does it offer potential for great returns, but it is uncorrelated to major assets.

As more investors warm to the idea of Bitcoin as an uncorrelated hedge, career risk will decrease, institutional products will come to market, and firms will have the go-ahead to allocate. It’s reflexive.

Bitcoin is a Millennial Movement

Most convincing of all is the interest younger generations show for Bitcoin. They’ve grown up in a digital world, and they are comfortable with digital money. Gold is the reserve asset of Baby Boomers. Bitcoin is the reserve asset of Millennials. It represents a changing of the guard.

Millennials just became the largest US generation as of 2019 and are soon to be the largest generation in the world. They prefer alternative financial products - mobile banking, robo advisors, prepaid debit cards, emergency lending. They have grown up in a digital world and are comfortable holding money on their phones.

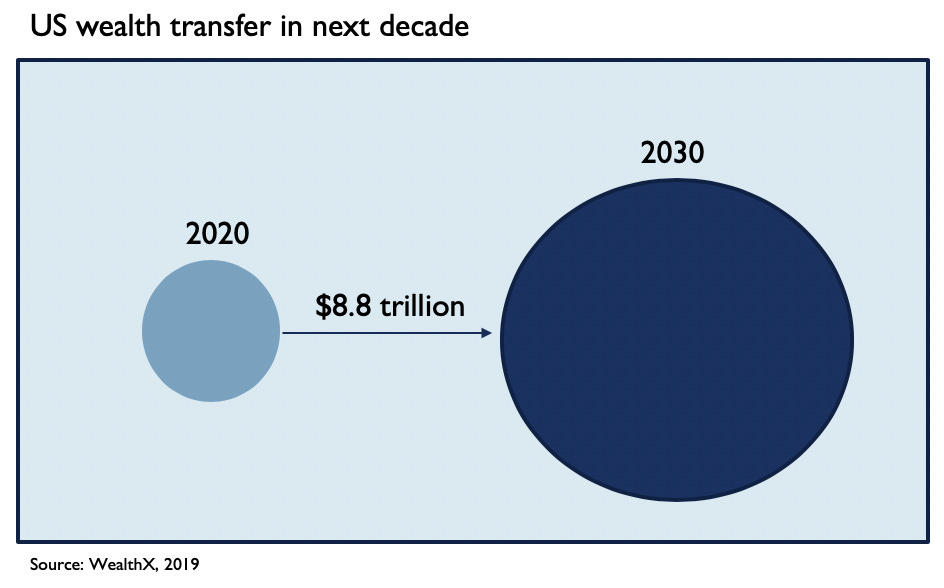

And in the next 10 years the younger generations are estimated to inherit almost $10 trillion. This does not even include the money millennials will earn as they enter their prime working years. This is the tip of the iceberg. Over the next 30 years, estimates indicate almost $70 trillion of wealth transfer.

And millennials are buying Bitcoin like crazy!

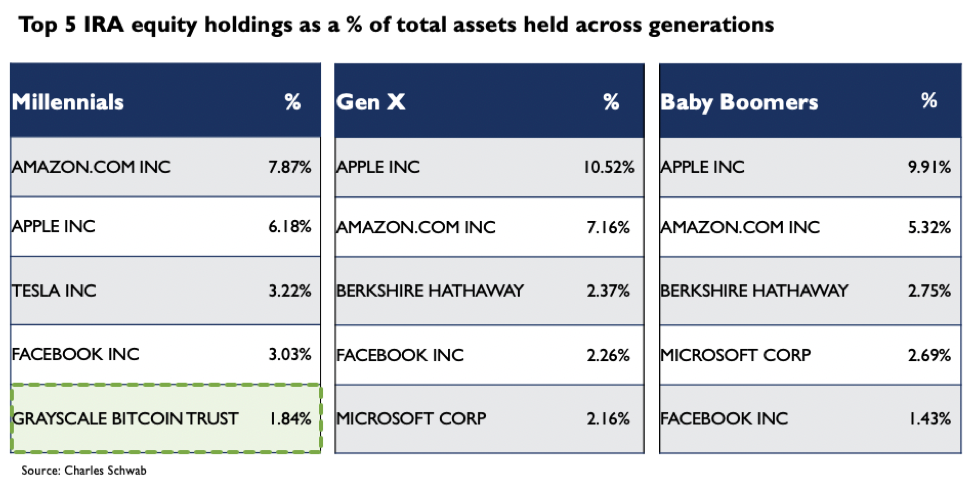

The data below shows the top 5 equity holdings as a percent of total assets across generations in Charles Schwab IRAs. Amazingly, millennials hold almost 2% of their assets in Grayscale Bitcoin Trust, a Bitcoin vehicle that often demands over 20% premium to spot. Not only are millennials interested in exposure to Bitcoin, but they are willing to pay a substantial premium.

As millennials enter their prime earning years and inherit enormous wealth, this Bitcoin buying should increase dramatically. Square “Bitcoin is resilient. Bitcoin is principled. Bitcoin is native to internet ideals. And it’s a great brand” – Jack Dorsey To further illustrate the connection between Bitcoin and millennials, it’s worth exploring Square, one of the companies at the center of the trend. Jack Dorsey, CEO of Square and Twitter, is an avid supporter of Bitcoin. And with $3.2 billion in revenue in 2018 (~50% increase YoY), Square’s business is growing quickly, especially with younger generations.

- 70% of users are millennial or younger

- 2x increase in first time Bitcoin buyers in Q3 2019

- 2 million merchants use the point of sale product

- 60 million Cash App downloads.

Square is on the path to providing end-to-end financial services for consumer and merchant that represent a massive portion of the population. Expect Bitcoin to be integrated into all of these services in the coming years.

Bitcoin is a Tool for Survival, Social Good, and Dissidence

“Africa will define the future (especially the bitcoin one!). Not sure where yet, but I’ll be living here for 3-6 months mid-2020.” – Jack Dorsey

Jack Dorsey also recently made a trip to Africa where he sees substantial opportunity. Africa is home to 7/10 fastest growing economies on earth and 1.2 billion people.

Nigeria also has the highest Bitcoin search volume since 2018. Comfort level with digital products, acceptance of alternative money/financial products, and their intrigue for Bitcoin shows interesting parallels to millennials broadly.

Currently, Africa’s GDP is only 10% that of the United States. Generally, Africa isn’t burdened by past technological success and is now in the throes of a technological revolution, leapfrogging personal computers in favor of internet connections through mobile phones. It’s plausible that we see Africa lead tech adoption over the next two decades.

Because currencies and banking infrastructure have been so unreliable, pre-paid minutes and services like M-Pesa have been used for the last decade to transfer value. Consumers are comfortable with alternative payment systems, simply using whatever works best. And increasingly, Bitcoin is the tool of choice.

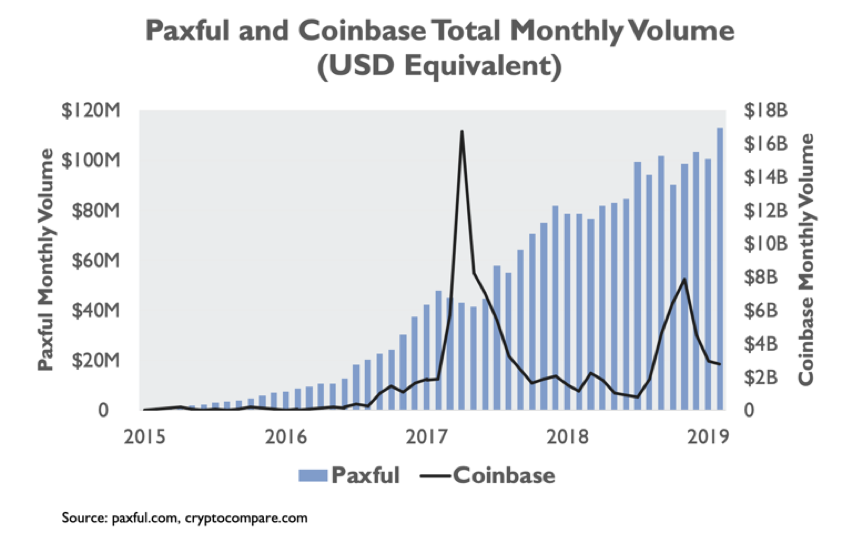

This chart shows monthly volume for Paxful vs Coinbase. Coinbase is the most popular US retail trading venue. Paxful is a peer-to-peer online exchange where Bitcoin is traded for direct bank transfers, gift cards, other goods or services, or cash. Paxful doesn’t require connection to traditional banking or regulatory infrastructure so it can service unbanked citizens in developing countries or authoritarian regimes. This chart is particularly interesting because it shows that organic demand for Bitcoin as a money is steadily growing while the trading volume on Coinbase seemingly follows price movements.

Necessity is the mother of innovation. It’s worth paying attention to how those that need this technology are using it.

Bitcoin is Driving Profitability of Renewable Energy

Critics opine on the wastefulness of Bitcoin mining. But contrary to popular belief, Bitcoin mining is emerging as a key driver of profitability for renewable energy.

From the perspective of those selling electrical power, Bitcoin miners have become the buyers of last resort. Energy economics in many countries have carved out a serendipitous niche for Bitcoin miners. Governments are forcing a transition from fossil fuels by subsidizing renewable energy. These subsidies have resulted in over-production of renewable energy. This over-production has outpaced transmission capacity. Because energy storage at scale is still inefficient and uneconomical, this forces power plants to sell electricity at substantially reduced prices. This has become a boon for Bitcoin miners and power companies. Miners buy power at a discount by locating themselves near the plants, and the power companies have buyers of excess power that would otherwise go to waste. Unsurprisingly, companies are taking advantage of the opportunity.

In the fall of 2019, two companies announced funding to launch mining operations in the U.S., specifically to capitalize on these dynamics. Layer1 raised $50 million led by PayPal founder, Peter Thiel. The goal is to launch a vertically integrated operation that utilizes wind energy in Texas. Crusoe Energy raised $70 million, $40 million in financing and $30 million in equity. This raise was led by Bain Capital Ventures. Crusoe provides solutions to oil and gas companies to reduce flaring and repurpose the energy for mining and cloud computing.

Environmentalists – from foes to friends!

Bitcoin is the Best Performing Asset of the Decade

Finally, Bitcoin is the best performing asset of the decade. From fractions of a penny to over $9000 today, millions of percent of appreciation all without a central team managing its success.

This price performance is inescapable. If you are paying attention to markets, you know the Bitcoin story. The price increase and the resulting wealth that some have gained, attracts others. Once again, the is reflexive.

Conclusion

Bitcoin is catching on from multiple angles. Sovereign wealth funds are forced to consider the Bitcoin prisoner’s dilemma. Gold bugs are forced to consider Bitcoin as a worthy digital counterpart. Institutional investors are forced to consider Bitcoin’s low correlation and its status as a reserve asset. Baby Boomers are forced to consider the preferences of future generations. Developed nations are forced to consider the adoption trends in developing nations. Environmentalists are forced to consider the positive impact that Bitcoin mining has on renewables. And everyone has to consider Bitcoin’s meteoric rise.

Once more from Satoshi…

It might make sense just to get some in case it catches on. If enough people think the same way, that becomes a self fulfilling prophecy. – Satoshi Nakamoto, 2009

Tweetstorm: On Adversarial Thinking

By Ragnar Lifthrasir

Posted January 12, 2020

A thread/rant on the the importance of thinking critically and adversarially about Bitcoin claims and ideas, and the dangers of failing to do so.

This isn’t directed at anyone specifically so please don’t make it personal. Let’s stick to ideas and arguments please

Below is an example of robotic repetition of unquestioned simplistic dogma as a mantra of faith and an excuse for inaction and critical thought.

In this instance it’s HODLmonomania. (Yes I HODL and recommend it). The danger of this monomania is what follows from it…

- Don’t develop and use @btcpayserver, a self-hosted, open-source bitcoin payment processor to build a circular Bitcoin economy. Just HODL.

- Don’t develop and use the Lightning Network to give better privacy for censorship resistant and faster payments. Just HODL.

- Don’t build a network of people to informally buy and sell bitcoin to escape the KYC/ AML and surveilled 3rd party Bitcoin exchanges. Just HODL.

- Don’t use bitcoin to pay for Bitcoin products and services to spread adoption of bitcoin, create a circular bitcoin economy, and offer an alternative to exchanges to acquire bitcoin. Just HODL.

We can see how reducing all of Bitcoin to one monomania keeps bitcoin from progressing, gives an excuse for inaction, narrows the scope of Bitcoin’s purpose and abilities, and discourages rigorous intelligent discourse.

Memes are for humor, not orthodoxy.

Here’s an example of an extraordinary claim, that feels good to believe, but lacks empirical support and isn’t evaluated with common sense.

If you owned all the BTC currently in circulation, 18,144, at today’s price of $8,087, then you’d have a net worth of $147 billion. Jeff Bezos is worth $131 billion. From when he started Amazon & it was worth $0 to today he had a “wealth transfer” of almost the market cap of bitcoin

There’s many more extraordinary claims about Bitcoin that require extraordinary evidence, or at least critical thinking, but lack either. These claims have become givens, unquestioned, and widespread.

Some other examples: Lightning Network can replace Visa and MasterCard. Bitcoin solves inequality. Bitcoin will become the world’s reserve currency. Bitcoin will end wars. Bitcoin will prevent governments from collecting taxes at a mass scale.

As much as we hope some of these claims come true (I do!) we make bitcoin weaker by burdening bitcoin with unrealistic expectations, setting up bitcoiners for disillusionment, and lulling into inaction and dangerous overconfidence.

Humility is the beginning of wisdom.

To make Bitcoin and ourselves stronger we need to think like the software engineers who contribute to Bitcoin. They peer review, mercilessly seeking flaws. At their tech events they talk about every which way a proposal can fail. They think adversarially. They’re conservative

Stressing muscles makes them stronger

Testing & reviewing codes reduces the risk of exploits

Thinking critically about ideas & claims focuses our limited resources on what’s realistic & achievable. It also helps us let go of future fantasies to focus on the present.

Tweetstorm: On Cheating

By Dhruv Bansal

Posted March 3, 2020

\1 “Bitcoin is a game we play where we can easily tell when someone is cheating.”

When I first saw this (in some ELI5 bitcoin Tweet) I thought it just some pithy phrase.

But over time this simple sentence has come to resonate with me as a profound summary of the bitcoin ethos.

\2 Bitcoin IS a game, but an infinite one, where the goal is to keep playing – not a finite game where the goal is to win.

“Finite games are theatrical, necessitating an audience; infinite ones are dramatic, involving participants”

\3 Like any game, bitcoin is an opt-in set of rules devised by its players.

Once the game has begun, changing rules is tough. Only rules which help players continue playing will survive. And no one is in charge of making changes.

So, like the game of culture, Bitcoin evolves.

\4 Preventing cheating is important in infinite games because cheaters are seeking to win, not to continue play.

Cheating in bitcoin isn’t prevented by referees (3rd parties) or parents (the state).

Mathematics, energy & the greed of other players ensures the game continues.

\5 Imagine other games if they were like bitcoin:

- A news industry in which those with the incentive to lie don’t because it’s more profitable to tell the truth.

- Societies which don’t pollute because it’s cheaper to be clean.

- Making people free making people money.

\6 Yes, bitcoin is deadly serious with big fortunes, egos, and ambitions in play.

But thinking of it as an infinite game can help engender the playfulness required for creativity, innovation, progress.

To a beautiful game…

So You Think Bitcoin Mining is Wasteful?

By Daniel Frumkin

Posted March 5, 2020

Much has been said in the past couple of years about the amount of electricity consumed by Bitcoin mining. In fact, negative environmental impact has become one of the go-to talking points for Bitcoin pundits to criticize the digital currency.

However, data provided without context can be very misleading, and this is often the case when journalists write about Bitcoin mining. The total (estimated) energy consumption is indeed quite high, and still growing rapidly as the network hash rate continues to climb. However, the real world impact is frequently misrepresented and misunderstood.

In this article, we’ll be comparing the electricity consumption of Bitcoin mining with all of the world’s videogame consoles and computers. Then we’ll discuss the difference in typical electricity _sources _for the two and their respective environmental impacts.

Let’s begin with an update on the most common of comparisons: Bitcoin vs. countries.

Bitcoin’s Electricity Consumption Relative to Countries

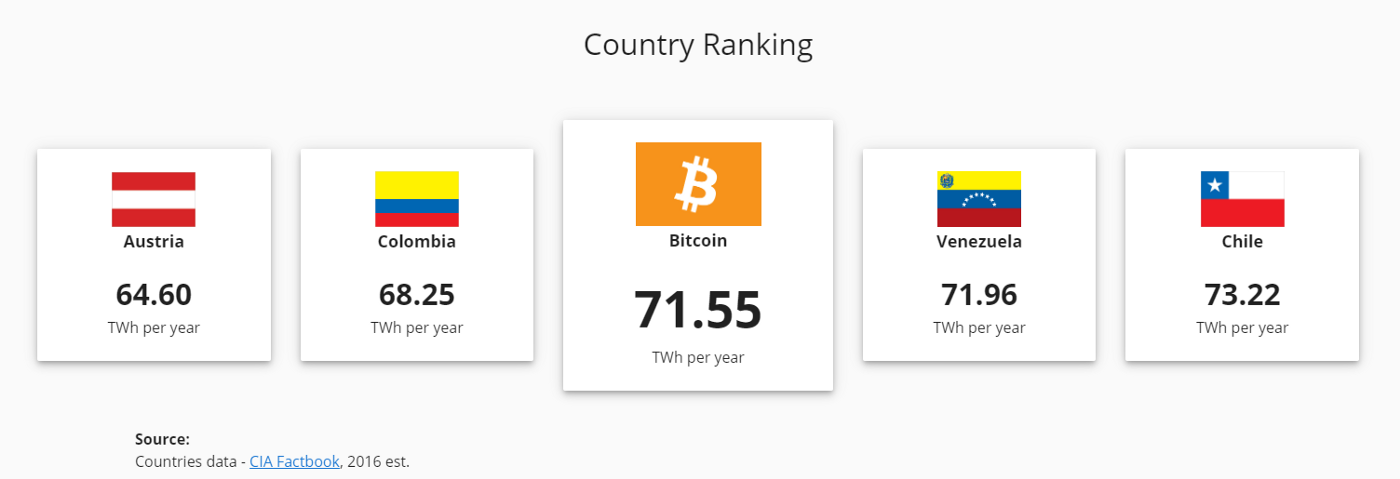

It became popular around 2017 to compare Bitcoin’s total electricity consumption with that of entire countries. To that end, the University of Cambridge created a handy tool called the Cambridge Bitcoin Energy Consumption Index (CBECI) that tracks annualized electricity consumption of Bitcoin mining and makes interesting comparisons to provide some context.

As of November 2019, Bitcoin’s estimated energy consumption is in the same range as Colombia, Venezuela, and Chile.

It should be noted, however, that this is still asmall amount compared to the top global electricity consumers: China (5564 TWh per year) and USA (3902 TWh per year).

Now let’s get to the real comparison we want to know about…

Bitcoin vs. Video Games — Electricity Consumption

First, it’s important to clarify that the following calculations are estimates with potentially high error margins.

Bitcoin mining’s energy consumption varies depending on the total network hash rate and the efficiency of each mining machine being used. For example, producing 100 Eh/s with only the newest and most efficient ASICs would consume substantially less electricity than, say, 100 Eh/s with only ASICs from 2017 and earlier.

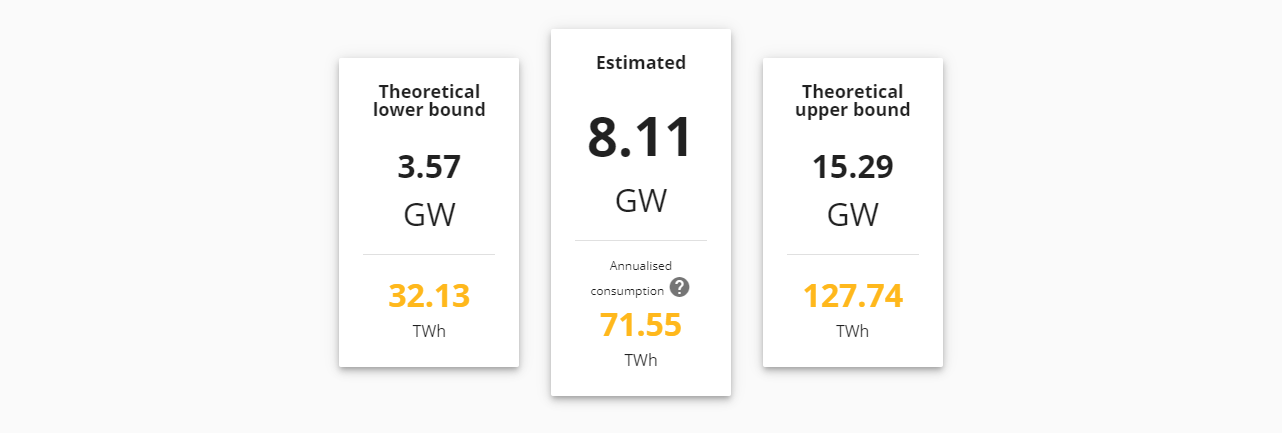

With that being said, CBECI has a rather robust methodology for calculating electricity consumption, so we feel comfortable using their estimate of 71.55 TWh per year as of November 2019.

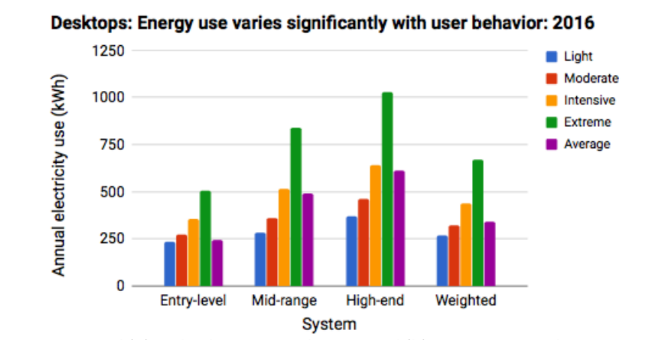

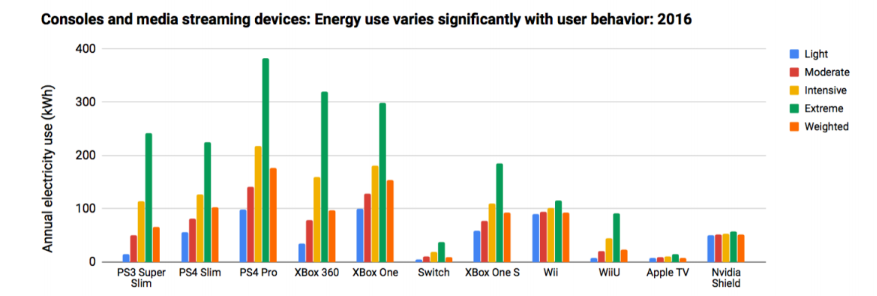

Global electricity consumption of video game playing is substantially more difficult to estimate. For one, there is a large diversity of devices that are being used for gaming. Consoles such as the PlayStation 4 and Xbox One consume less electricity than high end gaming computers such as a Digital Storm — Velox, so treating all gameplay equally will not be remotely accurate. On top of that, there is the extra complication that gaming consoles and computers don’t run 24/7, unlike Bitcoin mining machines.

Accurately estimating the energy consumption of video game playing around the globe requires consideration of these factors and many others. In fact, it’s well beyond the scope of this simple blog article. Fortunately, a team of researchers at Lawrence Berkeley National Laboratory carried out an incredibly thorough research study on the energy consumption of video game playing in California in 2018. They took into account factors such as the popularity of various gaming systems, their respective efficiencies, typical user behavior, and much more.

You can get a better idea of the thoroughness of their methodology from the graphics below calculating the weighted consumption of a wide selection of gaming systems based on typical user behavior.

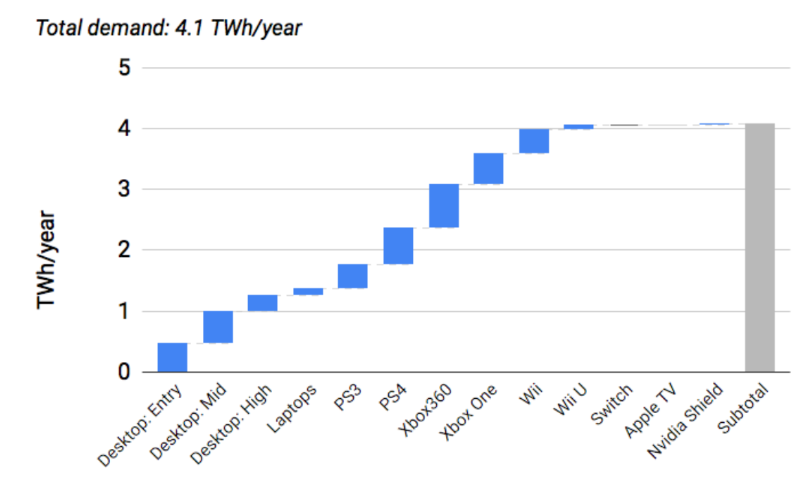

Ultimately, after taking all of this data into account, the research team concluded that the annual consumption of video game play in the state of California for 2016 was approximately 4.1 TWh per year.

Now, our only remaining task is to somehow extrapolate that estimate to cover video game playing for the entire world. (This is a good time to reiterate that these estimates have a high potential error margin.)

First, we need to use the estimate from California to come up with an estimate of the total United States consumption. California’s population is approximately 40 million people, while the whole of the US population is approximately 327 million. If we assume that the behavior of video game players in the rest of the US resembles California, then we can simply multiply California’s 4.1 TWh/y consumption by the ratio 327/40. From that, we get 33.5 TWh/y as the total consumption for the USA.

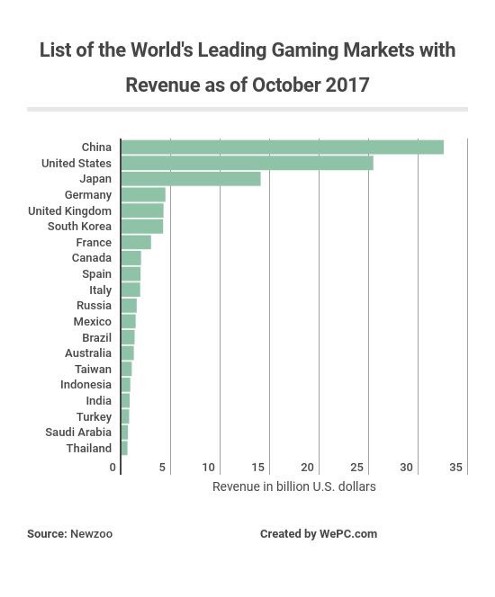

Next, we’ll use data collected by NewZoo and presented in WePC’s 2019 Video Game Industry Overview to further extrapolate for the total energy consumption of video game playing worldwide. In this case, data about revenue is far easier to come by than more nuanced data about the number of gamers around the world and their typical user behaviors. (Note that according to NewZoo, “the revenues are based on consumer spending in each country and exclude hardware sales, tax, business-to-business services, and online gambling and betting revenues.”)

Considering that the US accounts for 32% of global gaming revenue, we’re going to make the (admittedly far from perfect) assumption that it also accounts for about 32% of global energy consumption from gaming. In that case, we arrive to a grand total of 104.7 TWh per year consumed by video game play worldwide.

So What’s the Takeaway?

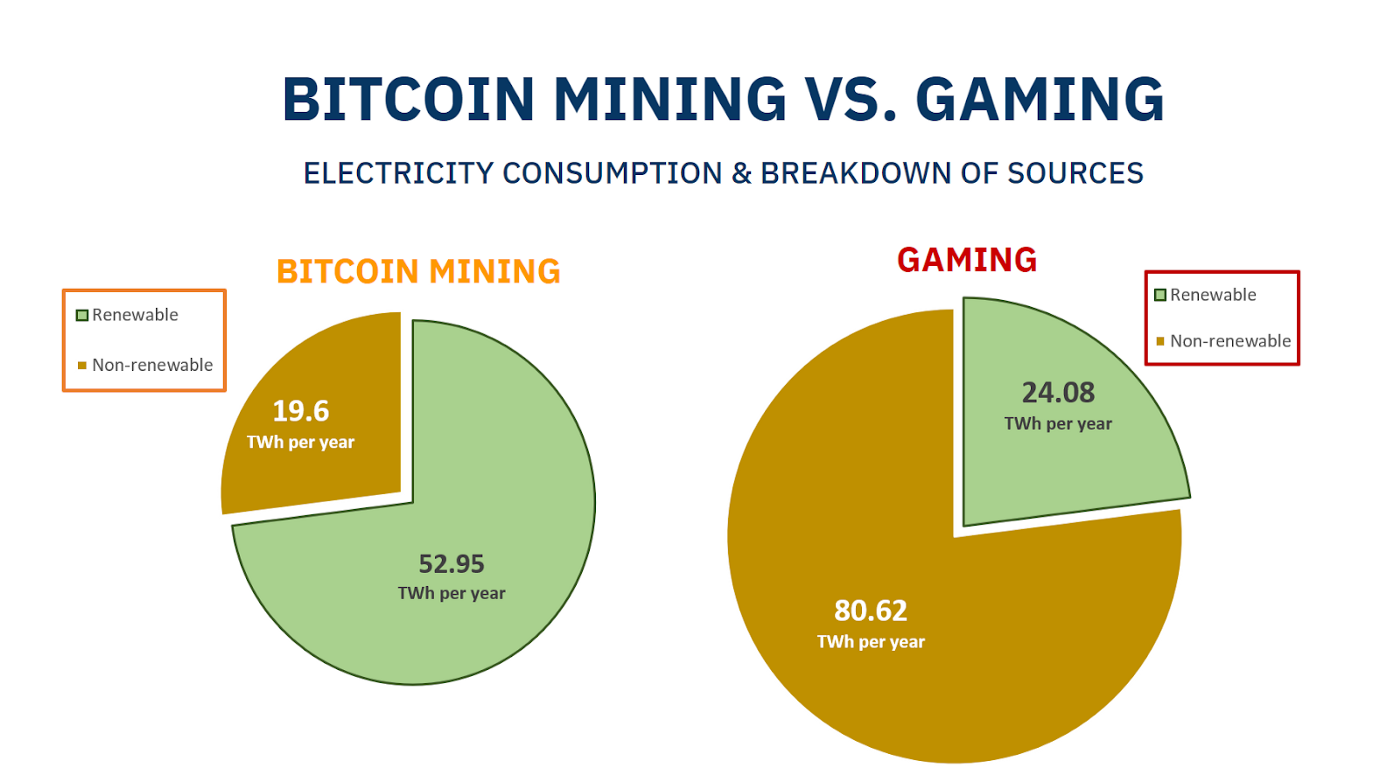

Based on our very rough estimates, we found that the worldwide electricity consumption of people playing video games is 46% higher than the total consumption of Bitcoin mining as of November 2019. However, since these are such imprecise estimates, the bigger takeaway is simply that the two amounts are pretty close to each other. This provides much better context as to the true scope and impact of modern day Bitcoin mining than comparing the annualized energy consumption directly to small countries.

But it’s even more important to understand _where _that energy is coming from. In their June 2019 report, the cryptocurrency investment and research firm CoinShares estimated that more than 74% of all Bitcoin mining electricity comes from renewable energy sources. In fact, about 50–60% of the total hash rate comes from Sichuan province in China during its wet season due to the abundance of cheap hydropower there, much of which would otherwise go unused because it is difficult to store and transport. When the wet season is over, many miners move their operations elsewhere to harness cheap thermal and wind power.

The reality is that access to cheap electricity is a necessity in order for miners to compete long-term. With this economic incentive to find the lowest cost electricity possible, many miners have set up shop in rural locations where excess renewable energy is produced. This is simple supply and demand: the supply in these locations is high, and the demand is practically nonexistent since the excess energy is so difficult to store and transport to urban areas where there are consumers.

On the other hand, the US Energy Information Administration estimated that only 23% of the world’s electricity generation came from renewable sources in 2015. Since the majority of video game playing likely occurs in urban areas, it’s reasonable to guess that the same 23% figure is a decent estimate for the amount of renewable energy powering gameplay. In that case, we get the following breakdowns.

Explore More

As Den Held explains in his article, Proof of Work is Efficient, “Bitcoin is a super commodity, minted from energy, the fundamental commodity of the universe. PoW transmutes electricity into digital gold.” To put it another way, Bitcoin is like the batteries we don’t yet have, capable of storing excess energy and carrying its value through time.

Are there any other topics related to Proof of Work and Bitcoin mining that you’d like us to cover? Let us know by leaving a comment below or tweeting @braiins_sytsems @slush_pool.

Stop Treating Bitcoin as Risky. It’s a Safer Asset Than Most

By Jill Carlson

Posted March 5, 2020

This article was written by Jill Carlson on March 5, 2020 and was originally published on Coindesk

People think I got into bitcoin (BTC) because I have a high risk tolerance.

Actually, I got in because I have a low risk tolerance for worst-case scenarios.

Bitcoin is often touted as a risky bet. It is nascent. It has only been around for about a decade. It is poorly understood by mass markets. It is an experiment. It could still fail. All of these claims are true. In many ways, the risk profile of bitcoin resembles that of an early stage startup. Bitcoin appears to be hovering between the trough of disillusionment and the slope of enlightenment. This means that most people continue to view cryptocurrency as kind of crazy. It’s a gamble.

THE ROAD TO HAVING BITCOIN UNDERSTOOD AND VIEWED AS A SAFE HAVEN IS A LONG ONE, DEMANDING DEEP INVESTMENT IN EDUCATION.

These dynamics mean that investors often bucket bitcoin as a risk asset. It gets put in the same category as high-growth stocks, high-yield debt, high-beta exchange-traded funds, venture capital investments and emerging markets.

Markets broadly have two modes: risk-on and risk-off. In risk-on scenarios, when markets are confident and things are moving higher, risk assets tend to outperform safe havens. When the markets are risk-off, safe-haven assets like gold, treasury bonds and cash fare better, and are often the only investments trading higher as investors sell out of their riskier positions.

Whether a financial product is a risk asset or a safe haven depends on a number of properties. In some cases it depends on the fundamentals of the asset. Share price is a reflection of the projected future cash flows of the business, which in turn depend on dynamics like customer demand. The dynamics can make companies more or less subject to movements of the markets. In other cases, the categorization of a given asset might depend on supply and demand dynamics. Gold, with its relatively fixed supply and consistent demand from entities like central banks, is resilient to market cycles and downward shocks. In all cases, however, I would argue that what matters most in understanding asset correlations and behavior is market perception. Do traders and investors view the asset as a good place to hunker down in volatile markets? Or do market participants view the investment as vulnerable to the downside, but also prime to participate in boom cycles?

The markets certainly still seem to view bitcoin as the latter. And as far as the price of bitcoin is concerned, and as far as any market correlations are concerned, that perception is all that matters.

Via Jill Carlson

Via Jill Carlson

This perception misses bitcoin’s most important properties. Bitcoin is, in many ways, the ultimate safe haven asset. It can be self-custodied, so even when systems of trust and rule of law breaks down, it can be held. It is open and borderless, with relatively liquid markets in every country in the world. It is censorship-resistant, meaning no government nor institution can, practically speaking, prevent investment or transaction in bitcoin. Bitcoin has a fixed supply, much like gold. Bitcoin is digital, which makes it practical to hoard, hold and transport. For doomsday preppers, dystopian sci-fi fans and apocalypse predictors, there is a lot to like about bitcoin.

Yet, if we look at the behavior of the bitcoin price over the last couple of weeks, as concerns over a global pandemic have ramped up, it is clear that bitcoin continues to behave more like a high-risk investment than like the safe haven which it promises to be.

Do the markets have it wrong? Should bitcoin be more correlated with gold than with Apple stock? Maybe. But as John Maynard Keynes put it, “The markets can stay irrational longer than you can stay solvent.” The road to having bitcoin understood and viewed as a safe haven is a long one, demanding deep investment in education. What matters is the narrative around the asset, and right now the narrative around bitcoin is that it is an early-stage, high-risk bet. As far as the markets are concerned, that perception is reality.

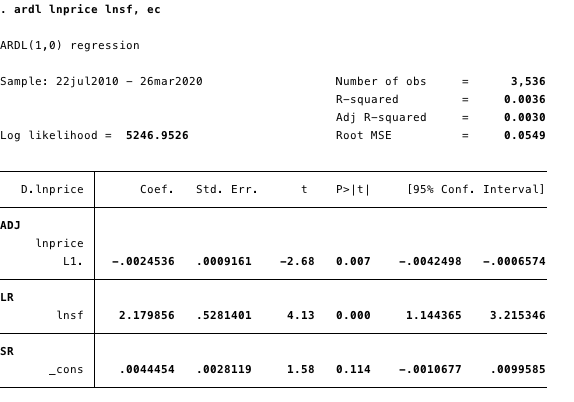

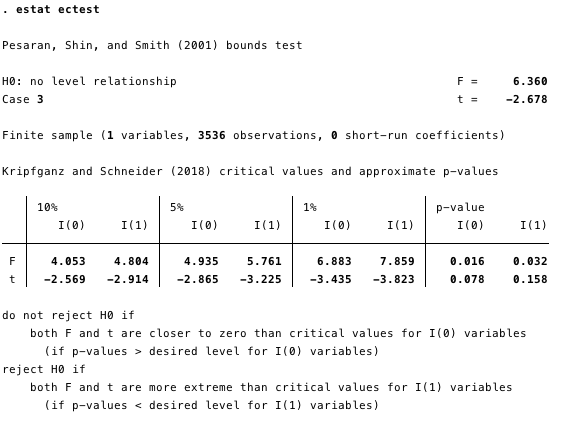

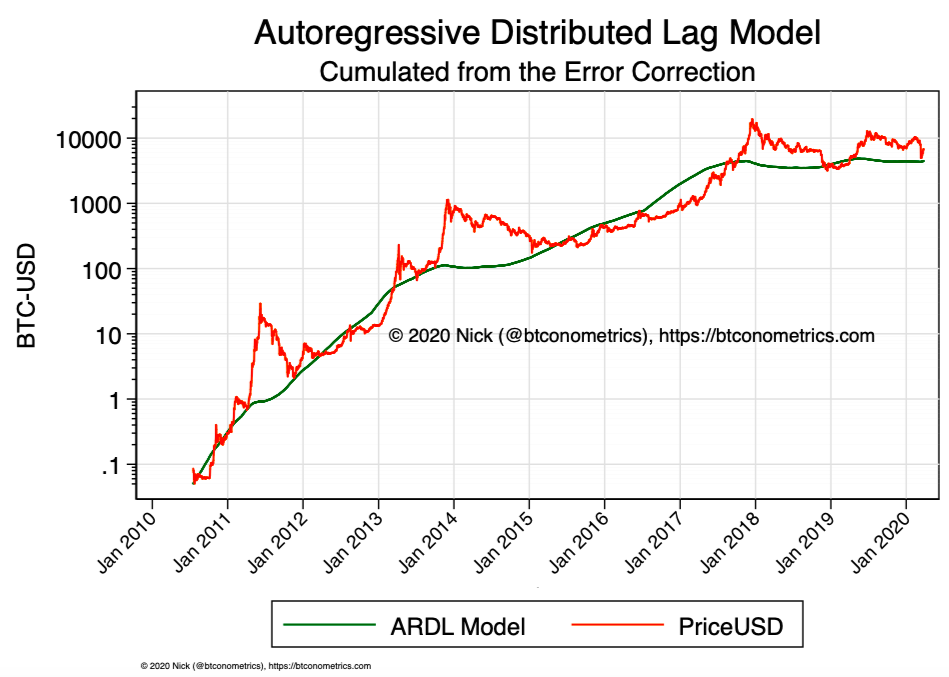

Reviewing “Modelling Bitcoin’s Value with Scarcity” — Part IV: The Theoretical Framework leading to the Error Correction Model

The next step after the shown cointegrating relation between stock-to-flow and market cap of bitcoin

By Marcel Burger

Posted March 7, 2020

Introduction

In my first review of the work of PlanB, I concluded that the relation between stock-to-flow and bitcoin price as pointed out by the author was invalid because the general assumptions of ordinary least squares regression were not met. When two variables are non-stationary and we estimate a regression model, there is a good chance we find highly autocorrelated residuals and a significant value for the coefficient. This phenomenon is well known as spurious regression. But, spurious regression isn’t always the case. Sometimes the variables might be cointegrated, which would imply that the estimated relation is super consistent. Nick pointed out that we could very well be dealing with the exceptional case of cointegration and showed that he wasn’t able to falsify the cointegrating relationship between stock-to-flow and bitcoin’s market cap. After Nick showed that the variables were cointegrated, I verified his findings. Since I still was skeptic, I chose to run the analysis on my own dataset and ran three different cointegration tests to make sure there was no doubt. Even though I expected I would be able to show that at least one of those tests would lead me to reject cointegration, I could not. Initially, I was a bit too fast with drawing my conclusions and as a result I warned people that the model was flawed. So, I offered my apologies in public for drawing a wrong conclusion and engaged in many discussions to explain why the model was eventually right. Because I noticed in those discussions that the basis underneath the material we discuss is poorly understood by most people, I decided to start writing a book that will help people to better understand the econometric concepts we’re dealing with. To stay in the loop about that development, I recommend subscribing at www.bitcoinometrics.io to get notified once the book is available. But that’s not what this piece is about. This piece is about further development of the model and presenting a framework which helps to understand the developments. In the process of writing my book I also conduct some academical research. Not only to refresh my mind on time series analysis, but also to check with academical researchers if there were any important developments in that field of research. Nick in his write up already mentioned the Vector Error Correction Model (‘VECM’) and estimated the coefficients for the model as part of his attempt to falsify cointegration. In my ‘hunt for cointegration’ I also touched on it without estimating any of the model coefficients, but I ended the article by stating that setting up a VECM would be a nice subject for a follow up article. This is still work in progress, but I like to share a bit more on how we actually get to that point and how to go about.

Model Selection Framework

Usually when one is looking to quantify the relation between non-stationary time series, the first step is to difference the series until a stationary series is found. This is basically the first thing you learn as an Econometrics student when you follow classes on Regression Analysis or Time Series Analysis. But differencing the time series to make them stationary is only one possible direction to come to a solution. And it comes at the cost of throwing away data that might identify long run relationships between the time series.

Another possibly better solution is to test whether the time series are cointegrated. If the cointegration test tells us cointegration exists, we can set up a model that is able to describe both the long run relationship and the short term corrections.

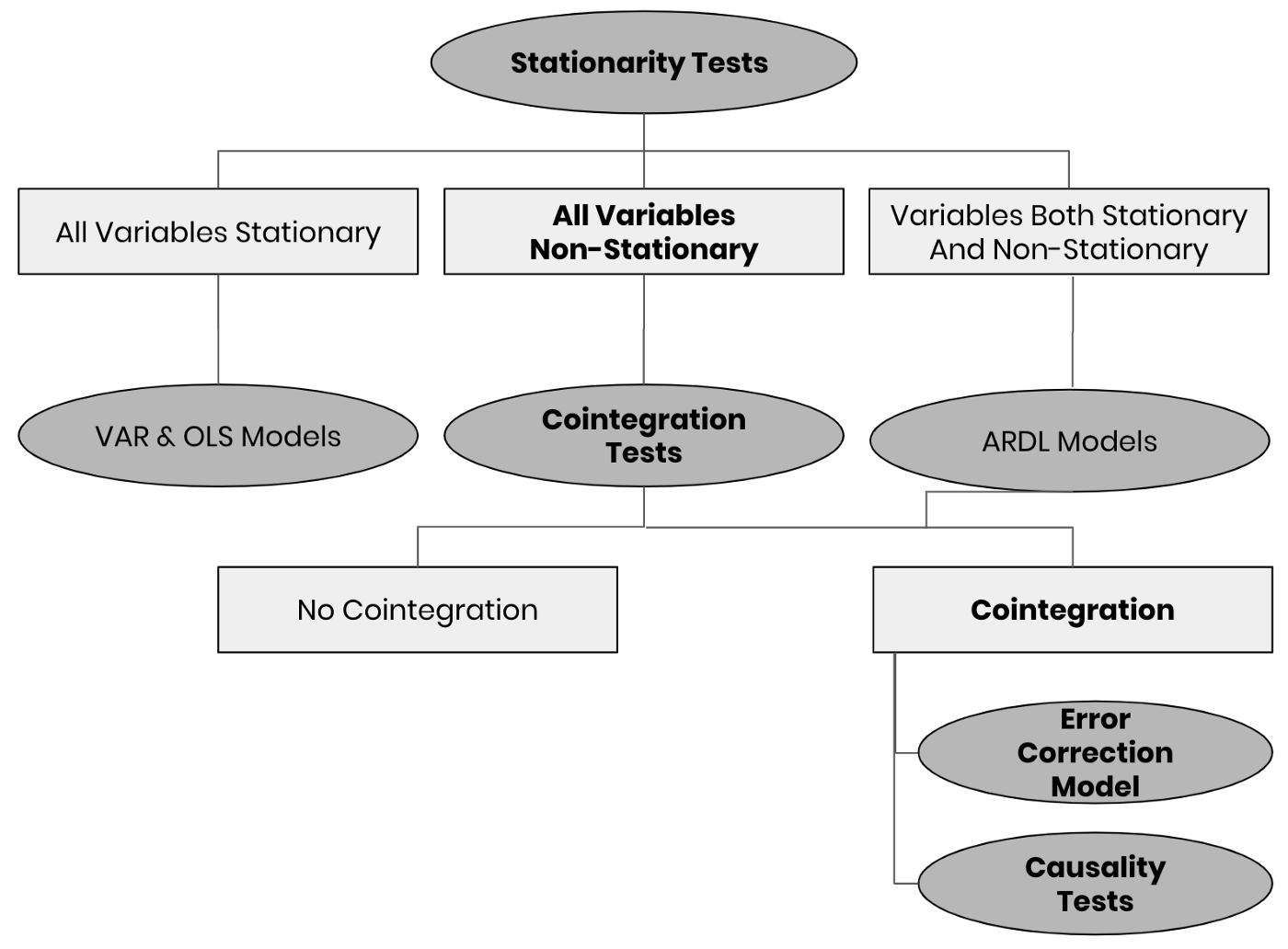

One of the things I noticed in the literature is that it’s hard to find a basic method selection decision tree. I like to attack these kind of problems as structured as possible, so that the chance of actually finding meaningful relations increases while you also prevent yourself from misspecifying a model. In my search for a helpful framework, I found this useful article.

The framework as shown below is my slightly adjusted version that is based on the one I found. It will serve as a guide in the steps we will take. All the shapes that contain bold text, show the path we follow in case we like to construct a model to quantify the relation between stock-to-flow and price (or market cap). In the earlier articles (here and here) Nick and I both independently showed that both variables are first order integrated (after applying differencing we end up with a stationary series over time) and that cointegration couldn’t be rejected by running different tests.

Fig 1: Simplified Model Selection Framework for time series analysis

Fig 1: Simplified Model Selection Framework for time series analysis

Note that even though the overview above is far from complete, it offers a useful overview for those models that are often used. Most practitioners who use linear regression models, just go straight to the OLS models without even testing for stationarity. Using frameworks like these would be beneficial to many of them. It also helps people with less of a statistical background to check whether the beautiful model they have been introduced to was indeed the appropriate model to use.

Please also note that this overview is only about model selection and not about estimation of the model. I like to emphasise again that this overview is very simplified.

We found cointegration. Now what?

As cointegration couldn’t be falsified, this means that the two variables are linked to form an equilibrium relationship spanning the long run. One of the issues though with the different cointegration tests is that some of them have weaknesses. Johansen (1988) addressed those and came up with an improved cointegration test model, which is widely applied nowadays and incorporated in many different econometric software packages. Both Nick and I used that test in our model validation and we concluded that the model as introduced by PlanB couldn’t be falsified.

If both the variables are first order integrated and there exists a cointegration relationship then we can derive an Error Correction Model. When both variables are put into a vector this can also more generally be referred to as a Vector Error Correction Model (‘VECM’).

Following the framework

First, I set up all the different equations, and briefly touch upon them. Keep in mind that the long term relation is what matters most in terms of showing us the road, and realise that the short term corrections are modelled to return to the middle of the road. In order to run a full blown analysis we need to define:

- the linear model

- the cointegration representation

- the error correction models for both S2F and BMC

- the models to run causality analysis

Setting up the model equations

If we consider the logarithm of bitcoin market cap (‘Log(BMC)’) as _Y _and we consider the logarithm of stock-to-flow (‘LogS2F’) as _X, _then the relationship between the two is written as:

Equation 1: The Linear Model

Equation 1: The Linear Model

Based on the representation theorem of Engle and Granger (1987), we rewrite the equation to display the cointegrating relationship:

Equation 2: Cointegration Representation

Equation 2: Cointegration Representation

Since both variables have their own Error Correction Models, I introduce them here:

Equation 3: Error Correction Model for bitcoin market cap

Equation 3: Error Correction Model for bitcoin market cap

Equation 4: Error Correction Model for Stock-To-Flow

Equation 4: Error Correction Model for Stock-To-Flow

The first expressions at the right hand side of the Error Correction Model equations indicated by ⍺ are both stationary white noise processes for some number of lags _l. _In case we look at only at one period lag, the equations become:

Equation 5: Error Correction Model for BMC with one lag.

Equation 5: Error Correction Model for BMC with one lag.

Equation 6: Error Correction Model for S2F with one lag

Equation 6: Error Correction Model for S2F with one lag