Bitcoin is Not Too Slow

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

Bitcoin is Not Too Slow

By Parker Lewis

Posted August 23, 2019

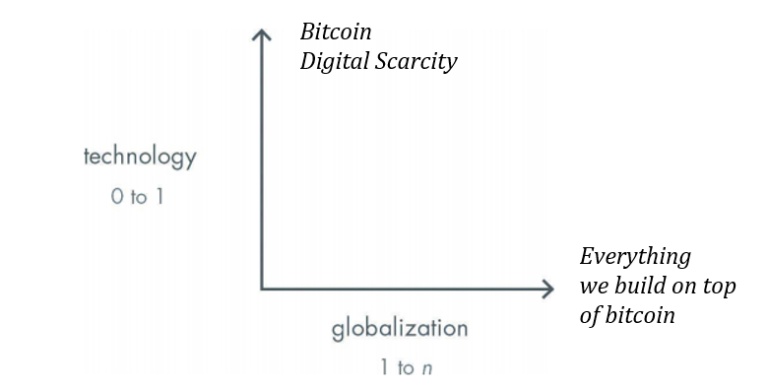

In Peter Thiel’s Zero to One, he outlines the impact new technology has on building a non-zero sum future. While the book is focused on individuals and companies, bitcoin as a monetary system is the ultimate zero to one technology leap. For historical examples, Thiel highlights the advent of the steam engine as well as the shift from typewriters to computer processors among others. He also articulates a view that innovation has largely stagnated since the early 1970s, while noting that technological progress since then has been more 1 to n than 0 to 1. Bitcoin fixes this. Bitcoin’s innovation is not only zero to one; it is fundamentally distinct from the class of innovation that is the focus of Thiel’s book. Bitcoin is a monetary protocol built on digital scarcity, the impact of which will be far broader than steam engines and computer processors.

Bitcoin fixes this

There’s a new meme floating around the internet; whatever the problem, bitcoin fixes this. Negative yielding debt? Bitcoin fixes this. Wealth inequality? Bitcoin fixes this. Endless global war? Bitcoin fixes this. Financial crises? Bitcoin fixes this. Rage culture? Bitcoin fixes this. We’re not exactly sure how just yet, but it’s an articulation of the balancing effect a sound and stable monetary system will have on every aspect of society. Money is the coordination function of society. It allows hundreds of millions of people to cooperate who otherwise would not have a basis to do so. And, bitcoin is the tool that will allow for more peaceable coordination because it is both unmanipulable and devoid of moral hazard. How it globalizes is the “1 to n” problem (not in the express sense as Thiel describes), but the solutions to scale bitcoin will naturally be incremental. The non-zero sum collective benefit that follows may not literally cure every ill in the world, but the invention of a step-function change monetary network is fundamentally different than any single product because money is the economic good that coordinates all other economic activity.

“The problem is precisely how to extend the span of our utilization of resources beyond the span of the control of any one mind; and therefore how to dispense with the need of conscious control and how to provide inducements which will make the individuals do the desirable things without anyone having to tell them what to do.” – F.A. Hayek, The Use of Knowledge in Society

Hayek writes about the invention of money and the price mechanism as the tool that allows society to dispense with the need of “conscious control.” Bitcoin is the superior successor to this mechanism, and its zero to one innovation is digital scarcity, not payments or speed of transactions. While bitcoin’s property of scarcity still needs further stress testing, it is a profound achievement and what makes bitcoin unique. Never before bitcoin has any asset, let alone a digital one, been finitely scarce; the end result of its innovation is the hardest form of money that has ever existed. That is the zero to one achievement and a phenomenon that almost certainly will not be repeated.

Every other problem that bitcoin will have to overcome is more pedestrian relative to scarcity. Digital payments? The idea that human ingenuity can create digital scarcity but that we then cannot layer on payments technology does not logically follow. Payments technology is just one of the many 1 to n innovations that will be built on top of bitcoin to globalize its adoption. Not only are payments easier to solve, it is also not a critical path that needs solving today. The primary use case for bitcoin today is as a savings mechanism, not payments. Over time, as adoption increases and as more infrastructure is built, bitcoin will evolve into a more transactional currency, but that process will occur gradually, not suddenly. And as the shift occurs, bitcoin adopters will continue to leverage legacy monetary systems and legacy payments rails.

Not a Payments Rail

The bitcoin blockchain will never be a layer for mass payments, but there is a considerable amount of debate on this topic. Many hold the view that for bitcoin to be “successful” it needs to be a one-stop shop, combining the roles of currency issuer, settlement layer and payments rail. While bitcoin fulfills the first two functions beautifully (currency issuer + settlement layer), it is categorically not a payments rail. Both for reasons of speed and scale, bitcoin fails the payments test. The good news? We don’t need the bitcoin network to be a payments rail.

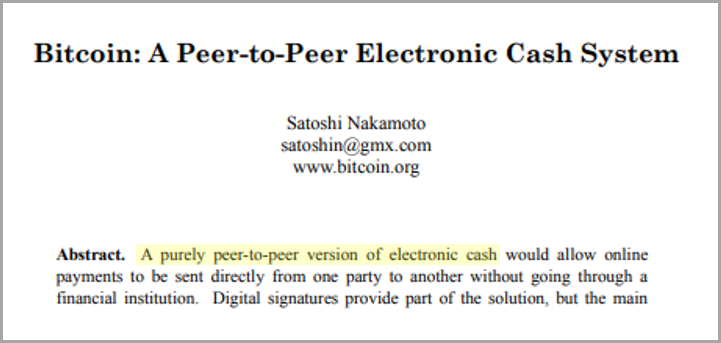

Much of the confusion in the philosophical (rather than technical) debate stems from the opening salvo of the bitcoin whitepaper: “a Peer-to-Peer Electronic Cash System.” Peer-to-peer has been interpreted by some to imply that bitcoin needs to be able to handle every last transaction in the world between any two peers. Separately, others believe that if bitcoin transactions cannot occur at the scale or speed of Visa or Mastercard, it is structurally flawed. Essentially, according to skeptics, if bitcoin cannot meet both of these standards, it fails on its promise. Thankfully it does not.

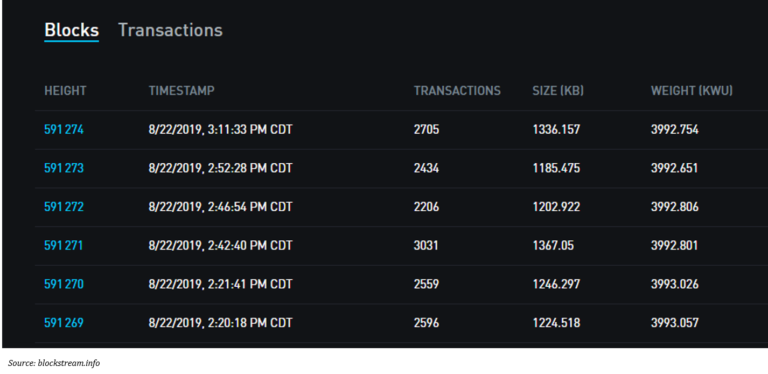

For additional background, bitcoin blocks are solved every 10 minutes *on average; however, bitcoin blocks are not solved precisely every 10 minutes on a fixed schedule. The next block may be solved in 1 minute or 20 minutes, 30 seconds or 36 minutes. The network adjusts such that blocks are solved on average every 10 minutes. How could a merchant or transaction processor live in a world either this slow or unpredictable? Separately, bitcoin blocks have a limited amount of space to include transactions. While there is not a fixed transaction capacity in bitcoin by count, each bitcoin transaction consumes a limited amount of block space; as a function of limited capacity, blocks include approximately 2,700 transactions on average. With ten-minute average block intervals, six blocks per hour, 24 hours per day, 365 days per year, that equates to a network capacity of approximately 145 million transactions per year which is the equivalent of approximately 4.6 transactions per second. Visa on the other hand processes 124 billion transactions per year at a rate of ~4,000 transactions per second (see here).

How can bitcoin be the purely peer to peer engine that powers the global financial system, if it operates at nearly one one-thousandth the scale and speed of Visa alone? The reality has always been that, if bitcoin were to have a non-zero value, the consequence would be a system so valuable that any base layer would not be able to handle all transactions without sacrificing decentralization or censorship resistance. Without these properties, bitcoin would not be a zero to one innovation and its value function would break down. Ultimately, the bitcoin protocol layer provides the function of currency issuance and final settlement, but it is not capable of storing every small purchase, including your Starbucks, for the rest of time for everyone.

If it were the latter, all transactions by all people, no matter how big or how small, would have to be validated and stored by every other person on earth. Without a mechanism to align the interests of network participants, a tragedy of the commons problem would exist and the end result would be a less secure currency system subject to centralization. Instead, we accept a mechanism to limit transaction throughput at the base layer, shifting aspects of bitcoin’s peer-to-peer transactional architecture to separate layers that integrate with bitcoin. These tradeoffs have been made in order to secure the foundation of bitcoin’s monetary system (decentralization → censorship resistance → fixed supply).

]

]

Many point to this text from the bitcoin whitepaper released by its pseudonymous founder as evidence that bitcoin was always intended to fulfill every payment by every possible network peer. It does say “purely peer-to-peer” after all. However, more important to bitcoin than anything written in this summary (or any interpretation) is bitcoin’s consensus mechanism. Everything critical in bitcoin is enforced by a consensus of network participants, including its fixed supply and ultimately the capacity within each bitcoin block, which limits the number of transactions it can process. This is the fundamental difference between bitcoin and the legacy financial system: monetary policy by consensus rather than by fiat. Bitcoin’s founder created a system that ultimately removed critical decisions from any central authority, instead deferring to the wisdom of market consensus. It is a system that is flexible enough to be adapted but rigid enough that any material change is very difficult. As a consequence, network peers have to decide, on a decentralized basis, how best to scale bitcoin. It is through this consensus mechanism that bitcoin dispenses of the need for “conscious control.”

Security Trade-offs

Everything comes with trade-offs. In bitcoin, there are two holy grails: a fixed 21 million supply and preventing the currency from being spent multiple times (the double spend problem). The value of bitcoin is derived from its ability to secure both of these functions on a decentralized, trustless basis and both are inextricably linked to bitcoin’s fixed network capacity. Think of the capacity within each bitcoin block as valuable digital real estate. All market participants seeking to clear bitcoin transactions have to compete for block capacity. Scarcity in network capacity is the function by which bitcoin’s shared resource is optimized. Or, think of it as bitcoin’s solution to the tragedy of the commons. Competition for this scarce resource ensures that the resource is used efficiently and that its value is maximized. Ultimately, scarcity causes market participants to compete with each other, bidding up the value of the network’s capacity, rather than shifting negative externalities on to the rest of the network.

In bitcoin’s free market, the highest value and most profitable transactions are prioritized. Without scarcity in transaction capacity, this value function would break down. It is less important that we optimize for transaction capacity and more critical that scarcity exists. No one really knows the optimal amount of transaction capacity at any point in time, partly because demand is ever changing but also because it is generally growing over time. The critical piece is that capacity is known and scarce, which allows market participants to plan and ultimately, to compete. The commons is never depleted; instead participants compete and innovate to figure out how best to utilize a scarce asset. Scarcity ensures that the commons is not abused and creates a predictable rate of growth in the overall size of bitcoin’s blockchain, which ultimately protects and promotes decentralization.

As discussed in a prior edition (see here), miners secure the bitcoin network by devoting real world energy resources to run cryptographic hashing functions and to solve bitcoin blocks. By solving blocks, miners validate history and clear current transactions which are then checked and validated by the rest of the network. In return, miners are paid in bitcoin. Devote resources to secure the network and get paid in the network’s native currency (bitcoin). The actual compensation paid to miners comes in two forms: newly issued bitcoin and transaction fees. In order to devote resources today to secure the network, miners have to reliably expect that aggregate compensation will hold its value into the future.

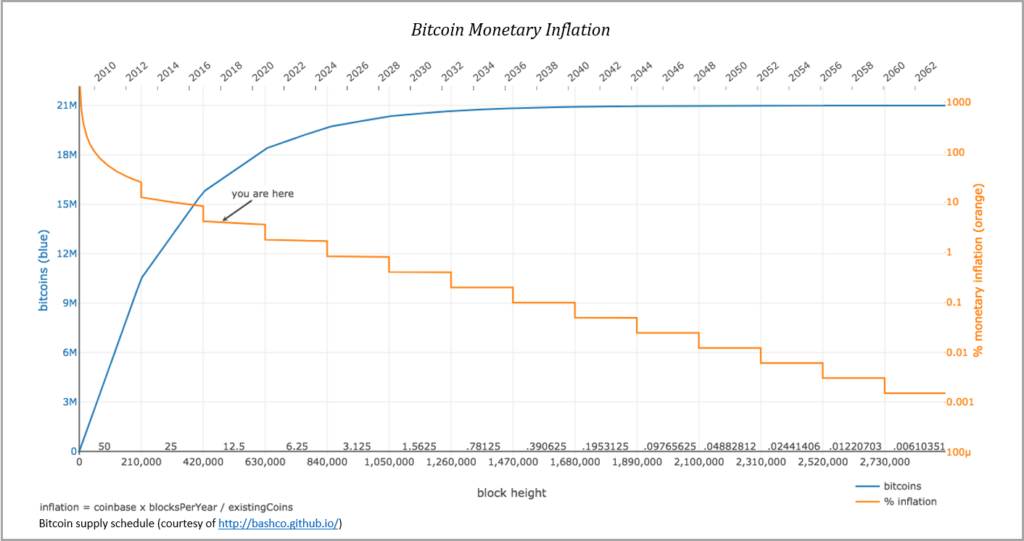

Approximately every four years, the newly issued bitcoin paid to miners gets cut in half (the bitcoin “halvening”). Today, with each block, 12.5 new bitcoin are issued. In approximately eight months, when the next halvening event occurs (see here), that amount will be reduced to 6.25 new bitcoin per block. Approximately four years after that, 3.125 new bitcoin per block will be issued. This process will continue until we reach the smallest unit of bitcoin (1/100,000,000th) and thereafter no new bitcoin will be issued. This is the issuance function that governs bitcoin’s fixed supply (21 million), and as a derivative function, it also shifts compensation to secure the network from (mostly) new bitcoin today to ultimately a system relying completely on transaction fees.

But how does this relate to Visa and transaction capacity? If it were not for the scarcity of capacity in each bitcoin block, there would not be a mechanism to create a transaction fee market. Scarcity in block space creates competition between market participants to clear transactions which causes them to bid up the value of real estate and to use it efficiently. Without a fee market, the only mechanism to pay miners to secure the network would be to alter bitcoin’s fixed monetary policy and increase supply. But recall that scarcity in bitcoin’s fixed supply (21 million) is the basis of its store of value property, which is where the rubber meets the road. By creating scarcity in network capacity, we also ensure the integrity of bitcoin’s fixed supply, which makes the whole value cycle function. Working within this reality, scarcity is a far more important property than either the speed or ultimate capacity of transaction throughput.

Fixed Network Capacity → Limited Transaction Capacity → Fee Market → Fixed Supply of Bitcoin

And because the real problem bitcoin is intending to solve is that of money and global QE (not payments), those that store wealth in bitcoin would much rather secure the money supply than sacrifice its long-term integrity and credibility for transaction throughput. In short, the future of bitcoin is far more secure in a world where all market participants can depend on it having a reliably fixed and scarce supply, while accepting lower transaction throughput or speed as trade-offs. What good is high transaction throughput and faster speeds if the fundamental value of the underlying currency is at risk? The existing financial system has already made the opposite trade-off for us. High transaction throughput and fast transactions by way of centralization but with the cost of an architecture susceptible to systemic monetary debasement. Bitcoin represents the alternative, and we are not about to make the same mistake twice.

Bitcoin ≠ Visa

Ultimately, bitcoin is not competing with Visa for supremacy in global payments. Instead, bitcoin is competing with the dollar, euro, yen and gold as money, and any comparison to Visa, its transaction volume or transaction speed is fundamentally flawed. Bitcoin fulfills the role of currency issuer and final settlement. As a result, the proper comparison would be between bitcoin and the Fed as currency issuer and as a clearing mechanism. No one makes the mistake of confusing the functions of Visa for that of the New York Fed, but for some reason, the comparison is often made between Visa and bitcoin.

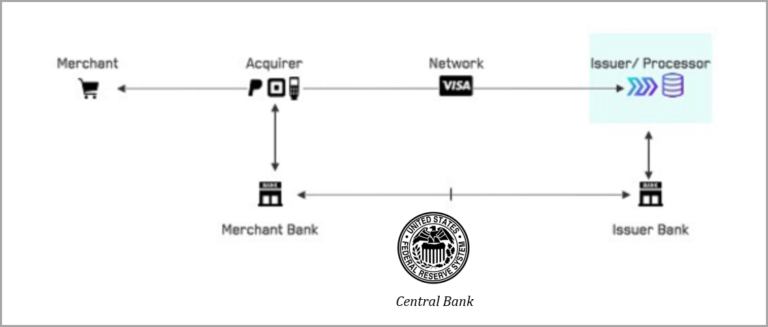

While it would require time and investment, Visa’s payment network could sit on top of the bitcoin network to fulfill payments much the same way it sits on top of the existing banking system. Rather than clearing the currency through a central bank, final settlement of transactions would clear through the bitcoin network. In the existing architecture, the payments layer (Visa) and the settlement layer (banking network/central banks) are separate and distinct. The principal problem bitcoin intends to solve has little to do with the former, but instead, with the mechanism by which currency is issued and cleared (think the Fed and QE). Visa helps move dollars but Visa is not the dollar. It is a technology company that provides a service; it has 17,000 employees. Bitcoin has none.

Whether credit or debit, Visa is an inherently trust-based credit system. While consumers generally associate swiping a Visa card (or the equivalent) at a point of sale terminal as payment, it really is not. Instead, balances are checked, transactions are authorized and settlement occurs later. Dollars are not actually cleared through a central bank or settled at the point of sale every time a transaction is processed. Individual transactions are also never really cleared. Instead, transactions are batched together, netted and settled at a later point in time; only then are accounts credited with proper balances. So when someone attempts to equate a Visa transaction with final settlement, that is just not the way the world works. But that is the comparison that is implicitly being made when someone attempts to compare Visa with bitcoin.

Bitcoin vs. the Federal Reserve

When compared against its real competition (the Fed, ECB, BOJ, etc.), bitcoin begins to look like a Ferrari. Final global settlement approximately every 10 minutes, 24 hours per day, 7 days a week, 365 days a year on a permissionless basis. Compare this to the existing permissioned financial system, which is subject to multiple layers of bank and central bank intermediaries and only open during “business” hours. This is the great misnomer that exists within bitcoin. Those that believe bitcoin to be too slow or lacking in network capacity are comparing bitcoin to the wrong application. We could set up a network of banks on top of the bitcoin network and the payments system could function as it does today.

The push back on this point is the risk of centralization. If bitcoin were to just sit in centralized banks, it would increase the possibility that the bitcoin network could be co-opted and undermined by a network of banks and central banks, whether to force changes to network consensus rules or to censor end users. Ultimately, this was gold’s failure as a monetary medium. It was susceptible to centralization, which then spawned fiat currencies, which have turned out to be easily manipulable. While this is unlikely (and hopefully not) how bitcoin scales, money and payments technology are distinct problems. The fundamental reason being that there are two sides to every value transfer; one side almost always involving money and the other as the fulfillment of goods and services. Payments layers help provide a bridge.

Because of the nature of trade, the two sides of a value transfer generally, and naturally, occur by different processes and at different points in time. Think about the settlement of currency on one side and the transfer of title to a home or car on the other. Or, payment for a good on Amazon and the fulfillment of that good two days later. Two different processes, occurring at two different times. And, it is important to recognize that bitcoin has no knowledge of the outside world, whether identities or the second leg of a value transfer; all bitcoin knows how to do is issue and validate currency (whether a bitcoin is a bitcoin). This is really the function and limitation of any base currency system. Payments layers provide a bridge between currency settlement (the Fed or bitcoin) and the fulfillment of goods and services. Gold solved mass payments via bank centralization, the dollar, the Fed and large payments processors such as Visa. Bitcoin likely solves payments through a technologically superior mechanism, but we have time to solve what is a separate and distinct problem from that of money.

Scaling Bitcoin is 1 to n

If we solve the problem of money through digital scarcity first (zero to one), the technology advancements to scale transactions and ultimately solve payments are 1 to n. It is not credible to think that human ingenuity can solve the former but then fail on the incremental derivatives. It is not just a matter of hope and faith; instead, it is one of reason and logic, considering both the advancements in scaling solutions that are already being pursued and the challenges relative to the problem bitcoin has already solved. Permissionless innovation and the economic incentives inherent in bitcoin will coordinate and accelerate solutions to any number of future challenges. Market participants have an incentive to increase the value of the network and to innovate to scale the network, but the solutions will have to work within the network’s consensus or garner sufficient consensus to change the rules.

Because of the nature of bitcoin’s economic incentives, it is far more likely that scaling solutions work within existing consensus rules. One such example of an advancement to scale bitcoin within the network’s consensus is the lightning network. The lightning network builds on top of bitcoin as a trust-minimized layer to scale transaction capacity, which still remains fundamentally distinct from payments fulfillment. However, if successful, lightning will be used to create bitcoin payment channels that enable far greater transaction throughput at far lower cost, the scale and speed of which would rival Visa. While it may not be the ultimate solution, it is an example of the innovation that bitcoin is fostering. Lightning is also only one of many solutions that are actively being developed, and competition will drive us toward the best scaling solutions, of which there may be a combination of many.

The approach to scaling bitcoin is a slow and conservative process. Bitcoin is too important to follow the Silicon Valley mantra of move fast and break things. Instead, it’s move slowly and don’t break anything. If a global financial system is to be built on a decentralized monetary system, the foundation must be protected at all cost. Ensure the security of the base monetary layer (bitcoin) first and then allow network participants to innovate on top of it in a permissionless manner. Remember that bitcoin is only ten years old; we are in the very inception of bitcoin’s monetization event, and infrastructure is still being built to allow for the proliferation of this new technology.

It’s a little ridiculous to contemplate the problem bitcoin has already solved and then immediately pivot to a “but why not mass payments today” line of thinking. Especially when considering that bitcoin, in its clearing function, is already faster and more reliable than comparable mechanisms for final settlement of dollars, euros, yen or gold. Then, when understanding that the fundamental use case for bitcoin today is as a long-term savings mechanism (not to fulfill payments), it becomes more clear that not only is the problem misdiagnosed but also that the desired solutions can wait. We will need the ability to fulfill payments in the future, but we have time before we get there. In due time, we’re going to have our cake and eat it too.