Bitcoin is Common Sense

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

Bitcoin is Common Sense

By Parker Lewis on Unchained Capital

Posted May 1, 2020

AUDIO VERSION BY Bitcoin Audible

“Perhaps the sentiments contained in the following pages, are not yet sufficiently fashionable to procure them general favor; a long habit of not thinking a thing wrong, gives it a superficial appearance of being right, and raises at first a formidable outcry in defense of custom. But the tumult soon subsides. Time makes more converts than reason.” – Thomas Paine, Common Sense (February 24, 1776)

These were the opening remarks of Thomas Paine’s call for American independence in early 1776. At the time, a declaration of independence was far from a certainty, but in Paine’s view, there was no question. It wasn’t a debate; there was only one path forward. Still, he understood that public opinion had not yet caught up and naturally remained anchored to the status quo, with a preference for reconciliation rather than independence. Old habits die hard. The status quo has a tendency of being defended, regardless of merit, merely by its anchoring in time to the way things have always been. However, truths have a way of becoming self-evident in time, more often due to common sense rather than any amount of reason or logic. One day, the truth is more likely to smack you in the face, becoming painfully obvious through some firsthand experience which opens up a perspective that otherwise would not have existed. While Paine was undoubtedly attempting to persuade an undecided populous with reason and logic, it was at the same time an appeal to not overthink that which stands in opposition to what is already self-evident.

In Paine’s view, independence was not a modern-day IQ test, nor was its relevance confined to the American colonies; instead, it was a common sense test and its interest was universal to “the cause of all mankind,” as Paine put it. In many ways, the same is true of bitcoin. It is not an IQ test; instead, bitcoin is common sense and its implications are near universal. Few people have ever stopped to question or understand the function of money. It facilitates practically every transaction anyone has ever made, yet no one really knows the why of that equation, nor the properties that allow money to effectively coordinate economic activity. Its function is taken for granted, and as a result, it is a subject not widely taught or explored. Yet despite a limited baseline of knowledge, there is often a visceral reaction to the very idea of bitcoin as money. The default position is predictably no. Bitcoin is an anathema to all notions of existing custom. On the surface, it is entirely inconsistent with what folks know money to be. For most, money is just money because it always has been. In general, for any individual, the construction of money is anchored in time and it is very naturally not questioned.

But enter bitcoin, and everyone suddenly becomes an expert in what is and isn’t money, and to the fly-by-night expert, it certainly is not bitcoin. Bitcoin is natively digital, it is not tied to a government or central bank, it is volatile and perceived to be “slow,” it is not used en masse to facilitate commerce, and it is not inflationary. This is one of those rare instances when a thing does not walk like a duck or quack like a duck but it’s actually a duck, and what you thought was a duck all along was mistakenly something entirely different. When it comes to modern money, the long habit of not thinking a thing wrong, gives it a superficial appearance of being right. In all perceived-to-be successful applications today, money is issued by a central bank; it is relatively stable and capable of near infinite transaction throughput; it facilitates day-to-day commerce; and by the grace of god, its supply can be rapidly inflated to meet the needs of an ever-changing economy. Bitcoin has none of these traits (some not presently, others not ever), and as a result, it is most often dismissed as not meeting the standards of modern-day money. This is where overthinking a problem can cripple the highest of IQs. Pattern recognition fails because the game fundamentally changed, but the players do not yet realize it. It is akin to getting lost in the weeds or failing to see the forest through the trees. Bitcoin is finitely scarce, it is highly divisible and it is capable of being sent over a communication channel (and on a permissionless basis). There will only ever be 21 million bitcoin. Rocket scientists and the most revered investors of our time could look at this equation relative to other applications in the market and be confounded, not seeing its value. While at the same time, if posed with a very simple question, would you rather be paid either in a currency with a fixed supply that cannot be manipulated or in a currency that is subject to persistent, systemic and significant debasement, an overwhelming majority of individuals would choose the former all day, every day.

On bitcoin: “It’s probably rat poison squared” – Warren Buffett

“Bitcoin – there’s even less you can do with it […] I’d rather have bananas, I can eat bananas” – Mark Cuban

Money Doesn’t Grow On Trees

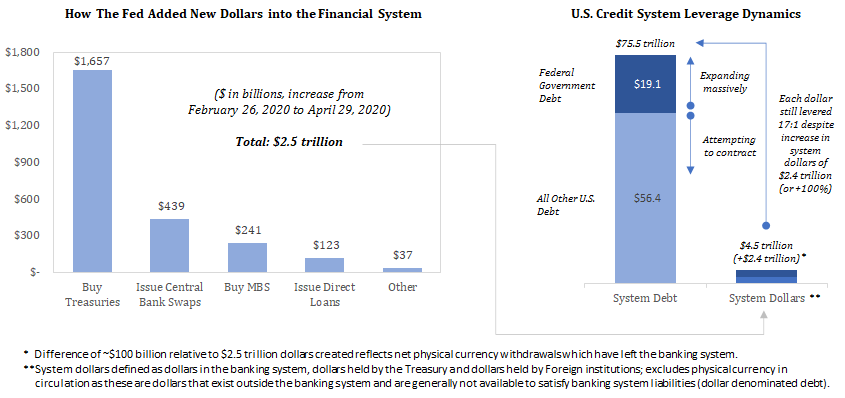

As kids, we all learn that money doesn’t grow on trees but on a societal level, or as a country, any remnant of common sense seems to have left the building. Just in the last two months, central banks in the United States, Europe and Japan (the Fed, ECB and BOJ) have collectively inflated the supply of their respective currencies by $3.3 trillion in aggregate – an increase of over 20% in just eight weeks. The Fed alone has accounted for the majority, minting $2.5 trillion dollars and increasing the base money supply by over 60%. And it’s far from over; trillions more will be created. It is not a possibility; it is a certainty. Common sense is that deep feeling of uncertainty many are experiencing that says, “this doesn’t make any sense” or “this doesn’t end well.” Few carry that thought process out to its logical conclusion, often because it is uncomfortable to think about, but it is reverberating throughout the country and the world. While not everyone is connecting the equation to 21 million bitcoin, a growing number of people are. _Time makes more converts than reason. _Individuals don’t have to understand how or why there will only ever be 21 million bitcoin; all that has to be recognized in practical experience is that dollars are going to be worth significantly less in the future, and then the idea of having a currency with a fixed supply begins to make sense. Understanding how it is possible that bitcoin has a fixed supply comes after making that initial connection, but even still, no one needs to understand the how to understand that it is valuable. It is the light bulb turning on.

For each individual, there is a choice to either exist in a world in which someone gets to produce new units of money for free (but just not them) or a world where no one gets to do that (including them). From an individual perspective, there is not a marginal difference in those two worlds; it is night and day, and anyone conscious of the decision very intuitively opts for the latter, recognizing that the former is neither sustainable, nor to his or her advantage. Imagine there were 100 individuals in an economy, each with different skills. All have determined to use a common form of money to facilitate trade in exchange for goods and services produced by others. With the one exception that a single individual has a superpower to print money, requiring no investment of time and at practically no cost. Given human time is an inherently scarce resource and that it is a required input in the production of any good or service demanded in trade, such a scenario would mean that one person would get to purchase the output of all the others for free. Why would anyone agree to such an arrangement? That the individual is an enterprise, and more specifically, a central bank expected to act in the public interest does not change the fundamental operation. If it does not make sense on a micro level, it does not magically transform into a different fundamental fact merely because there are greater degrees of separation. If no individual would bestow that power in another, neither would a conscious decision be made to bestow it in a central bank.

Everything beyond this fundamental reality strays into abstract theory, relying on leaps of faith, hypotheticals and big words that no one understands, all while divorced from individual decision points. It is not that one individual is more trusted than another or one central bank relative to another; it is simply that, on an individual level, no individual is advantaged by someone else having the ability to print money, regardless of identity or interests. That this is true leaves only one alternative, that each individual would be advantaged by ensuring that no other individual or entity has this power. The Fed may have the ability to create dollars at zero cost, but money still doesn’t grow on trees. It is more likely that a particular form of money is not actually money than it is that money miraculously started growing on trees. And at an individual level, everyone is incentivized to ensure that is not the case. While there is a long habit of not thinking this particular thing wrong, the errant defense of custom can only stray so far. Time converts everyone back into reality. At present, it is the Fed’s “shock and awe” campaign contrasted by the simplicity in bitcoin’s fixed supply of 21 million. There is no amount of reason that can replace an observed divergence in two distinct paths.

Defending Existing Custom

“There’s money and there’s credit. The only thing that matters is spending and you can spend money and you can spend credit. And when credit goes down, you better put money into the system so you can have the same level of spending. That’s what they did through the financial system (referencing QE in response to the past crisis) and that thing worked.”– Ray Dalio, CNBC September 19, 2017

Basic Bitcoin Common Sense

There is No Such Thing as a Free Lunch

As more people become aware of the Fed’s activities, it only begins to raise more questions. $2,500,000,000,000 is a big number, but what is actually happening? Who gets the money? What will the effects be and when? What are the consequences? Why is this even possible? How does it make any sense? All very valid questions, but none of these questions change the fact that many more dollars exist and that each dollar will be worth materially less in the future. That is intuitive. However, at an even more fundamental level, recognize that the operation of printing money (or creating digital dollars) does nothing to generate economic activity. To really simplify it, imagine a printing press just running on a loop. Or, imagine keying in an amount of dollars on a computer (which is technically all that the Fed does when it creates “money”). That very operation can definitionally do nothing to produce anything of value in the real world. Instead, that action can only induce an individual to take some other action.

Recognize that any tangible good or service produced is produced by some individual. Human time is the input, capital production is the output. Whether it is software applications, manufacturing equipment, a service or an end consumer good, all along the value chain, an individual contributed time to produce some good or service. That time and value is ultimately what money tracks and prices. Entering a large number into the computer does not produce software, hardware, cars or homes. People produce those things and money coordinates the preferences of all individuals within an economy, compensating value to varying degrees for time spent.

When the Fed creates $2.5 trillion in a matter of weeks, it is consolidating the power to price and value human time. Seems cryptic but it is not a suggestion that the individuals at the Fed are consciously or deliberately operating maliciously. It is just the root level consequence of the Fed’s actions, even if well intentioned. Again, the Fed’s operation (arbitrarily adding zeros to various bank account balances) cannot actually generate economic activity; all it can do is determine how to allocate new dollars. By doing so, it is advantaging some individual, enterprise or segment of the economy over another. In allocating new dollars that it creates, it is replacing a market function, one priced by billions of people, with a centralized function, greatly influencing the balance of power as to who controls the monetary capital that coordinates economic activity. Think about the distribution of money as the balance of control influencing and ultimately determining what gets built, by whom and at what price. At the moment of creation, there exists more money but there exists no more human time or goods and services as a consequence of that action. Similarly, over time, the Fed’s actions do not create more jobs, there are just more dollars to distribute across the labor force, but with a different distribution of those holding the currency. The Fed can print money (technically, create digital dollars), but it can’t print time nor can it do anything but artificially manipulate the allocation of resources within an economy.

No Free Lunches, Just More Dollars

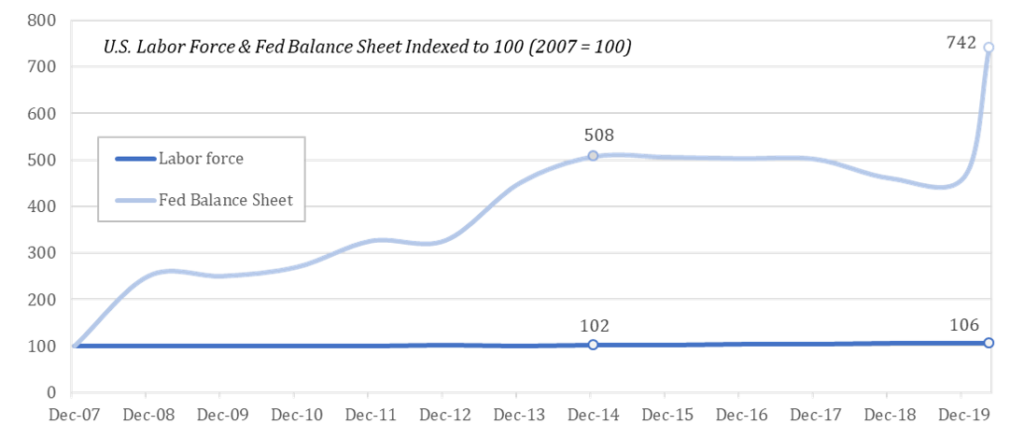

Since 2007, the Fed balance sheet has increased seven-fold, but the labor force has only increased 6%. There are roughly the same number of people contributing output (human time) but far more dollars to compensate for that time. Do not be confused by impossible-to-quantify theory concerning the idea of a job saved versus a job lost; this is the U.S. labor force, defined by the Bureau of Labor Statistics as all persons 16 years of age and older, both employed and unemployed. The inevitable result is that the value of each dollar declines, but it does not create more workers, and all prices do not adjust ratably to the increase in the money supply, including the price of labor.

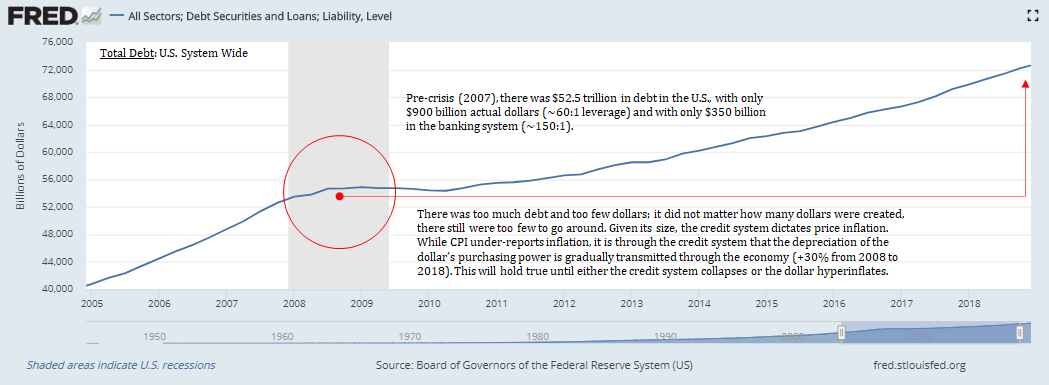

In a theoretical world, if the Fed were to distribute the money in equal proportion to each individual that held the currency previously, it would not shift the balance of power. In practical application, the distribution of ownership shifts dramatically, heavily favoring the holders of financial assets (which is what the Fed buys in the process of creating new dollars) as well as those with cheap access to credit (the government, large corporations, high net-worth individuals, etc.). In aggregate, the purchasing power of every dollar declines, just not immediately, while a small subset benefits at the cost of the whole (see the Cantillon Effect). Despite the consequences, the Fed takes these actions in an attempt to support a credit system that would otherwise collapse without the supply of more dollars. In the Fed’s economy, the credit system is the price setting mechanism as the amount of dollar-denominated debt far outstrips the supply of dollars, which is also why the purchasing power of each dollar does not immediately respond to the increase in the money supply.

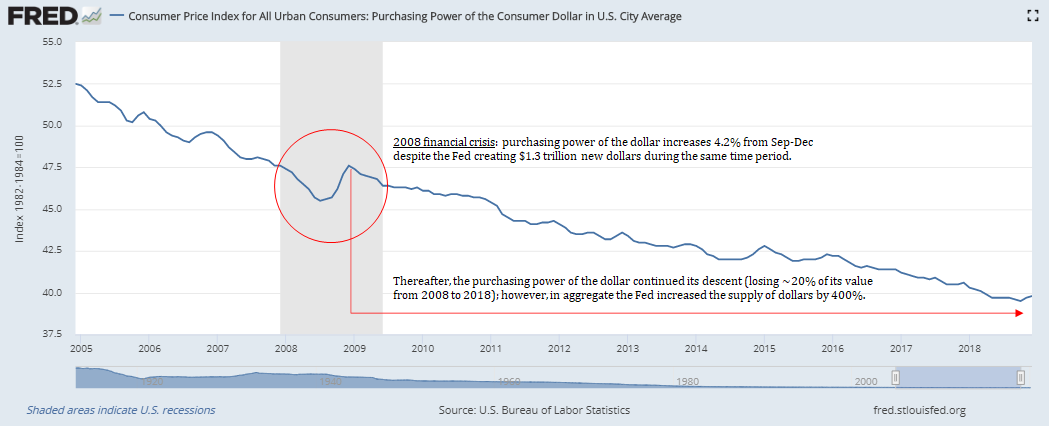

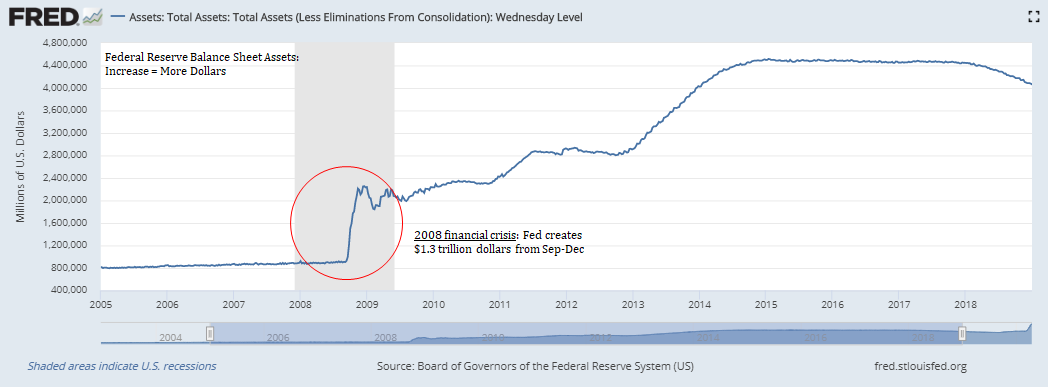

Instead, the effects of increasing the money supply are transmitted, over time, through an expansion of the credit system. The credit system attempting to contract is the market and the individuals within an economy adjusting and re-pricing value; the Fed attempting to reverse that natural course by flooding the market with dollars is, by definition, overriding the market’s price setting function, fundamentally altering the structure of the economy. The market solution to the problem is to reduce debt (expression of preference) and the Fed’s solution is to increase the supply of dollars such that existing debt levels can be sustained. The goal is to stabilize the credit system such that it can then expand, and it is a redux to the 2008 financial crisis, which provides a historical roadmap. In the immediate aftermath of the prior crisis, the Fed created $1.3 trillion new dollars in a matter of months. Despite this, the dollar initially strengthened as deflationary pressures in the credit system overwhelmed the increase in the money supply, but then, as the credit system began to expand, the dollar’s purchasing power resumed its gradual decline. At present, the cause and effect of the Fed’s monetary stimulus is principally transmitted through the credit system. It was the case in the years following the 2008 crisis, and it will hold true this time so long as the credit system remains intact.

How the effects manifest in the real economy is very complicated, but it does not take any sophistication to recognize the general direction of the end game or its foundational flaws. More dollars result in each dollar becoming worth less, and the value of any good naturally trends toward its cost to produce. The marginal cost for the Fed to produce a dollar is zero. With all the bailouts from both the Fed and Congress, whether to individuals or companies, someone is paying for everything. It is axiomatic that printing money (or creating digital dollars) does nothing to generate economic activity; it only shifts the balance of powers as to who allocates the money and prices risk. It strips power from the people and centralizes it to the government. It also fundamentally impairs the economy’s ability to function as it distorts prices everywhere. But most importantly, it puts the stability of the underlying currency at risk, which is the cost that everyone collectively pays. The Fed may be able to create dollars for free and the Treasury may be able to borrow at near-zero interest rates as a direct result, but there is still no such thing as a free lunch. Someone still has to do the work, and all printing money does is shift who has the dollars to coordinate and price that work.

The Moon is a Harsh Mistress, by Robert Heinlein

“Gospodin,” he said presently, “you used an odd word earlier–odd to me, I mean…”

“Oh, tanstaafl. Means there ain’t no such thing as a free lunch. And isn’t,” I added, pointing to a FREE LUNCH sign across room, “or these drinks would cost half as much. Was reminding her that anything free costs twice as much in long run or turns out worthless.”

“An interesting philosophy.”

“Not philosophy, fact. One way or other, what you get, you pay for.”

Bitcoin is Common Sense

Among its perceived flaws as a currency, bitcoin is viewed by many to be too complicated to ever achieve widespread adoption. In reality, the dollar is complicated; bitcoin is not. It becomes very simple when abstracted to the least common denominator: 21 million bitcoin; and who controls the money supply: no one. Not the Fed or anyone else. At the end of the day, that is all that matters. Bitcoin is in fact complicated at a technical level. It involves higher level mathematics and cryptography and it relies on a “mining” process that makes very little sense on the surface. There are blocks, nodes, keys, elliptic curves, digital signatures, difficulty adjustments, hashes, nonces, merkle trees, addresses and more.

But with all this, bitcoin is very simple. If the supply of bitcoin remains fixed at 21 million, more people will demand it and its purchasing power will increase; there is nothing about the complexity underneath the hood that will prevent adoption. Most participants in the dollar economy, even the most sophisticated, have no practical understanding of the dollar system at a technical level. Not only is the dollar system far more complex than bitcoin, it is far less transparent. Similar degrees of complexity and many of the same primitives that exist in bitcoin underly an iPhone, yet individuals manage to successfully use the application without understanding how it actually works at a technical level. The same is true of bitcoin; the innovation in bitcoin is that it achieved finite digital scarcity, while being easy to divide and transfer. 21 million bitcoin ever, period. That compared to $2.5 trillion new dollars created in two months, by one central bank, is the only common sense application anyone really needs to know.

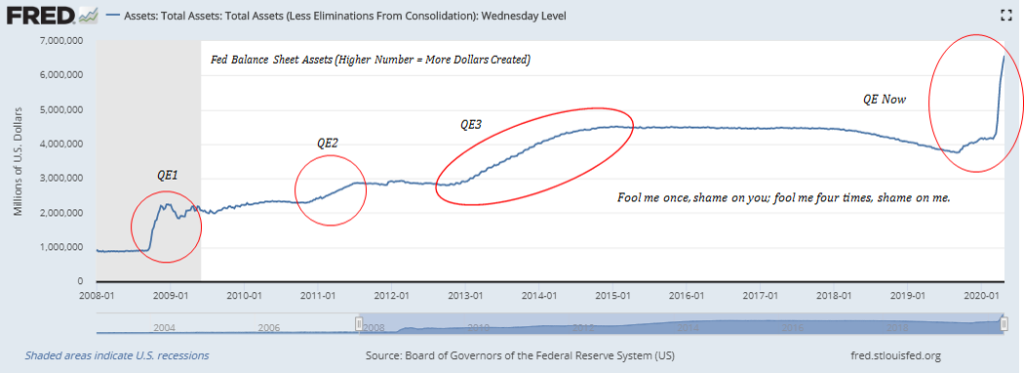

Exhibit A – Dollar Supply

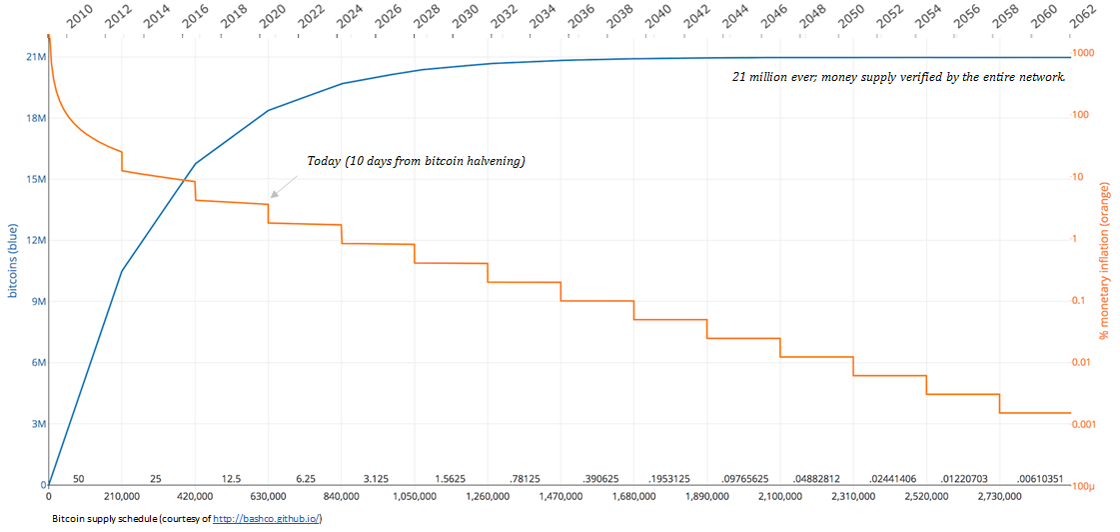

Plus Exhibit B – Bitcoin Supply

Equals Exhibit C – Purchasing Power of Bitcoin Relative to Dollars

There is a lot happening in the background, but these three charts are what drives everything. People all over the world are connecting these dots. The Fed is creating trillions of dollars at the same time the rate of issuance in bitcoin is about to be cut in half (see the bitcoin halvening). While most may not be aware of these two divergent paths, a growing number are (knowledge distributes with time) and even a small number of people figuring it out ultimately puts a significant imbalance between the demand for bitcoin and its supply. When this happens, the value of bitcoin goes up. It is that simple and that is what draws everyone else in: price. Price is what communicates information. All those otherwise not paying attention react to price signals. The underlying demand is ultimately dictated by fundamentals (even if speculation exists), but the majority do not need to understand those fundamentals to recognize that the market is sending a signal.

Once that signal is communicated, then it becomes clear that bitcoin is easy. Download an app, link a bank account, buy bitcoin. Get a piece of hardware, hardware generates address, send money to address. No one can take it from you and no one can print more. In that moment, bitcoin becomes far more intuitive. Seems complicated from the periphery, but it is that easy, and anyone with common sense and something to lose will figure it out; the benefit is so great and money is such a basic necessity that the bar on a relative basis only gets lower and lower in time. Self-preservation is the only motivation necessary; it ultimately breaks down any barriers that otherwise exist.

The stable foundation that underpins everything is a fixed supply which cannot be forged, capable of being secured without any counterparty risk and resistant to censorship and seizure. With that bedrock, it does not require a lot of imagination to see how bitcoin evolves from a volatile novelty into a stable economic juggernaut. A hard-capped monetary supply versus endless debasement; a currency that becomes exponentially more expensive to produce compared to a currency whose cost to produce is anchored forever at zero by its very nature. At the end of the day, a currency whose supply (and derivatively its price system) cannot be manipulated. Fundamental demand for bitcoin begins and ends at this singular cross-section. One by one, people wake up and recognize that a bill of goods has been sold, always by some far away expert and never reconciling with day-to-day economic reality.

With bitcoin as a backdrop, it becomes self-evident that there is no advantage either in ceding the power to print money or in allowing a central bank to allocate resources within an economy, and in the stead of the people themselves that make up that economy. As each domino falls, bitcoin adoption grows. As a function of that adoption, bitcoin will transition from volatile, clunky and novel to stable, seamless and ubiquitous. But the entire transition will be dictated by value, and value is derived from the foundation that there will only ever be 21 million bitcoin. It is impossible to predict exactly how bitcoin will evolve because most of the minds that will contribute to that future are not yet even thinking about bitcoin. As bitcoin captures more mindshare, its capabilities will expand exponentially beyond the span of resources that currently exist. But those resources will come at the direct expense of the legacy system. It is ultimately a competition between two monetary systems and the paths could not be more divergent.

Bananas grow on trees. Money does not, and bitcoin is the force that reawakens everyone to the reality that was always the case. Similarly, there is no such thing as a free lunch. Everything is being paid for by someone. When governments and central banks can no longer create money out of thin air, it will become crystal clear that backdoor monetary inflation was always just a ruse to allocate resources for which no one was actually willing to be taxed. In common sense, there is no question. There may be debate but bitcoin is the inevitable path forward. Time makes more converts than reason.

“You can fool all the people some of the time, and some of the people all the time, but you cannot fool all the people all the time.” – Abraham Lincoln

“These proceedings may at first seem strange and difficult, but like all other steps which we have already passed over, will in a little time become familiar and agreeable: and until an independance is declared, the Continent will feel itself like a man who continues putting off some unpleasant business from day to day, yet knows it must be done, hates to set about it, wishes it over, and is continually haunted with the thoughts of its necessity.” – Thomas Paine, Common Sense

Views presented are expressly my own and not those of Unchained Capital or my colleagues. Thanks to Will Cole and Phil Geiger for reviewing and for providing valuable feedback.