Banks, QE, and Money-Printing

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

Banks, QE, and Money-Printing

By Lyn Alden

Posted November 22, 2020

Lately, it has become fashionable to debate what is, or is not, “money-printing” by central banks.

This debate is natural, due to the extreme policy nature of 2020, with massive fiscal expenditures, huge increases in central bank balance sheets, and changes in central bank inflation targets. It’s important to know what is inflationary, and what isn’t, and to what extent.

Because people have very different understandings of how central bank policy and fiscal policy work, there have been analyst calls this year ranging from hyperinflation to deep deflation, and everything in between.

The outcome has of course been somewhere in the middle as measured by CPI or PCE, with inflation that rebounded from March lows in response to policy, but neither much of an overshoot or undershoot, and still generally below long-term central bank inflation targets.

Many inflation categories for the most essential and non-outsourced goods and services, however, have risen faster than the overall basket this year, and in recent years.

The crux of this article is that quantitative easing on its own, and quantitative easing combined with massive fiscal deficits, are two very different situations to consider when it comes to analyzing the possibilities between inflation and deflation, and what constitutes “money printing”.

The Deflationary Backdrop

Before diving into the mechanisms of money-printing, it helps to set the stage. Context is key.

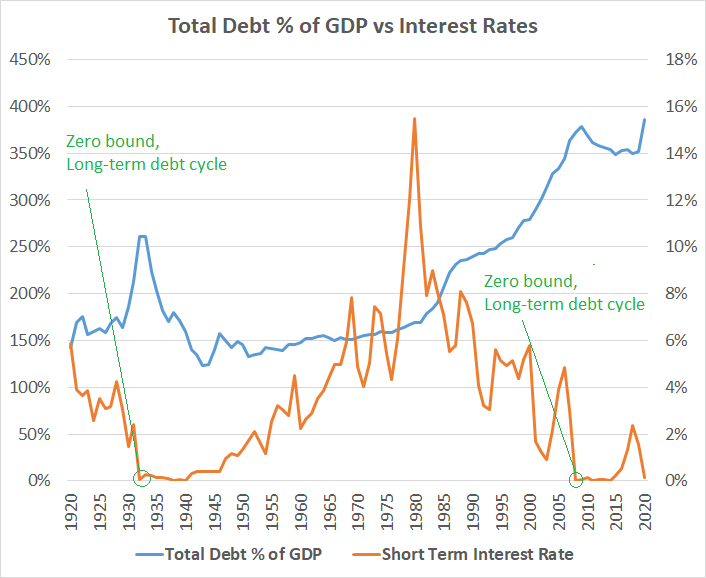

Historically speaking, we’re coming down from the apex of, and currently within the lengthy resolution process of, a long-term debt cycle, which refers to a multi-decade peak in public and private debts relative to the size of the economy and money supply. This occurs in the aftermath of when interest rates hit zero.

We’ve been in this resolution process for the past 12 years, and the previous time before that was the two-decade period of the 1930’s and 1940’s where we hit the previous apex of a long-term debt cycle.

Here is total debt as a % of GDP in the United States over the past century in blue on the left axis (all debts, public and private), along with short-term interest rates in orange on the right axis:

Data Sources: U.S. Treasury Department, U.S. Federal Reserve

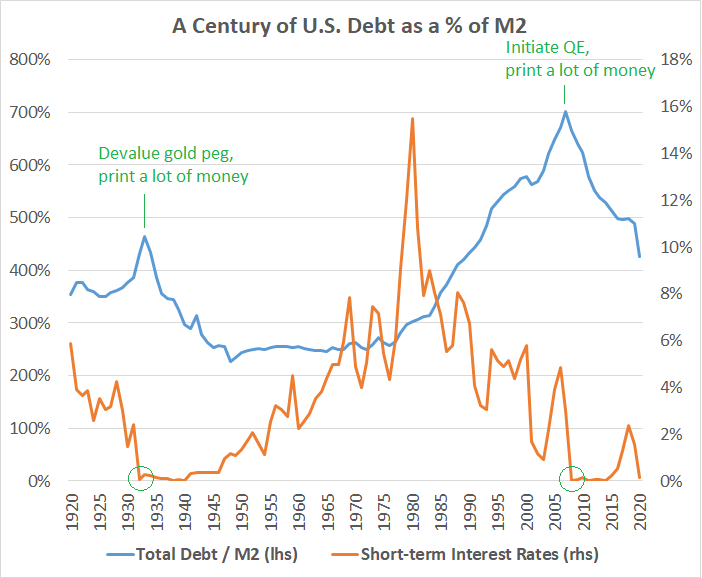

And here is total debt as a % of the broad money supply, which shows the structural peaks of each cycle even more clearly (since policymakers have more influence over broad money supply than GDP, due to shifting monetary velocity):

Data Sources: U.S. Treasury Department, U.S. Federal Reserve

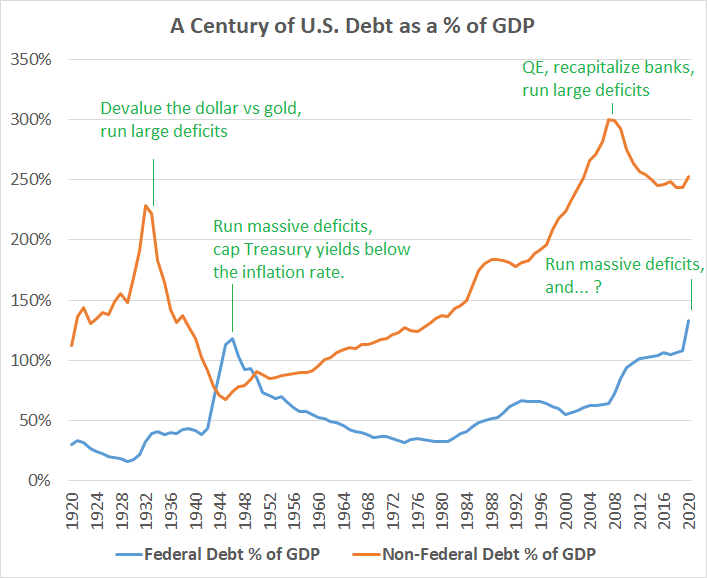

If we break out federal debt from non-federal debt (households, businesses, states, financial leverage, etc), we see two distinct peaks in each long-term cycle. Non-federal debt (orange line) peaks first in a commercial banking crisis (early 1930’s and late 2000’s), and then federal debt (blue line) peaks many years later in a sovereign debt crisis (mid-1940’s and ???-2020’s):

Data Sources: U.S. Treasury Department, U.S. Federal Reserve

There are a lot of deflationary forces on consumer prices in the economy:

- High private debt levels are deflationary, since it makes consumers and businesses financially restrained and risk-adverse.

- Slowing population growth and aging demographics are deflationary, since resource demand slows.

- Technology is deflationary, since it makes some things cheaper and better.

- Wealth concentration into fewer hands is deflationary, since money coalesces rather than circulates.

- Commodity oversupply is deflationary, since it cheapens the building blocks we use for everything else.

- Outsourcing is deflationary, since it lowers labor costs of goods and puts downward pressure on domestic wages.

In a low-debt system, structural deflation for some of the positive reasons, such as technological improvement, would be a good thing. It means your money’s purchasing power grows over time, as higher productivity from technological enhancements lowers the cost of goods or improves their quality, so you get more value for your dollar.

However, in an extraordinarily high-debt system (which requires a lot of central policy intervention in the first place to be able to get up that high), deflation breaks things and results in widespread defaults, because the cost of servicing debts goes up relative to cash flows.

So, fiscal and monetary policymakers deliberately push back on deflationary forces with inflationary policy, especially when it gets to those extremes. And there are a few definitions or types of inflation that we can identify.

Monetary inflation refers to the growth of the broad money supply, which can be calculated in a few ways but is pretty straightforward.

Asset price inflation refers to bubble-like increases in the prices of financial assets, like stocks, bonds, gold, private equity, fine art, and so forth. This is a bit more subjective because valuations on assets can vary, but there are various ratios to keep track of it in a broad sense.

Consumer price inflation refers to a broad rise in the prices of everyday goods and services, and people debate about how it should be measured. The government uses CPI and PCE calculations on a basket of goods, but those use various substitutions. There are alternative calculations that don’t use substitutes, which generally lead to higher figures.

Each household has their own unique basket of consumer goods and services that they buy. For research purposes, I calculated that my personal household consumer price inflation rate averaged about 3% per year over the past two years, taking into account our total purchases of non-investment goods and services.

QE Alone = Bank Recapitalization

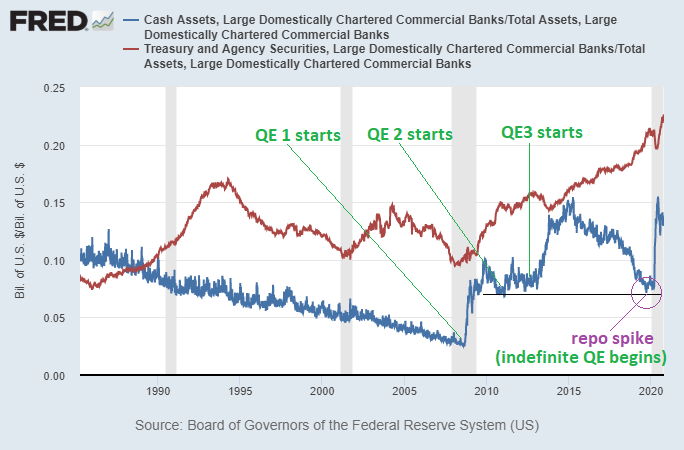

Going into the 2008 crisis, U.S. banks were extremely leveraged, with very low bank reserves.

Large bank cash levels equaled just 3% of their assets (blue line below; cash as a percentage of total assets), and large bank holdings of Treasuries as a percentage of assets were pretty low historically as well (red line; treasury securities as a percentage of total assets):

Chart Source: St. Louis Fed

So, leading into the financial crisis, only about 13% of their assets consisted of cash (3%) and Treasury securities (10%). The rest of their assets were invested in loans and riskier securities. This was also at a time when household debt to GDP reached a record high, as consumers were caught up in the housing bubble.

That over-leveraged bank situation hit a climax into the 2008/2009 crisis, coinciding with record high debt-to-GDP among households, and was the apex of the long-term private (non-federal) debt cycle. When banks are that leveraged with very little cash reserves, even a 3% loss in assets results in insolvency. And that’s what happened; the banking system as a whole hit a peak total loan charge-off rate of over 3%, and it resulted in a widespread banking crisis.

However, banks were bailed out via QE and the Troubled Asset Relief Program. It was a top-down, anti-deflationary bank industry bailout, but not a bottom-up, pro-inflationary real economy bailout. TARP boosted bank solvency, and QE boosted bank liquidity.

As the crisis played out and some banks failed and others were bailed out, regulators wanted to increase bank reserve requirements and capital requirements, requiring banks to hold a greater percent of their assets in cash reserves and other safe assets. The problem with that, however, is that banks can’t just magically boost up their reserves; they would have to sell other assets to get cash, but if every bank in the system sells assets to get cash, who do they sell to, and where would so much cash come from to buy what they sell?

In other words, while it’s possible for an individual bank to boost its reserves by selling assets to raise capital, it’s mechanically impossible for the entire banking industry to collectively raise its reserves industry-wide.

So, in the role of lender/buyer of last resort, the Federal Reserve created new cash reserves out of thin air, gave them to the banks, and took some of their Treasuries and mortgage-backed securities in return, aka quantitative easing or QE. Along with TARP, this recapitalized banks, bringing them from 3% cash as a percentage of assets at the start of 2008, to 8% by the end of 2008. The Fed did further rounds of QE through 2014 that brought banks collectively up to 15% cash levels, which brought them up to frothy levels of excess reserves.

This, however, didn’t result in more money chasing fewer goods and services, and therefore wasn’t particularly inflationary for every prices. The money remained mostly internal to the banking system, at higher reserve levels. Broad money supply didn’t increase rapidly.

Many analysts that were worried about inflation missed the fact that the transmission mechanism from QE to the real economy was small, so this was mostly just a bank-recapitalization process. Banks and their executives got a nice assist from the Fed and Treasury, but the broad public did not. Banks didn’t lend much of the money out (nor was there a ton of creditworthy demand for them to do so), and fiscal spending didn’t go around the banking channel very much either.

A similar version of this played out in the 1930’s, which was the previous time that interest rates hit the zero bound at the apex of a long-term private debt cycle. The banking system collapsed back then too, so policymakers devalued the dollar vs the gold peg, expanded the monetary base, and recapitalized banks during a banking holiday. This was enough to offset the deep deflation that was happening in the early 1930’s, and turn it back into a reflationary trend in the mid-1930’s, but not enough to cause rapid broad consumer price inflation. It was anti-deflationary, in other words, but not outright inflationary.

The Inflation Fake-Out

All told, the Fed expanded their balance sheet by about $3.5 trillion from mid-2008 to the end of 2014. They created new bank reserves to buy Treasuries and mortgage-backed securities.

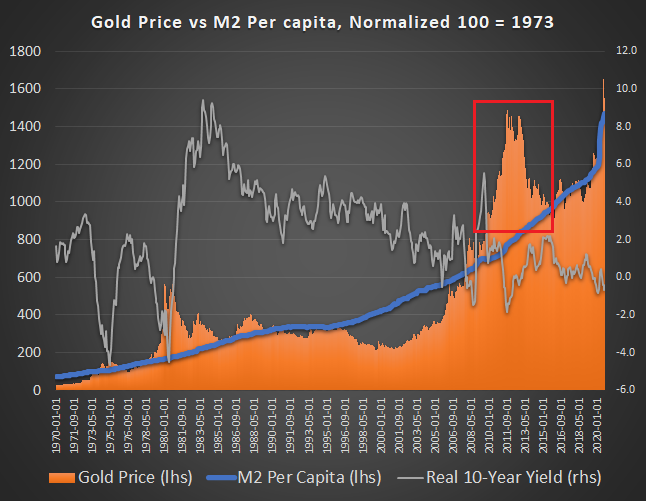

Many folks thought this would be hyperinflationary, Weimar Republic style. So, they bid up the price of gold rather high. I’m glad they felt that way, because I sold my gold to them in 2011, during a period of very high sentiment. It’s the only time I sold physical bullion. I wanted to load up on historically cheap stocks instead.

Here was the gold price relative to my model (i.e. orange area way above blue line):

Data Source: St. Louis Fed

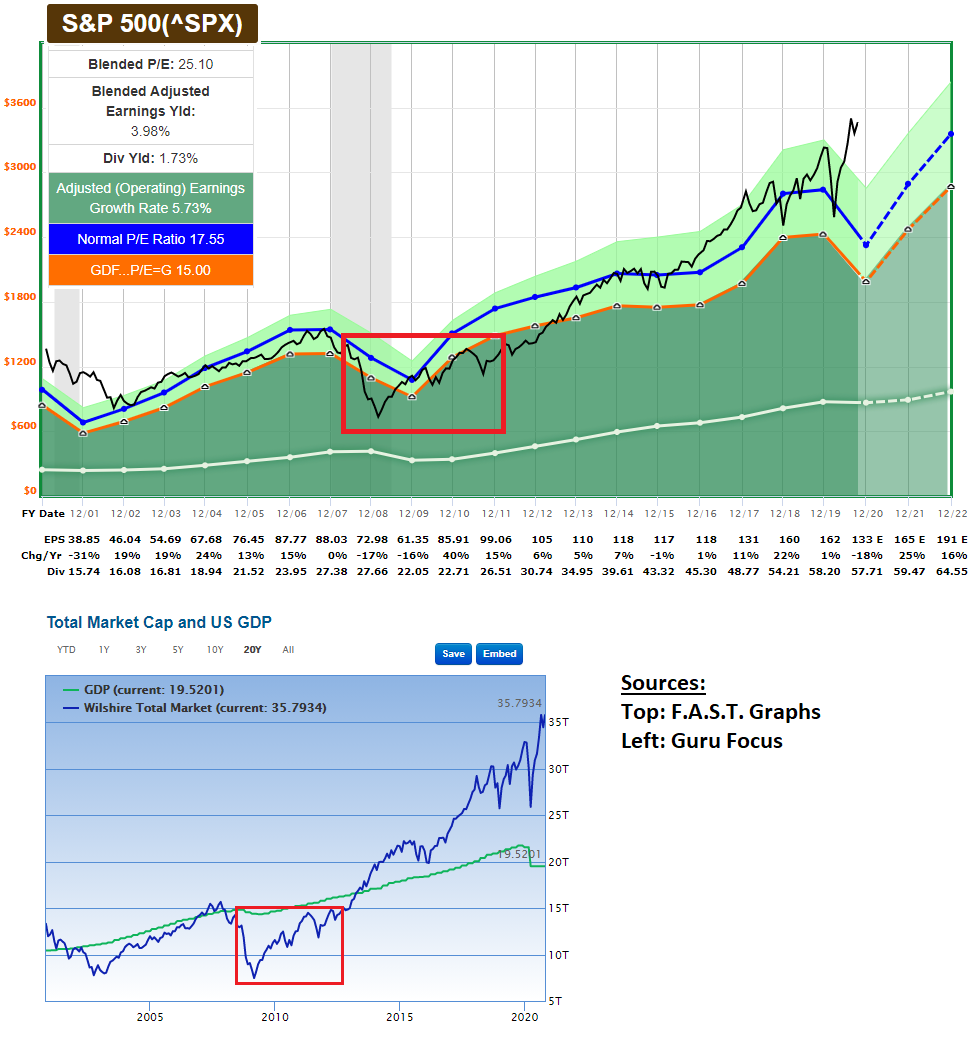

And here were stock valuations relative to fundamentals:

Of course, this QE ended up not being outright inflationary for consumer prices, for reasons described before. It was anti-deflationary, rather than outright inflationary. Along with low rates, it was somewhat inflationary for asset prices, but not most consumer prices. That’s how it worked in the 1930’s, too.

We can put some broad numbers on it. From 2007 to 2009, there was a $11 trillion decline in U.S. household net worth, as it fell from $71 trillion to $60 trillion, due to a decline in stock and house prices. It then took about five years for U.S. household net worth to recover to previous highs. This was $11 trillion in deflationary wealth destruction (plus technology improvements, and commodity oversupply, tightened credit for home equity loans, and other deflationary forces), up against the response of $3.5 trillion in Fed bank reserve creation or QE. Of course it wouldn’t be hyperinflationary.

Morally hazardous? Sure. Hyperinflationary? No.

Moreover, as previously-described, most of the $3.5 trillion never entered the broad money supply because there was no major fiscal transfer mechanism, so it mostly just stayed in bank reserves. It offset a deflationary shock and bank collapse by recapitalizing the banking system with higher levels of solvency and liquidity (and thus was anti-deflationary), but it was not outright inflationary.

Bank Reserve Example

Banks, in practice, are limited in how much leverage and risk they can take by their regulatory capital requirements. In this model, there are some very low-risk assets (like bank reserves, Treasury securities, and gold) that don’t count against the bank’s risk level, and there are higher-risk assets (like personal loans, or corporate bonds) that do count against a bank’s overall risk level. Banks need to maintain an appropriate balance of assets to avoid being considered too risk-heavy.

In some regulation regimes, banks can also be constrained by reserve requirements, meaning that banks are required to have a certain percentage of deposits stored as cash reserves.

Suppose that there is a regulatory rule which says that all banks must have an amount of cash equal to 5% of their customer bank deposits (which are liabilities for banks; owed to their customers) held in reserve at the Federal Reserve. So, if a bank has $100 billion in customer bank deposits held with them (which are liabilities for the bank), and $110 billion in assets (and so they have $10 billion more assets than liabilities), they can put up to $105 billion of their assets into various forms (making loans, buying securities, etc), but must hold at least $5 billion in cash reserves at their account with the Fed.

Here is a reserve-constrained bank example. A bank has $100 billion in deposits (liabilities), and $110 billion in assets. Of their assets, $5 billion is in cash reserves, $20 billion is in Treasuries, $10 billion is in mortgage-backed securities, and $75 billion is in other assets (personal loans, mortgage loans, corporate loans, and/or whatever else). This bank can’t lend anymore, until either it collects more deposits which would also boost reserves, or sells some existing assets. It is therefore reserve-constrained. It might want to lend, and has good client demand to lend money to, but it simply can’t leverage itself anymore. If the Fed were to create $5 billion in brand new reserves (aka QE) and buy $5 billion of their Treasuries or mortgage-backed securities, it would alleviate their reserve-constrained status, and the bank could use that $5 billion to lend more, or buy more securities. This would be economically stimulative if the bank wants to lend money, because now the bank can go ahead and lend that money, and thus create deposits somewhere in the system and increase the broad money supply.

Here is a non-reserve-constrained example. A bank has $100 billion in deposits (liabilities) and $110 billion in total assets. Of their assets, $15 billion is in cash reserves, $20 billion is in Treasuries, $10 billion is in mortgage-backed securities, and $65 billion is in other assets. This bank has $10 billion in excess reserves above the $5 billion requirement; extra money it can lend. Maybe it doesn’t want to lend right now; it doesn’t see any good risk-adjusted loans to make. Or maybe there isn’t a lot of demand from its clients to borrow money. So, it’s just holding that extra $10 billion as excess reserves, in addition to their $5 billion required reserves. If the Fed were to do QE and buy $5 billion of their Treasuries, and bring the bank up to $20 billion in reserves, it won’t affect how much they lend, because they weren’t reserve-constrained to begin with. This would not be stimulative and would not increase the broad money supply, since it doesn’t coerce the bank to make any more loans.

That is why QE alone isn’t inflationary. Increasing bank reserves does not necessarily increase the broad money supply. A rapidly increasing broad money supply along with constraints on the supply of goods and services, is what can lead to inflation.

There are two ways to increase broad money supply. Either banks need to lend, or the federal government can go around them and run big fiscal deficits. At the apex of a long-term debt cycle, the latter tends to happen.

QE + Fiscal Stimulus = Money Printing

Now in 2020, in the next recession twelve years after the 2008 banking crisis, we’re back at it and bigger than before, but with a twist.

This time, going into the crisis, the banking system was already well-capitalized. The percent of bank assets that consist of cash and Treasuries was already historically high. So, unlike 2008, banks weren’t over-leveraged. However, the broader economy was over-leveraged, and the pandemic hit the broader economy.

Millions of people became unemployed, and countless businesses faced insolvency risk as their cash flows collapsed. For the Fed to simply buy Treasuries and MBS from banks wouldn’t do almost anything for this, because it’s not a bank recapitalization issue, and there would be no transmission mechanism to the public. Banks were already well-capitalized, and so the banks weren’t reserve-constrained.

Instead, this time, fiscal authorities (Congress and the President) spent trillions of dollars into the real non-bank economy, sending folks stimulus checks, boosting unemployment benefits by an extra $600/week (which is $2,400/month for several months for folks who received it), financing banks to give small businesses PPP loans that mostly turn into grants, and partially bailing out some of the hardest-hit corporate industries with fresh capital injections. It was a much larger stimulus than anything from 2008/2009.

The way that the government’s accounting works in the current legal structure, is that they have to issue a lot of Treasury securities to fund that expenditure. However, the foreign sector was not really buying Treasuries, and in fact were selling some Treasuries early this year. So, who would be available to buy $3 trillion in extra Treasury securities this year?

Enter the Fed again. When the Treasury market became illiquid in March from foreigners and hedge funds selling Treasuries against a backdrop of insufficient buyers, the Fed stepped in, and created $1 trillion in brand new bank reserves out of thin air to buy $1 trillion in Treasuries over a 3-week period. This was the most rapid asset-purchase program the Fed has ever done. And then they tapered that rate but kept buying Treasuries for months to soak up the massive 2020 Treasury issuance that funded all the stimulus, and are still buying tens of billions of dollars of Treasuries monthly with newly-created bank reserves to this day.

So, the Fed once again increased its balance sheet (this time by nearly $3 trillion in just three months) to buy a large chunk of Treasuries, plus some other assets like mortgage-backed securities and a handful of corporate bonds. About $2 trillion, or 2/3rds of this 2020 balance sheet expansion so far, consisted of buying Treasuries. But what made this one different, was that it didn’t just stay in the banking system to recapitalize banks. It flowed through banks to the U.S. Treasury Department, which injected that money directly into the economy as authorized by Congress’ CARES Act.

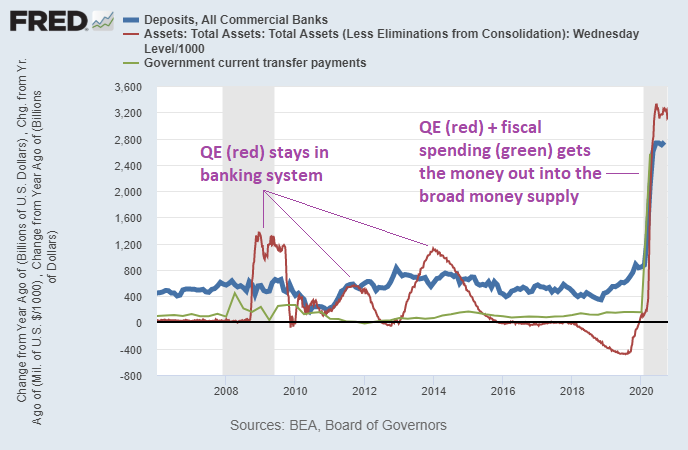

This following chart shows the year-over-year change (in billions of dollars) of total U.S. commercial bank deposits in blue, government transfer payments in green, and the Fed’s balance sheet in red:

Chart Source: St. Louis Fed

That chart is critical to see why 2020 and 2008 were quite different, and why the policy response acted so much quicker and more powerfully on financial markets and personal income this time. Personal income and net worth on a nationwide scale went up, rather than down, in 2020 so far.

In 2008-2014, there was a lot of QE (red line going up), but those dollars didn’t get out into public bank deposits (which is what mostly makes up the broad money supply). This was because there was little or no fiscal transmission mechanism; the government wasn’t sending huge checks to people. So, the green line (year-over-year change in government transfer payments) and blue line (year-over-year change in bank deposits) remained low. The QE process in 2008 mostly just recapitalized banks.

However, 2020 was a very different story. The government sent out tons of money directly into the economy, and financed it by issuing Treasury bonds that the Federal Reserve created new bank reserves to buy. For legal reasons, the Fed buys those securities on the secondary market, but that doesn’t make much of a difference in practice; it’s where they end up and remain that matters. The banks that buy them from the Treasury and sell them to the Fed just act as pass-through entities in this case.

So, the blue, green, and red lines all went vertical in 2020, unlike the 2008-2014 period. The government sent money to people and businesses (green line), that money showed up in their bank deposits (blue line) and thus in the broad money supply, and the Fed created new bank reserves to buy a lot of the Treasury securities issued to fund that program (red line).

Or, put simply, the broad money supply went up a lot in 2020, but didn’t budge nearly as much in 2008/2009 (in either absolute or percent terms), because QE alone to recapitalize banks, and QE-financed fiscal stimulus into the real economy, are two very different situations:

Chart Source: St. Louis Fed

Many people who saw the inflationary non-event from 2008-2014, are suggesting that QE is inherently deflationary, and that it won’t cause inflation this time either.

I’m glad many people feel that way, because I’m happy to buy their gold from them on dips. I bought plenty of precious metals back in 2018 and have cooled my purchases since then due to the notable uptick in price, but am still happy to dollar-cost average into them at these prices, or buy on dips. I also like cheap natural resources more broadly, as well as high-quality equities, real estate, Bitcoin, and other scarce assets for a diverse mix, with a long-term view.

In my view, the “QE is deflationary; it only increases bank reserves!” position is from not taking into account the fiscal element; the transmission mechanism that gets QE into the hands of the public rather than stuck in the banking system. QE alone is not inflationary and mostly stays in bank reserves, but QE combined with massive fiscal deficits, is inflationary, and gets the funds out into the broad money supply, out into commercial bank deposits of the public.

Basically, massive fiscal spending combined with the central bank buying lots of sovereign bonds to fund it, is a modern monetary theory “MMT” program in practice, for the first time since the 1940’s when the equivalent of “wartime MMT” was used.

Now, bear in mind that this is still up against large deflationary forces: technology, demographics, debt, and shifting consumer behavior around the pandemic. So, even a one-time pro-inflationary $3 trillion injection into the real economy is merely enough to cause a quick rebound in inflation and a sharp recovery in asset prices, as we saw in 2020 from the March lows. Combined with certain supply limitations, it also helped cause non-discretionary prices to rise: grocery price inflation in particular was rather significant this year.

However, a one-time $3 trillion injection is not enough to cause a persistent trend change in inflation. Those deflationary forces outweigh it. There is not yet a situation of too much money chasing too few goods and services, except in niche areas. The stimulus delayed an insolvency crisis for several months and got consumers through the worst 3-4 month period of the economic shutdowns.

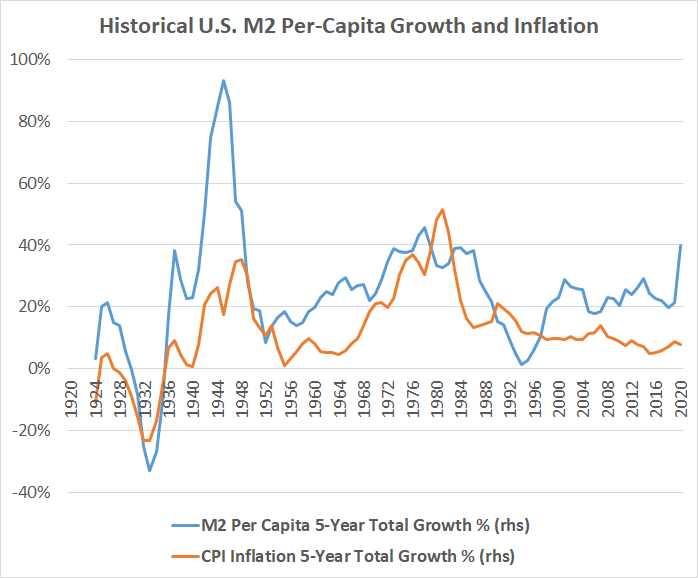

If we look over the past century, we can see that the two inflationary decades (the 1940’s and 1970’s) occurred when broad money rose rapidly. This chart shows the 5-year rolling cumulative percent increase in the consumer price index and in broad money supply per capita:

Data Source: U.S. Federal Reserve

Therefore, the big question for investors in multiple asset classes, is whether the fiscal authorities will keep repeating that on a notable scale, or whether they will cool off. Without the massive fiscal+QE “MMT” combo, the economy remains in the grip of structural disinflation, and a renewed cyclical disinflationary trend. However, with another round of massive fiscal+QE “MMT” combo, the outcome would likely be more of what we saw in spring/summer of 2020: rebounding inflation and asset prices, and likely eventually pushing too far.

Ultimately, with so much debt in the system and the weight of private debt, policymakers are likely to be forced to do more rounds of fiscal stimulus (either from civil unrest or political donors), but the timing for that is something that investors need to work around when it comes to assessing the inflationary or disinflationary outlook for the next couple quarters ahead.

Right now, with money velocity so low and the pandemic still raging, and plenty of commodity oversupply particularly in regards to oil, it may seem like there is a limitless sink for broad money creation without leading to sustained consumer price inflation. However, that can change a couple years down the line, as the world fully emerges from pandemic effects, after years of not putting much capital into resource development.

It’s also worth noting that “fiscal stimulus” in this sense refers to both spending and taxation. In other words, federal deficits. A fiscal stimulus could include giving everyone a $1,200 check, or could include giving everyone a $1,200 payroll tax cut, for example. The differences between those two mechanisms matter around the margins (particularly for the unemployed, who wouldn’t benefit from a payroll tax cut), but for large chunks of the 150 million working population, a stimulus check and a payroll tax cut are functionally similar throughout the course of a year, and result in more cash in the hands of most people. These policies increase the amount of broad money, not just bank reserves.

When it comes to fiscal stimulus, regardless of whether it takes the form of taxation or spending changes, its stimulatory impact and inflation outcomes are mostly a question of magnitude, as well as who it primarily targets (unemployed, working class, middle class, wealthy, or rich). It’s inflationary, against the deflationary backdrop, and so whether the outcome shifts to inflation or remains disinflationary becomes a question of scale and persistence, and whether it increases productive capacity or not.

Rules Are Meant to Be… Broken? Bent?

In my view, focusing on some of the mechanics of the Fed’s QE combined with fiscal injections is like focusing on the trees and missing the forest.

This is because at the end of a long-term debt cycle, policymakers do whatever they need to in order to avoid a deflationary collapse and get towards some degree of reflation and devalued debt levels.

The Federal Reserve Act doesn’t allow the Fed to buy corporate bonds. And yet, the Fed bought corporate bonds this year.

How did the Fed do that? They worked with the Treasury and Congress, set up a Special Purpose Vehicle, and bought corporate bonds through that vehicle, with any defaults on those bonds funded by the Treasury so the Fed doesn’t face the risk of nominal losses.

People saying this violates the Federal Reserve Act are, unfortunately, falling on deaf ears.

Policymakers went around the spirit of the Federal Reserve Act, but perhaps not the letter of the law due to the structure involved. It’s perhaps not surprising that the heads of the world’s two biggest central banks, the Fed and the ECB, are both lawyers rather than economists.

I personally think that the Fed buying corporate bonds was not a good part of the overall policy response, and sets a bad precedent and moral hazard. But, it happened nonetheless, and it is during the apexes of long-term debt cycles that these sorts of “exceptions” tend to happen.

The Fed has legal limitations on its own, which is good. However, when the Fed works closely with the Treasury Department and Congress to combine fiscal and monetary policy, all bets are off. They worked together closely in 1940’s decade to fund World War II in the second half of the previous long-term debt cycle apex, and they did so again here in the new 2020’s decade.

Love it or hate it, that Treasury+Fed combo is extremely powerful and bypasses just about any limitation that the Fed alone has. The Fed can lend but can’t spend. The Treasury can spend, but if it spends a ton and issues more sovereign debt than there is demand for, it needs the Fed to buy some of its sovereign debt issuance (using primary dealer banks as pass-through entities). The Fed can’t buy certain securities, particularly those that could lead to nominal losses, but with a special purpose vehicle and a financial backstop by the Treasury, they can. Together, they can create new money, and inject it to whoever they want.

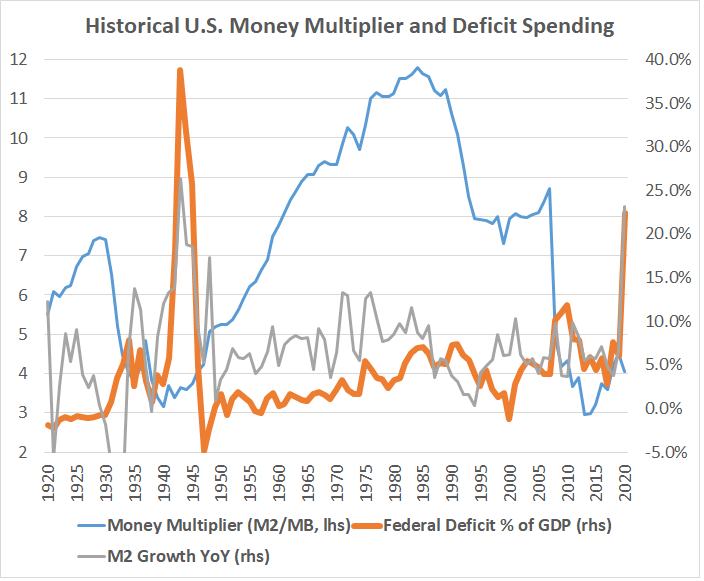

Many people think that the broad money supply is only able to increase when banks lend money and create deposits. However, ironically, the biggest increases in the broad money supply historically happen when things are terrible and so banks *aren’t* lending much, and thus when the money multiplier (broad money divided by base money) is low.

At those times, the federal government runs massive fiscal deficits, and goes around the bank lending channel to either tax less from the economy or inject more money into the economy (historically they choose the latter), and finances its massive deficits by having the Federal Reserve create new bank reserves to buy a large chunk of its Treasury debt issuance.

This chart highlights that, by showing the money multiplier on the left axis, with federal deficits as a percent of GDP, and year-over-year percent increase in the broad money supply, on the right axis:

Data Sources: U.S. Treasury Department, U.S. Federal Reserve

However, when it comes to investment timing, sometimes focusing on the mechanics is helpful. So, let’s dive into some of those mechanics.

Bank Reserve Accounting

Bank reserves, referring to the accounts that commercial banks have with the Federal Reserve, are strange beasts because of how unintuitive they are.

In fact, even the very definition of “money” is subject to debate. There are multiple ways to define “money” in the modern banking system.

The monetary base, and the broad money supply, are the two most important definitions, so let’s quantify them for context.

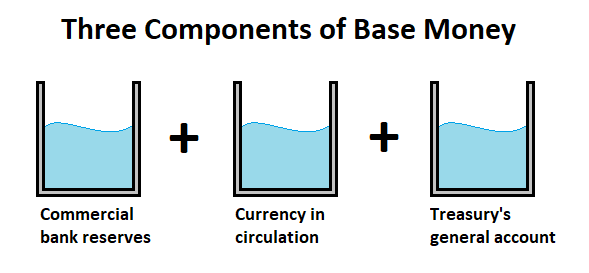

Base Money

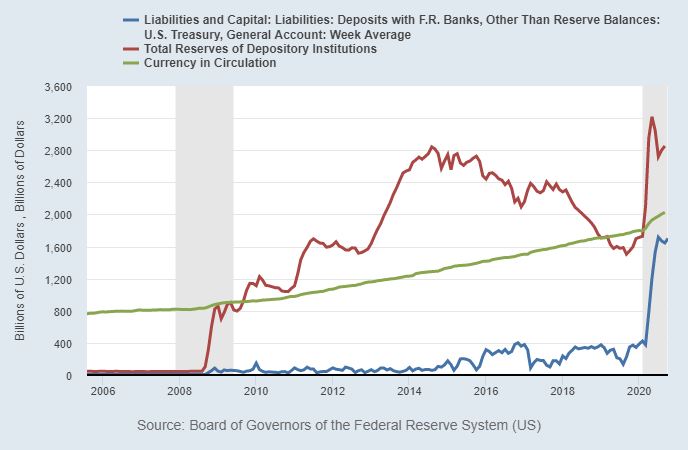

The monetary base is the foundation, and consists of physical currency in circulation (currently around $2 trillion) and cash reserve deposits that the commercial banking system has with the Fed (currently around $2.8 trillion).

Although not part of the original definition, because the Treasury’s general account “TGA” with the Fed has grown in size and importance in recent years (currently $1.7 trillion), we functionally should include that as well, since it’s another cash deposit with the Fed. Those three buckets combined are $6.5 trillion in “base money”.

All three of these buckets of base money (currency in circulation, bank reserves with the Fed, and the Treasury’s general account with the Fed) are the Fed’s biggest liabilities. On the other side of the Fed’s ledger, Treasuries and mortgage-backed securities represent most of the Fed’s assets.

If we look at these major Fed liabilities separately, with the TGA in blue, bank reserves in red, and currency in circulation in green, it looks pretty random:

Chart Source: St. Louis Fed

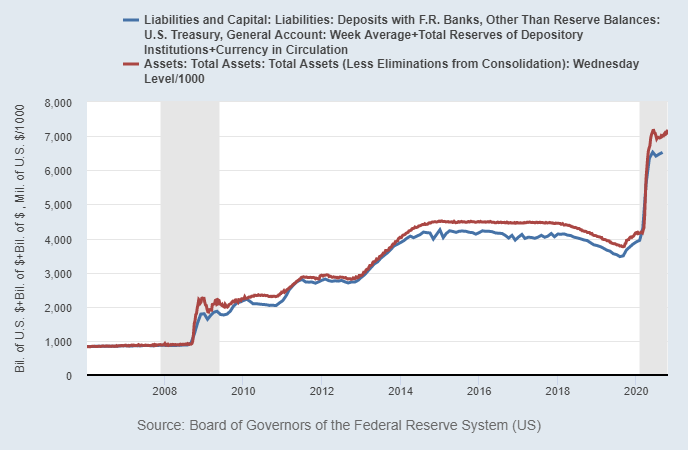

However, there’s a method to the madness, and the Fed controls the total sum.

This next chart shows the sum of those three lines, meaning currency in circulation, commercial bank reserves with the Fed, and the Treasury’s general account with the Fed (which are collectively the main liabilities of the Fed) in blue, and shows the Fed’s total assets in red (which mostly consists of Treasuries and mortgage-backed securities):

Chart Source: St. Louis Fed

Bank cash reserves at the Fed are fungible with each other. As folks like you and I use various payment systems to transact with each other, our banks use reserves to settle with each other behind the scenes.

Bank reserves are also fungible to some extent with currency in circulation. In fact, that’s one of the initial reasons for banks to have reserves in the first place: in case tons of people want to withdraw money at once. In theory, if we all wanted to go and take out some of our bank cash at once, it would come from bank reserves. However, in practice, the amount of minted physical currency is limited (mostly on purpose), so if there was a bank run, consumers would quickly find themselves limited in how much cash they would physically be allowed to withdraw, as the bank runs out of vault cash. But basically, physical currency and bank reserves are fungible.

Bank reserves are fungible with the Treasury general account as well. When the Treasury issues a lot of bonds and pulls capital into its account, it sucks it out of bank reserves. When it eventually spends down its account, those funds wind up back in bank reserves.

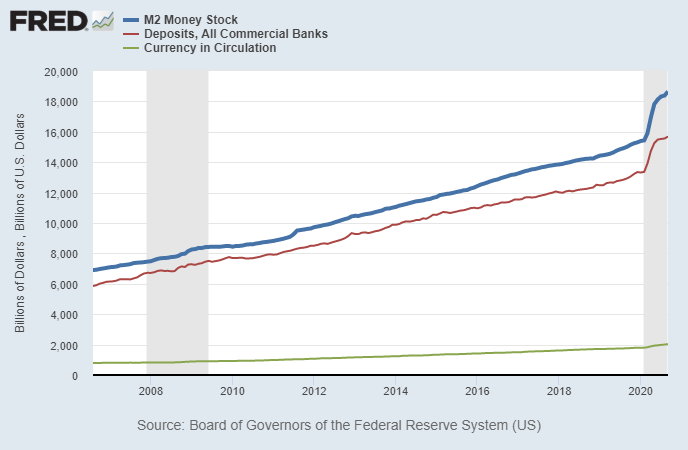

Broad money

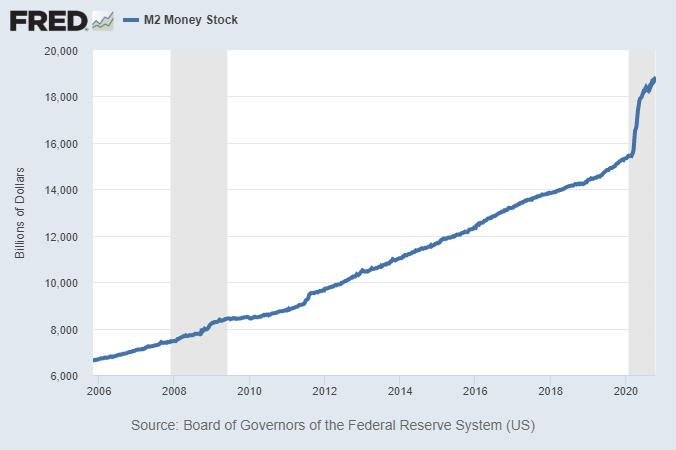

The broad money supply, on the other hand, is currently $18.8 trillion, which is far larger than the base money amount. This broad money calculation consists of currency in circulation, but then also includes the massive amounts of checking deposits, savings deposits, and various functional cash-equivalents that consumers and businesses hold at commercial banks. This is the broader set of money that we consumers actually use to transact with each other and store our capital and define as our “money”.

The blue line below shows the broad money supply. The red line shows commercial bank deposits, and the green line shows physical currency in circulation. The red line and green line added together roughly equal the blue line.

Chart Source: St. Louis Fed

When the Fed does QE alone, it increases bank reserves in the system, but doesn’t necessarily increase the broad money supply. The broad money supply only increases when either a) banks create more money by making loans or b) the federal government runs big fiscal deficits to inject money to people and businesses in the system. Many people miss that second one; they assume that money supply can only increase if banks lend, which isn’t correct.

Conservation of Reserves + Currency + TGA (Base Money)

For the most part, only the Fed can determine the sum of commercial bank reserves + currency in circulation + the Treasury’s general account, hereby referred to as “base money”.

Think of these three forms of base money as buckets of water. The total amount of water can move around between the three buckets if we pour one into another, but is conserved within the total three-bucket system. Only the Fed can increase or decrease the total amount of water in the total three-bucket system.

The purpose of modern banks is to “multiply” base money into broad money, and make a profit along the way. We can call this the “money multiplier”, defined as the broad money supply divided by the base money supply.

When a bank makes a loan to someone, it becomes another bank’s deposit, and the loaning bank sends the reserve amount to the depositing bank, and increases the total amount of commercial bank deposits and broad money in the system. So, when they “loan reserves”, banks collectively don’t actually reduce total bank reserves in the banking system; they just lever those reserves up with a higher money multiplier, and change the location/ownership of those reserves.

Any individual bank can leverage itself (up to a limiting point where it still meets capital and reserve requirements) by lending money or buying securities, and thus reducing its excess cash reserves at the Fed. However, when they make these loans or buy those assets, they create deposits somewhere else in the financial system, and those deposits become reserves of other banks. Similarly, a bank could sell assets and increases its cash reserves, but in doing so, some other bank deposits would be drained to buy those assets, which would reduce reserves somewhere else in the system.

Therefore, the banking system as a whole can’t decide to collectively increase or decrease the system-wide amount of bank reserves, even though any individual bank can alter its own level of reserves. They can collectively increase the money multiplier (the broad money supply divided by base money) by making more loans or buying more securities, but they can’t change the total system-wide bank reserves. They can just move them around, and leverage them up, or deleverage them.

Similarly, the U.S. Treasury can determine the size of its general account at the Fed. To increase it, they can issue Treasuries, bring in a lot of cash, and then hold the cash in that account at the Fed for a while before spending it. This sucks bank reserves out of the system, on a 1:1 basis with the general account increase. When they eventually reduce the general account by spending more than they take in, that money goes into peoples’ and companies’ bank accounts and thus winds up back in bank reserves.

The public can theoretically pull money out of excess bank reserves into physical currency, or deposit physical currency into banks which would wind up as more reserves, like water flowing back and forth between those two buckets of base money. In practice, however, physical currency is limited on purpose, so if the public collectively tries to pull bank reserves out into physical currency, they get told by the bank teller that they can’t, because there’s a nationwide shortage of physical currency.

The Fed, however, can create new base money, and thus add more total water to the three-bucket system analogy, by performing quantitative easing or “QE”. To do this, they create new bank reserves out of thin air, and then buy existing assets, like Treasuries or mortgage-backed securities with those new reserves. After this asset swap, the reserves become owned by a commercial bank (and thus become the Fed’s liabilities), and the securities become owned by the Fed (and thus become the Fed’s assets). In this process, the Fed increases their total assets (the securities they are buying) and increases their liabilities (the new reserves they are creating) by the same amount.

The Fed can also decrease base money, or destroy water in the three-bucket system analogy, by performing quantitative tightening “QT”. To do this, they sell or let some of their Treasuries or mortgage-backed securities mature and get their principle back. They then retire that cash. In this process, both the Fed’s assets and liabilities decrease.

In a vacuum, neither QE nor QT alone directly affects the broad money supply; it just affects the base money amount.

However, if the federal government is running very large fiscal deficits and the Fed is creating new bank reserves to buy the Treasury issuance to fund those deficits, it directly creates new broad money (and thus goes around the bank lending channel).

On the other hand, if the federal government were to run big fiscal surpluses on a sustained basis (i.e. tax more than they spend by a lot), at a time when banks aren’t lending much either, they can theoretically decrease the total amount of broad money. This would be very rare, if ever, to occur. Additionally, widespread bank collapses without any bailout or FDIC insurance can also theoretically reduce broad money, which happened in the early 1930’s.

Bank Reserve Accounting Examples

This section gets gritty. I’ll work through six examples of bank lending, QE, and fiscal deficits, to help show which types of actions by banks, the Fed, and the government, can influence the amount and location of bank reserves and broad money supply in the system.

| For each example, I have two people, Mary and Sara, the two banks they do business with, the Fed, and the U.S. Treasury. Each of these six entities has a column that represent each of their assets and liabilities “A | L”. |

Each example is a small closed-loop financial system. Each block in an entity’s asset or liability column represents $1,000 of value.

- “D” represents a $1,000 customer bank deposit.

- “R” represents a $1,000 cash reserve allocation that a bank has at the Fed.

- “T” represents a $1,000 U.S. Treasury note; U.S. federal government debt.

- Other assets, like a $1,000 used car “C” or a $1,000 car loan “L” are sometimes used as well.

A deposit block “D” is an asset for a consumer, and is simultaneously a liability for their commercial bank, since the bank holds it on behalf of the consumer and owes it to them on demand.

Similarly, a reserve block “R” is an asset for a commercial bank, and they keep it at the Fed. The Fed lists it as a liability, owed to the bank who deposited it with them.

Likewise, a Treasury note “T” is an asset for whoever holds it, whether a consumer, or a commercial bank, or the Fed, and is a liability of the U.S. Treasury.

A bank loan block “L” or mortgage block “M” is an asset for the bank that lent it, and is a liability for the consumer who borrowed it from their bank.

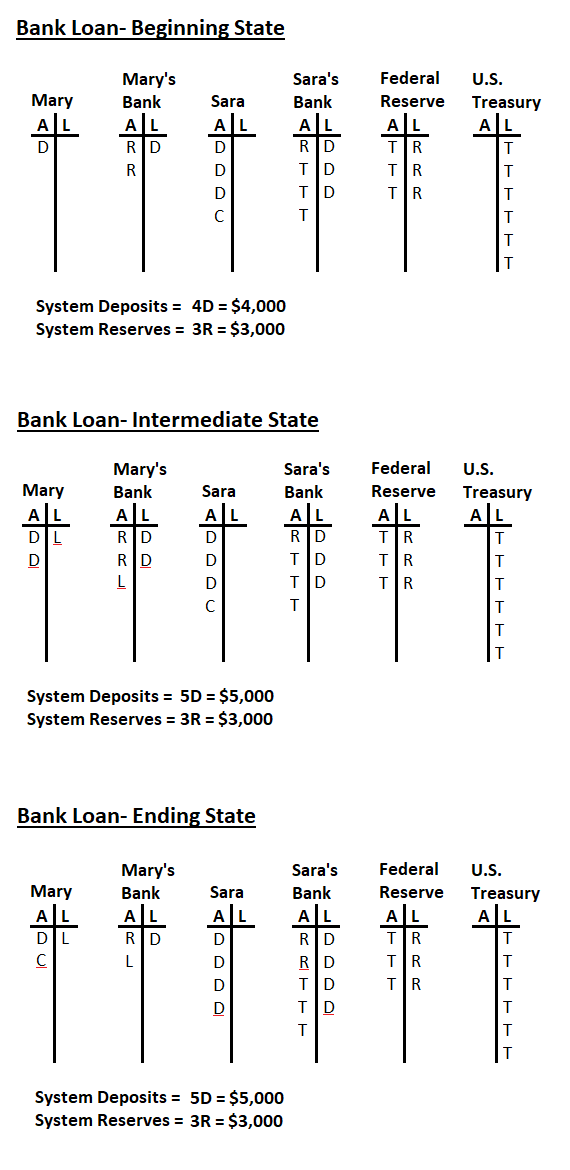

Example 1) A Bank Loans Money

This is the simplest example to show how banks create deposits and broad money without reducing the amount of reserves in the system. It involves Mary buying a used car from Sara.

Here is the visual, with a beginning, intermediate, and ending state, and a description afterward, so you can go back and forth between the visual and the description:

Beginning State

Mary begins with “D” in assets, meaning a $1,000 deposit in her bank, and no liabilities. Her bank (which is very unlevered) starts with her deposit “D” as a $1,000 liability, and then has two reserve block assets “R”, representing $2,000 held at the Fed.

Sara begins with “DDDC” in assets, meaning $3,000 in bank deposits at her bank “DDD”, and a $1,000 used car “C”, and no liabilities. Her bank starts with her deposit “DDD” as liabilities, and has its assets primarily invested in Treasuries “TTT” and one reserve block at the Fed “R”.

The Federal Reserve holds the three blocks of reserves from the two banks as its liabilities, and has three blocks of Treasuries as its assets. The banks use the Federal Reserve as their bank, in a similar way that Mary and Sara use their banks. In other words, the two banks store their extra cash reserve assets in their accounts at the Fed, which are the Fed’s liabilities.

The U.S. Treasury Department, representing the financial arm of the overall U.S. Federal Government, has 6 blocks of Treasuries outstanding as its liabilities. For the sake of simplicity it doesn’t have any assets listed, but in reality, its assets would consist of working capital, various federal buildings and lands and military assets, and its ability to tax citizens. Its 6 Treasury liabilities are owned by the Fed and Sara’s bank.

Between Mary and Sara’s cash, there are 4 deposit “D” blocks in the total system, which are assets for them and liabilities for their banks. Likewise, there are 3 reserve “R” blocks in the system, which are assets for their banks and liabilities for the Fed.

Intermediate State

Now, for the intermediate state, Mary and Sara enter into negotiations, and Sara agrees to sell her car to Mary for $1,000. Mary, however, only has $1,000 in deposits, and although she needs the car, she doesn’t want to be completely cash-less. So, she goes to her bank, and takes out a $1,000 car loan “L”. Mary’s bank creates a $1,000 deposit “D” for Mary, and creates a $1,000 loan liability “L” for her as well. For the bank itself, Mary’s new deposit asset is its new liability, and Mary’s new loan liability is its new asset. No reserves moved, but a new deposit was created.

Mary’s net worth is unchanged at $1,000 in total, but she now has $2,000 in deposits and $1,000 in loan liabilities ,and thus is a bit more leveraged. Mary’s bank’s net worth is unchanged as well, but it also leveraged itself up a bit, by creating a new asset and a new liability, since it expects that Mary will be able to pay the loan back with interest.

Neither the Fed nor the U.S. Treasury are involved yet.

There are now 5 deposit “D” blocks in the system rather than 4, because Mary’s bank is more levered with an additional asset and liability. It created new broad money by loaning a new deposit into existence. However, there are still 3 reserve “R” blocks in the system.

Ending State

For the ending state, Mary writes Sara a $1,000 check for the car, and therefore gives her the new deposit “D” that she just received from her bank loan. Sara receives the check and deposits it in her bank account, and her bank credits this by giving her an extra $1,000 deposit asset “D”, which becomes a new liability for her bank. Behind the scenes, Mary’s bank sends a $1,000 reserve block “R” to Sara’s bank to honor the check. So, Sara’s bank now has a new liability “D” in the form of Sara’s new deposit, but also has a new reserve block “R” as its new asset. Sara’s bank doesn’t have any creditworthy clients asking for loans at the moment, so it keeps its new reserve block at its Fed account for now.

The Fed’s ending state is unchanged on net, except that it updated its book-keeping for its two client banks when Mary’s bank sent Sara’s bank a $1,000 reserve block “R”. The Fed used to attribute “RR” to Mary’s bank and “R” to Sara’s bank, but now it attributes “R” to Mary’s bank and “RR” to Sara’s bank. These reserve blocks are liabilities for the Fed, but assets for its client banks.

The U.S. Treasury’s ending state is also unchanged, and unlike the Fed, it wasn’t even aware of the transaction at all.

In the final ending state, just like the intermediate state, there are still three reserve blocks “R” in the system, and there are 5 deposit blocks “D”, which is one extra deposit block compared to the beginning state, created by Mary’s bank loan.

The point of this example is to show how, when a bank uses its reserves to lend money, the reserves aren’t destroyed. The money shows up in another bank, and the reserve amount is sent there. The overall amount of reserves or base money in the system is unchanged, but the system becomes slightly more levered, and has more consumer deposits and therefore more broad money. In other words, the money multiplier ratio (D-to-R, broad money to base money) increased from 4-to-3 to 5-to-3.

Any bank can increase or decrease its own amount of reserves by buying or selling assets, or making loans. However, those reserves get moved around to or from other banks rather than created or destroyed. Banks can, however, create or reduce the amount of deposits leveraged on those reserves, depending on how much risk it wants to take on and how many creditworthy opportunities it has to lend money for.

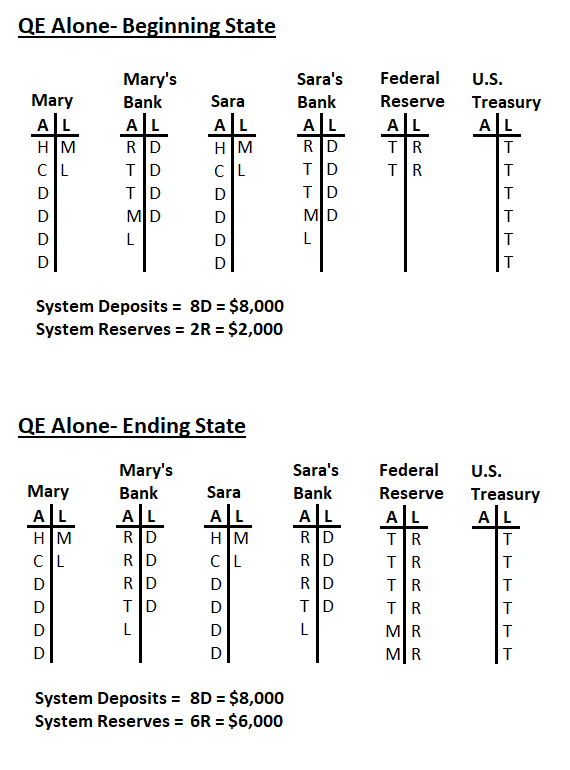

Example 2) The Fed Performs QE from Banks

This next example is a bit more realistic, with a more levered banking system. It involves the Fed performing quantitative easing on the banking system, meaning it creates new reserves to buy existing assets from the banks.

I’ll just show the beginning and end state here, and skip over the intermediate state:

Beginning State

Sara and Mary are identical to each other in this example. For assets, they each have a House “H”, a car “C”, and $4,000 in cash deposits “DDDD” at their banks. For liabilities, they also have a car loan “L” and a mortgage loan “M” owed to their respective banks.

The banks are also identical to each other in this example. They each have their $4,000 customer deposits “DDDD” as liabilities owed to Mary and Sara respectively. For assets, they each have “RTTML”, meaning one reserve block, two Treasury blocks, one mortgage loan block, and one car loan block. The banks are rather highly levered, with lots of assets and liabilities relative to their sole reserve block.

The Fed is small, with just “RR” in liabilities for their member bank reserve accounts, one for each, and “TT” in assets.

The U.S. Treasury has “TTTTTT” in liabilities, which are owned by the banks and the Fed.

There are 8 deposit blocks “D” in the system, and 2 reserve blocks “R”. So, the system money multiplier is levered 8-to-2, aka 4-to-1.

Ending State

In this example, the Federal Reserve realizes that both Mary’s bank and Sara’s bank have just one reserve block each. Assuming the banks are each required by regulations to have at least one reserve block, this means they can’t really lend any more, and can’t create more broad money. The Fed wants banks to be able to lend. So, the Fed decides to recapitalize the banking system by giving them plenty of excess reserve blocks. It can’t, however, legally just give free money to banks; it has to take something in return.

The Fed creates four new reserve blocks out of thin air, and gives two to Mary’s bank and two to Sara’s bank. These new reserve blocks become liabilities of the Fed, and become assets for the banks. In return, the Fed takes one mortgage block and one Treasury block from each bank. The Fed therefore adds “TTMM” to its assets and “RRRR” to its liabilities.

The banks are now much-better capitalized, with plenty of excess reserves as assets, and fewer Treasuries and mortgages. If they want to loan money or buy more securities, they now have plenty of excess reserves to do so with. However, they haven’t lent any more money yet, so the amount of deposits or broad money in the system remains unchanged. Underneath the surface, the banks are just less-leveraged, with plenty of reserves relative to deposit liabilities and overall assets.

Mary and Sara didn’t notice anything from beginning to end in this example. They have the same assets and liabilities that they started with. They weren’t even aware this happened.

The Fed is more leveraged now, with more assets and liabilities than it started with.

The U.S. Treasury didn’t change on net, except that it now attributes ownership of 2 of its Treasury note liabilities to the Fed instead of to the private banks, since the banks each sold a Treasury note “T” to the Fed.

There are still 8 deposit blocks “D” in the system, but the number of reserve blocks “R” increased from 2 to 6. So, the money multiplier in the system is now 8-to-6, aka 1.33-to-1. The amount of broad money hasn’t changed, but the amount of base money grew, due to the Fed’s decision to buy bank assets with new reserves. The banking system has been recapitalized, and has a lot more lending power now.

This is why, although many people think QE by itself is inflationary on consumer prices, it generally isn’t. The money isn’t getting out to consumers like Mary and Sara yet; it’s just internal to the banking system. This QE process sets the long-term stage for inflation as an early foundation, by recapitalizing banks and therefore being “anti-deflationary” by preventing a bank collapse and ensuring they have plenty of lending capacity, but it’s not inflationary yet.

Inflation would come if Mary and Sara have a lot more deposit money chasing the same amount of goods and services, but neither Mary nor Sara have more deposit money than they started with, and there’s no reason for anything to be inflationary. The amount of consumer deposits in the system hasn’t changed.

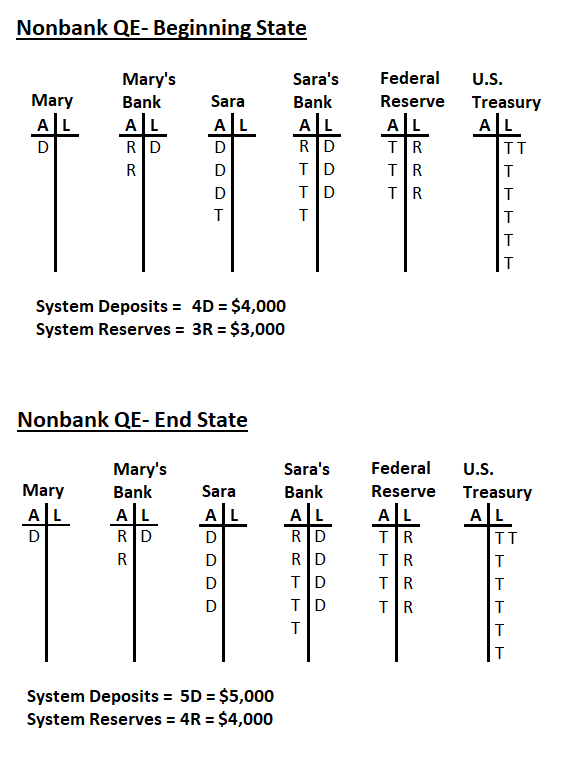

Example 3) The Fed Performs QE from Non-Banks

This third example starts with a simpler system again, very similar to Example 1. However, instead of having a car as an extra asset that she had in the first example, Sara has a Treasury note.

Sara decides to sell her Treasury note, but there aren’t many buyers for it at the moment. So, the Federal Reserve steps in and performs QE to buy it from her. The result ends up slightly differently compared to the Fed buying a Treasury note from the banking system.

Beginning State

Everything begins similarly to Example 1, except Sara has a Treasury note instead of a car. There are 4 “D” deposits in the total system, and 3 “R” reserves to start.

Sara decides to sell her Treasury note, but neither Mary nor either bank particularly want to buy it.

So, the Fed decides to buy it. The Fed creates a new bank reserve “R” out of thin air and gives it to Sara’s bank, and tells the bank to buy Sara’s Treasury note with a new deposit, and then to give the Fed the Treasury “T”.

The Fed, therefore, bought Sara’s Treasury note with a brand new reserve block, using the bank as the intermediary (so Sara and the Fed never talked to each other; Sara sold the Treasury note to her bank for a deposit block “D”, and her bank sold that Treasury note to the Fed, who bought it with a new reserve block “R”).

Ending State

After the bank completes this task, Sara has the same net worth as she started the example with, but replaced her Treasury “T” with an extra deposit “D”. Her bank also has the same net worth as it started the example with, but grew a bit bigger, with an extra reserve block asset “R” and an extra deposit block liability to Sara “D”.

The Fed grew a bit more leveraged as well, with an additional Treasury asset “T” and an additional reserve liability “R”, which it lists as an asset of Sara’s bank.

The U.S. Treasury didn’t change on net, except that it now recognizes Sara’s initial Treasury “T” as owned by the Fed instead of Sara now, since the Fed bought it.

Whether this is stimulatory for the economy or not depends on what Sara wants to do with her extra cash. She had “DDDT” and now she has “DDDD” as her assets. It’s still $4,000 but it’s a bit more liquid now. If the reason for her selling the Treasury was to raise more cash to do something big, like start a business or lend money to her friend to start a business, then it might be simulative. However, if she merely holds the money in an extra “D” deposit rather than the Treasury “T”, then she’s not using the money any differently. It then becomes a question of what her bank does.

Sara’s bank now has an extra reserve asset block and an extra deposit block liability compared to the beginning state, meaning it’s a bit bigger and has more lending power. It could finance a corporate loan, or a consumer loan, which would be stimulative. Or, if it thinks the economy is too risky, or if none of its creditworthy corporate or consumer clients are asking for a loan, it might just sit on its safe “RRTTT” assets and do nothing. In that case, this example wouldn’t be stimulative.

There are now 5 “D” deposits in the system compared to the beginning state that only had 4. In addition, there are 4 “R” reserve blocks in the system compared to the beginning state that only had 3.

So, there’s more liquidity in the system, with an increase in both base money and broad money. However, none of that broad money moved yet, and is just sitting there with Sara and her bank. Broad money velocity is low, in other words. There is more inflationary potential in the system, due to there being more broad money and reserves, but no consumer price inflation yet. Sara isn’t any richer; just slightly more liquid.

In this example, the Fed directly increased the amount of broad money in the system without banks doing any private lending, and without the federal government doing any spending, but it remains unclear if it will be impactful or not (subject to what Sara and/or her bank do with their extra liquidity). And even if it was impactful, the Fed wouldn’t be able to repeat it a second time, because neither Mary nor Sara (the two private non-bank entities) have any more Treasury notes to sell to the Fed.

If anything, it’s likely to be somewhat inflationary on asset prices, because Sara is flush with cash, and perhaps more willing to buy stocks, or buy more Treasuries, etc. She’s a saver and this might not make her spend more, but it might shift how she invests, with her extra liquidity.

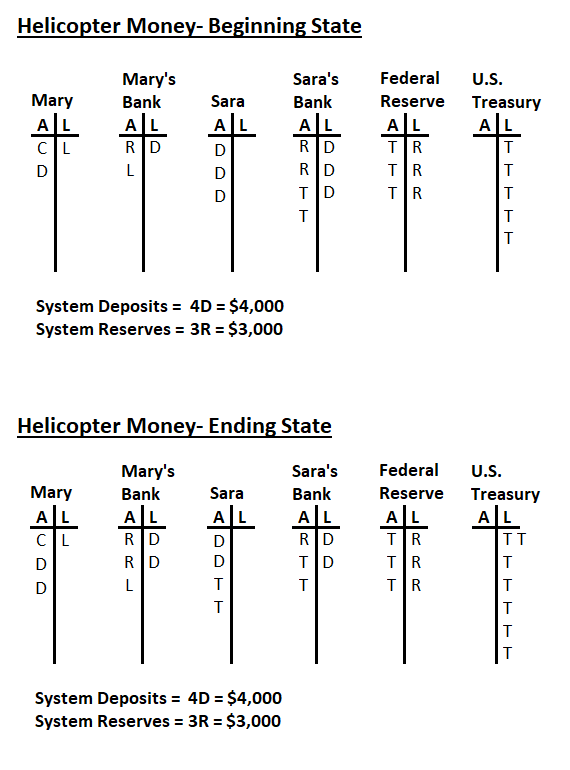

Example 4) Nonbank-Financed Helicopter Money

The first three example were separate cases, each meant to illustrate a different scenario.

These final three examples, Example 4, Example 5, and Example 6, however, build on top of it each other to show what happens when the U.S. Treasury gets involved with deficit spending, with differences depending on who finances that spending by buying the Treasury debt.

Example 4 begins with a relatively unlevered system. However, the economy is in a recession, and Mary just lost her job and only has a little bit of money in her bank account and is making her frustration known, so Congress authorizes the U.S. Treasury to send everyone $1,000 in stimulus checks, right to their bank accounts. This is known in economics as “helicopter money”, referring to a thought experiment of dropping money out of helicopters on consumers. The Treasury finances this by issuing Treasury bonds, which Sara, who has plenty of money and hasn’t lost her job, buys.

Beginning State

Mary has a car “C” and a deposit “D” as assets, and a car loan “L” as a liability. Mary’s bank has a reserve block “R” and Mary’s car loan “L” as assets, and has Mary’s deposit “D” as its liability.

Sara has three blocks of deposits “DDD” as her assets, and no liabilities. Sara’s bank has a blend of excess reserves and some Treasuries as assets “RRTT”, and has Sara’s three deposit blocks “DDD” as its liabilities.

The Fed holds the banks’ 3 total system reserve blocks as its liabilities, and holds 3 Treasuries as its assets.

The U.S. Treasury has 5 Treasury notes outstanding as liabilities, which are owned by the Fed and Sara’s bank.

Total system deposits are 4D = $4,000, and total system reserves are 3R = $3,000.

Intermediate State (not shown)

Although it is the originator of currency, the U.S. Federal Government legally has to finance its spending by receiving taxes or issuing Treasury debt to settle its account.

So, the U.S. Treasury sends a $1,000 deposit “D” block each to both Mary and Sara, deposited in their bank accounts. Both Mary and Sara are happy, because their net worth goes up by $1,000 each. Their banks get money deposited into them, and haven’t loaned any out yet, so they just keep this new cash at their Fed account as new reserves.

However, this is just a brief intermediate state. The Treasury now issues new Treasury note liabilities “TT” to pay for the expenditures it just made. Sara then decides to use two of her deposit blocks “DD” to buy those two Treasury securities “TT”, since they are yielding slightly higher rates than her bank deposit account yields.

If we imagine it happening simultaneously, what happened is that the U.S. Treasury extracted two deposit blocks from Sara (and therefore extracted two reserve blocks from Sara’s bank, as Sara’s bank settled the transfer with the U.S. Treasury), and the U.S. Treasury gave Sara two Treasury note blocks as assets in return. At the same time, the U.S. Treasury gave both Mary and Sara one deposit block each, and therefore gives one reserve block to Mary’s bank, and one reserve block to Sara’s bank, to settle the transfers.

Ending State

By the end of the transfers, both Mary and Sara are $1,000 richer than they started. Mary’s assets simply went from “CD” to “CDD” as she gained a deposit block. Sara’s assets went from “DDD” to “DDTT”, because she gained a deposit block but used two deposit blocks to buy two Treasury notes.

Mary’s bank is slightly bigger than it began, because Mary received a deposit block “D” and her bank was credited with a reserve block “R” to settle it (but also owes an extra liability “D” owed to Mary), and Mary hasn’t spent it yet. So, Mary’s bank has the same net worth (both its assets and liabilities increased by the same amount), but it’s overall combined assets and liabilities are bigger, and it has more lending power now because of that.

Sara’s bank is slightly smaller than it began, because although Sara and her bank received a deposit and reserve block respectively, Sara sent two deposit blocks to the Treasury to receive the Treasury notes, and therefore Sara’s bank sent two reserve blocks to the Treasury, which were then given back out, one to Mary’s bank and one back to Sara’s bank. Sara’s bank has the same net worth, but is simply smaller, as both assets and liabilities decreased, and its lending power is decreased.

The Fed is unchanged, except that it updated its book-keeping to attribute one of the reserve blocks “R” originally attributed to Sara’s bank, to being attributed to Mary’s bank instead. Its overall amount of Treasury note assets and reserve liabilities remains unchanged.

The U.S. Treasury is more leveraged, with an extra “TT” in debt liabilities outstanding, owed to Sara.

Total system deposits are 4D = $4,000, and total system reserves are 3R = $3,000, meaning that neither the total amount of deposits or reserves changed in the system from the beginning state to the end state. Deposits and reserves were just moved around a bit within the system.

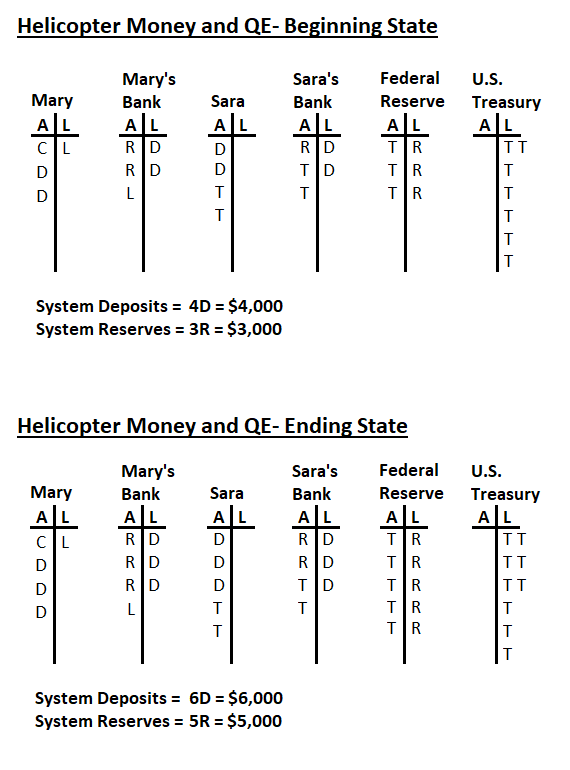

Example 5) Fed-Financed Helicopter Money

Example 5 starts exactly where Example 4 left off, and builds from there.

Both Mary and Sara are happy because they got some extra money in the previous example. However, Sara is just prudently saving her money due to uncertainty about the economy, and Mary still doesn’t have a job so she is also just saving her money, and their favorite restaurants and vacation spots are closed due a virus pandemic anyway.

Some politicians want to give $1,000 to everyone every month for the next year, due to so many displaced workers like Mary having so little money and with no jobs. Other politicians say, “no, that’s too much federal debt, let the economy try to heal itself.” The politicians argue for a couple months and then eventually compromise and decide to send everyone $1,000 one more time, to see if that helps. So, Congress authorizes the U.S. Treasury to send out another $1,000 to everyone.

This time, instead of Sara buying the new Treasury liabilities with her existing deposits, the Fed buys the new Treasury liabilities with new reserves.

Beginning State

Sara already owns a lot of Treasury notes and sees that the U.S. Treasury will become even more indebted after it sends out all this money without raising taxes, so she doesn’t want to buy any more Treasury notes. So, how will the U.S. Treasury finance this second round of helicopter money?

Well, because there is a lot of new Treasury note issuance but nobody desiring to buy it at current prices, the Treasury note market suddenly becomes illiquid, and prices start to fall (meaning yields start to rise). Sara and her bank both get nervous, because they own a lot of Treasury notes.

The Treasury note market briefly looks like it did in March 2020: totally illiquid, with yields extremely volatile.

However, this problem doesn’t last long, because the Fed says, “It’s fine everyone! We’ll buy the extra Treasury note issuance. Relax.”

So, the Fed creates two new bank reserve blocks “RR”, and gives them to the Treasury in exchange for the new Treasury debt liabilities, “TT”, which become the Fed’s assets. Technically, the Fed can’t legally buy directly from the Treasury, so they agree to transfer the securities through one of the banks as a brief pass-through entity.

The U.S. Treasury then sends a $1,000 deposit “D” each to Mary and Sara, and settles this by sending a reserve block “R” to each of Mary’s and Sara’s banks.

Ending State

Mary and Sara are both $1,000 richer, again. They each have a new $1,000 deposit “D”.

Mary and Sara’s banks are both bigger, although their net worth didn’t change. They each have an extra $1,000 reserve block “R”, but also each have a new $1,000 liability block to their customer deposits “D”.

The Fed is bigger and more levered, with $2,000 more assets in the form of Treasuries “TT”, and $2,000 more liabilities in the form of reserves “RR” that they hold for the banks.

The U.S. Treasury is bigger and more levered, with $2,000 “TT” in more debt liabilities outstanding.

System-wide deposits (broad money) increased over the beginning state, from 4D = $4,000 to 6D = $6,000. System-wide reserves (base money) also increased over the beginning state, from 3R = $3,000 to 5R = $5,000.

This was outright money-printing. The amount of broad money and base money in the system went up by a lot. Mary and Sara are richer, and their banks are bigger. Money was injected into the system, without being extracted anywhere from the system, because the deficit spending was financed by the Fed creating new bank reserves to buy the Treasury notes.

The Treasury and Fed can perform this repeatedly if they want, any number of times, although they both know that if they do it too much, it could cause consumer price inflation.

Whether it is inflationary for consumer prices or not, however, depends on whether Mary and Sara still have confidence in the value of their deposits, and whether they go and spend them or not. It’s also potentially inflationary for asset prices; Sara in particular is flush with assets and more likely to put some money to work in stocks other gold or other assets than she was before.

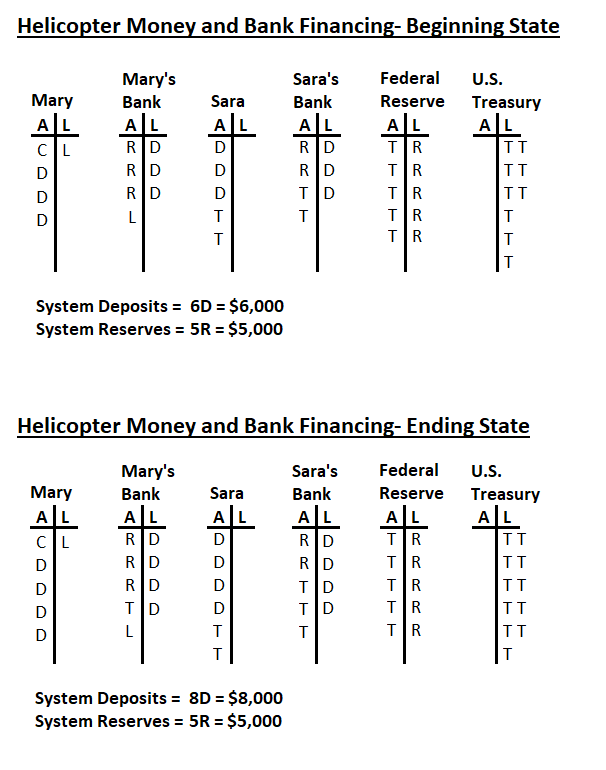

Example 6) Bank-Financed Helicopter Money

Example 6 starts exactly where Example 5 left off. Both Mary and Sara are happy because they got some extra money in the previous example, again.

The pandemic eased a bit, and Mary got a new job, but realizes she needs to keep more cash on hand in case she loses her job again in the future. She learned a lesson about saving, in other words.

Sara was already a saver, and hasn’t been spending extra money yet either. Sara, however, is considering going on a vacation or buying a car, now that she’s feeling a bit more confident with so much cash. She’s also not sure about the value of her money, as she watches the broad money supply expanding so rapidly due to these helicopter checks that everyone is receiving. Car prices are starting to go up, probably due to so many people receiving stimulus checks, so there seems little reason to wait.

However, because the economy is still sluggish, with many people saving more than they used to, Congress decides to do yet another round of $1,000 helicopter checks to everyone, and issue $2,000 in new Treasury note liabilities “TT” to pay for it. This is it, the final stimulus round!

Fortunately for the U.S. Treasury, the banking system has tons of excess reserves due to their previous round of helicopter spending that the Fed bought with new reserves, and so this time, the banks each agree to buy one Treasury note “T” with one of their excess reserve blocks. (In fact, the banks don’t have much of a choice, because as primary dealers they “have” to buy Treasury notes at auction if they have enough liquidity to do so, and if neither Mary nor Sara nor the Fed agree to buy the Treasury notes from them, they get stuck holding the Treasury notes.)

Beginning State

System-wide deposits are 6D = $6,000. System-wide reserves are 5R = $5,000.

Here’s what happens if we imagine the process happening simultaneously. The U.S. Treasury sends Mary and Sara each a $1,000 deposit “D” block, and sends their banks each a $1,000 reserve “R” block to settle it. The U.S. Treasury then issues two new Treasury note liabilities “TT” to pay for it. The banks each send a reserve block “R” to the U.S. Treasury in exchange for one of those Treasury notes “T”.

Ending State

Mary and Sara are, yet again, $1,000 richer. They each have yet another deposit block “D” added to their assets.

Their banks have the same amount of reserves they started with, because they each received a reserve block “R” from the U.S. Treasury’s helicopter deposits to their customers, but since each bank also sent a reserve block “R” back to the U.S. Treasury to pay for the stimulus, they each ultimately received a Treasury note “T” as an asset instead. They still have the same amount of reserve blocks that they started with, but they each have an extra asset “T”, and they each have an extra deposit liability “D” for their customers. So, they are a bit more levered overall.

The Fed didn’t change at all from the beginning of this example, although it did some book-keeping for the reserves moving around and ending back in the same place.

The U.S. Treasury is $2,000 or “TT” more in debt than it started the example with.

System-wide deposits increased by $2,000 or “DD” from 6D = $6,000 to 8D = $8,000. System-wide reserves are still 5R = $5,000. So, the money multiplier increased a bit, from 6-to-5 to 8-to-5. Broad money increased, but base money remained the same.

Will it be inflationary? It depends on what Mary and Sara do from here, but most likely at this point, yes. Sara now has tons of cash and is concerned about the value of that cash, so she decides to spend money on a vacation and buy that new car, or buy stocks or gold or real estate, or something. Even Mary decides to eat out at restaurants more, now that she has more cash than usual. Other people seem to be doing the same; prices of things are inching up each month.

There is now $8,000 in total deposits (broad money) in the system, compared to the start of Example 4 where there was only $4,000 in deposits. However, the amount of goods and service in the economy have not doubled. So, if Mary and Sara and others decide to start spending their money, it could indeed result in a lot of money chasing a limited supply of goods and services, and therefore could push up consumer prices and be inflationary.

In response to high inflation, the Fed’s normal tool would be to raise interest rates. However, with U.S. Treasury debt so high at that point, the Fed’s ability to raise interest rates would be limited, since it would result in an acute fiscal crisis as rising Treasury debt interest eats up a large part of the fiscal budget. So, either the Fed would have to let inflation run hot and inflate away part of the debt and keep creating Reserve blocks to buy new Treasury notes as needed to keep Treasury security yields low (which they did back in the 1940’s), or the U.S. Treasury would have to restructure/default on the central bank portion of U.S. Treasury debt.

So, the Treasury+Fed combo has all the power to boost the broad money supply enough to cause a rising trend shift in inflation, but when they do with such a highly-leveraged U.S. Treasury, they face some consequences in their ability to constrain it.

Example Summaries and Findings

If we analyze all of the examples, we see a few observations:

-Banks can create new deposits and increase the the amount of deposits (broad money) in the system by lending. Lending creates deposits. This lending doesn’t change the amount of base money (reserves) in the system, but it moves those reserves around from one bank to another, and levers those reserves up. This is the money multiplier ratio, the ratio of broad money to reserves in these simplified examples. Although the banks can create new deposits and increase broad money by lending, it is not “money printing” because the banks are simply making decisions regarding how much to lever themselves up relative to their cash reserve assets, and they are constrained by various regulatory standards for how much leverage they can have.

-The Fed alone has the power to create new bank reserves, and to therefore increase the amount of bank reserves in the system (base money) or more broadly, the total amount of water in the three-bucket system analogy. However, if it buys assets from banks, it doesn’t directly lead to more deposits (broad money) being in the system. It de-levers banks and gives them more capacity to lend and create new deposits (broad money), but whether they will or not is up to them. On the other hand, if it buys assets from non-bank entities like Sara (using the banking system as its intermediary), it can slightly increase deposits (broad money) in the system, but only to a limited extent, based on limited amounts of non-bank entities holdings’ of Treasuries that they can sell. It is, in this sense, very limited “money printing”.

-On behalf of Congress, the U.S. Treasury can give more deposits to somewhere in the system, but deposits also get extracted back out of the system when non-bank entities like Sara buy the Treasuries that are used to fund this expenditure. So, it doesn’t necessarily create new deposits or new reserves. This is what deflationists often refer to as the “crowding out effect”, meaning that the U.S. Treasury can extract capital from somewhere in the economy and inject it somewhere else in the economy, if it runs large deficits and builds up federal debt, and it displaces nonbank capital that could have been used for something else. This is not “money printing” since it just moves things around and levers up the Treasury.

-However, if the Treasury and Fed work together, they can rapidly increase both the deposits (broad money), and bank reserves in the system (base money), without extracting deposits from anywhere in the system. In this process, the Treasury injects money into the economy by spending, which creates new deposits, but instead of that money being extracted from deposits somewhere else in the economy, the Fed finances those new Treasuries with newly-created bank reserves out of thin air, and thus levers itself with additional assets (the new Treasuries) and additional liabilities (the new reserves attributed to the banking system). It doesn’t matter if banks lend or not; the Treasury+Fed combo goes around the bank lending channel by just giving people and businesses more deposits (broad money). This outright increases the net worth of Mary and Sara in the examples, and increases the size of their banks including broad money supply and bank reserves (but the banks’ net worth remains unchanged), and levers up both the Fed and the U.S. Treasury. There is no limit to the amount they can do this, other than the fact that it would eventually be inflationary if done too much and too rapidly relative to the amount of goods and services and productive capacity in the economy. This is outright “money printing”, although there are some checks and balances since fiscal changes have to be passed by Congress and signed into law, rather than done unilaterally by the Fed.

-Additionally, if the U.S. Treasury injects money into the economy with large deficits and the Treasuries to finance it are bought by a well-capitalized banking system (usually as a result of the Fed already having capitalized banks by creating excess reserves in the recent past), it also increases the deposits (broad money) and levers up the money multiplier. This can be done quite a bit if banks start with excess reserves, because every time the federal government injects more money into the system, it creates more bank deposits, which replenishes the reserves that the bank spent buying Treasuries, and thus gives the banks more ability to buy additional Treasuries. This is mostly “money printing”, although to maintain leverage ratios, the banks need to start with plenty of excess reserves.

-If there is a lot of broad money added to the system, with both Mary and Sara confident to spend, it could very well be inflationary. Plus, now that Mary and Sara are richer than they started, they might feel more confident to take out a mortgage loan or business loan from their bank to buy a house or start a business, and their banks are more willing to lend it now because Mary and Sara both have plenty of net worth and creditworthiness. This could very well be inflationary.

-There are proposals for central bank digital currencies, which if enacted may allow the Fed to inject money to consumer deposits without going through Congress. This would likely require an overhaul of the Federal Reserve Act, and would substantially change the nature of the system. Some folks argue that this would be necessary for inflation to happen, but inflation can already happen within the existing framework through the combination of fiscal deficits and QE monetization of those deficits. The current framework requires Congress to go along with it rather than performed unilaterally by the Fed, and thus has checks and balances in the system.

Implications: Focus on Broad Money

It’s fashionable to debate lately whether QE is inflationary or not, and whether central banks have run amok.

However, for more fruitful results as it relates to analyzing inflation vs deflation and the associated impacts on various asset classes, investors should focus on fiscal spending, especially when it is combined with monetary financing to pay for it. Are major fiscal deficits happening or no? How big are the deficits, relative to the deflationary backdrop? Who are the deficits targeting? Who is financing the deficits by accumulating the Treasury securities?

And then specifically, look at what the broad money supply is doing. Is it going up, or no? At what rate?

Banks are already well-capitalized. The big non-fiscal QE for bank recapitalization was done back in 2008-2014. Now, with massive Treasury debt in the system and interest rates at zero, fiscal authorities find themselves spending more, and running larger deficits, with the Fed and banking system buying the majority of their Treasury note issuance.

We have division of fiscal and monetary powers, and only when the powers combine (like in the 1940’s and again in 2020, where the Treasury runs massive deficits and those Treasury notes are accumulated by the Fed and banking system), does it become outright money-printing. It doesn’t require any change to existing laws for them to do that; they use banks as pass-through entities and other structures as needed to do what they do.

QE alone, where the Fed buys existing assets mostly from banks, is simply anti-deflationary, to recapitalize a banking system and fill it up with excess reserves. It’s not outright inflationary because it doesn’t directly increase the broad money supply. If the Fed buys existing assets from non-banks, it only increases broad money a bit, around the margins.

Meanwhile, large fiscal deficits funded by QE (the central banks monetizing deficit spending by buying any of the excess Treasuries over the real demand for them), actually is pro-inflationary, because it gets money directly into the economy, into the broad money supply, and can be done with no limit except for inflation that it would eventually cause when done to excess.