A most peaceful revolution

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

A most peaceful revolution

By Nic Carter

Posted September 7, 2019

Art by Jason Benjamin (@perfecthue)

Art by Jason Benjamin (@perfecthue)

People should not be afraid of their governments. Governments should be afraid of their people.

– V, V for Vendetta

It’s submission,” Rediger murmured. “The shocking and simple idea, which had never been so forcefully expressed, that the summit of human happiness resides in the most absolute submission.

― Michel Houellebecq, Soumission

Make no mistake, Bitcoiners are revolutionaries

Libertarians had it all wrong. They sought to shrink the State’s influence by participating in the democratic process. This has been and remains a hopeless, Sisyphean task. Like Tolkien’s Ungoliant, the State hungers without limit, and its most engaged constituents duly reward it with votes for more growth, receiving in exchange ever-greater entitlements. Libertarians are, in a word, stuffed. Like the creeping gelatinous menace in The Blob, the State grows regardless of what you throw at it. Participating in democratic processes empowers it and entrenches the Orderly Civic Ritual as the only legitimate mode of political engagement.

Bitcoiners reject this: they understand that the only winning move in politics is not to play.

Instead, they kicked over the chessboard and strutted around as if they had won. Bitcoiners chose to abandon the rules of engagement and began work on a monetary system totally outside the purview and supervision of the State, entirely without restriction. Ultimately, they anticipate a system which permits unfettered commerce, provable-reserve free banking (unlike the obscure socialized-loss mess we rely on), renders capital controls obsolete, frees savers from state-sanctioned theft by inflation, and eventually disempowers the State entirely, shrinking its monetary toolkit.

This proposition predictably enraged the State-dependent intelligentsia, the pundit class, and the press, which has backslid from its Fourth Estate perch as a proud critic to a feeble establishment mouthpiece. No surprise at all that Bitcoin’s most hysterical critics overwhelmingly benefit from their proximity to or membership in the Beltway bureaucracy or the overseas equivalent. Academics, the beneficiaries of a rampant government-guaranteed student loan bubble; politicians and ex-politicians, who time and time again manage to turn their political clout into personal wealth (how curious!); journalists, reduced to meekly passing on State messaging in a futile effort to build a moat against insurgent media startups and Youtubers with 1000x their clout; economists, forced to peddle Keynesian narratives for grants and tenure.

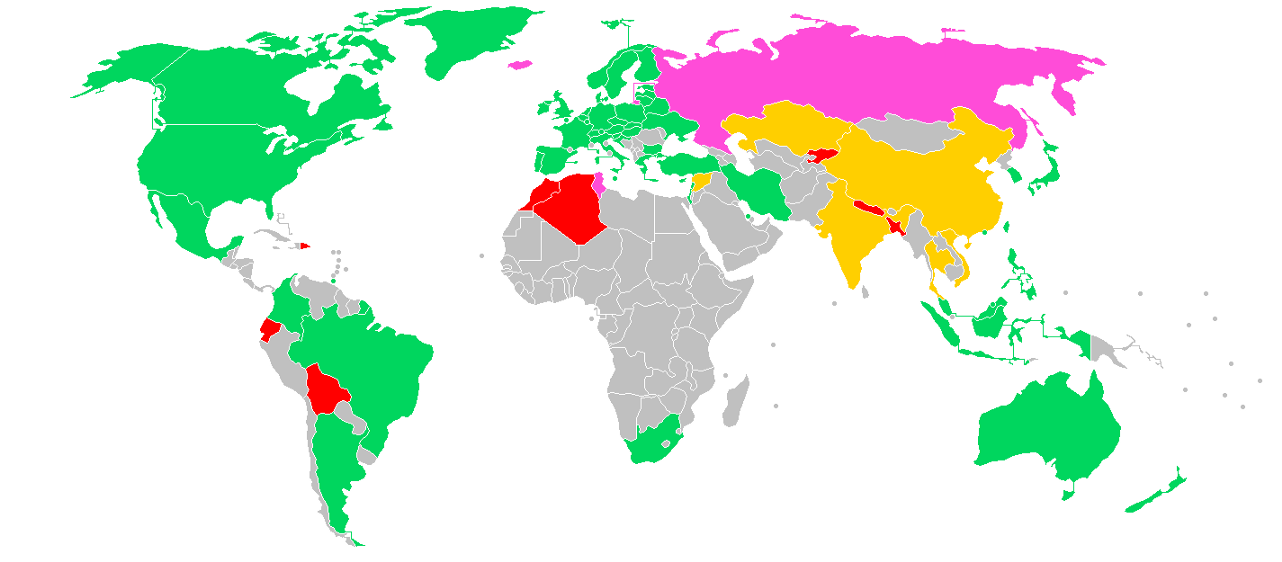

Thus, met with the screeching bile of the chattering classes, Bitcoiners went from utopian tinkerers to dissidents in short order — even as the movement was still in its infancy. Check the financial pages of your newspaper of record; you will find nothing but derision and mockery (and the very occasional nod of grudging acceptance). This is for an asset class which went from 0 to $200 billion in a decade, with no venture backing, no IPO, no corporate entity, an absent founder, and a purely open-source body of maintainers. In the U.S., the government saw fit to give Ross Ulbricht two non-parole-eligible life sentences plus 40 years for the crime of creating a free market denominated in Bitcoin. China has banned the formal exchange of bitcoins; India is mulling over legislation to make mere ownership illegal.

Legality of Bitcoin — Green: permissive; Orange: some restrictions; Pink: contentious; Red: Hostile. (Source)

Legality of Bitcoin — Green: permissive; Orange: some restrictions; Pink: contentious; Red: Hostile. (Source)

.png){kind=link}

We aren’t in the prelude to war; we are living it. Of course, war doesn’t look much like the savage romps of yore. But this has been the case for a long time. Gone are the days where men nobly lined up in front of each other and fired until one side ran out of able bodies. We no longer scramble out of the trenches at the sound of a whistle to the chatter of machine guns. Open warfare is virtually obsolete. Instead, contemporary conflict consists of a melange of insurgencies, IEDs, sanctions, emotionless drone strikes, and strategic infrastructure targeting through operations like Stuxnet. Since conventional warfare has migrated to the virtual, why not rebellion, too?

And it is a rebellion, make no mistake. Cryptocurrency, despite the earnest protests of some of its lily-livered adherents, remains manifestly independent and ultimately hostile to the State. It cannot be regulated, captured, or rendered compliant. The Silk Road was not an aberration or historical anecdote to uneasily chuckle over in hindsight. It was a profound demonstration of Bitcoin’s superior purpose and utter indifference to the shackles burdening the financial system. The current State, in its bloated and rapacious form, craves not only your corporeal submission, but it demands an endless torrent of metadata and analytics too. Your finances are not your own; they are scrutinized and require approval at every step. If you operate even slightly outside of the mainstream, you risk getting your savings confiscated with no recourse. Those armored personnel carriers aren’t going to pay for themselves.

Cryptocurrency tilts at the State

Just as sixteenth century Protestants began to question the official doctrine of indulgences and the scope of the Pope’s authority, so too came to wonder a ragged bunch of nerds and cypherpunks: is inflation really necessary? In a free market economy, should central banks really have the right to arbitrarily set the price of money? Should the State really have full discretion over one’s saving and spending? Should savers really be forced to trust banks (and ultimately, the taxpayer) to redeem and honor their savings? What does an entry in a bank’s database really mean?

Rare image of Bitcoin in physical form

Rare image of Bitcoin in physical form

Genuine cryptocurrencies — alternative monetary systems, really — threaten the State and its hangers-on. Bitcoin is absolutely profane, so much so that it hardly bears contemplation. It challenges the State’s most treasured privilege: its ability to finance itself through inflation and seignorage.

Cryptocurrency, chiefly Bitcoin so far, has already begun to affect central bank policy. I am not exaggerating when I stress its geopolitical significance. Combine a free market for money with the distribution rails of the internet and you get a very toxic stew. Let’s consider a few ways that cryptocurrency has begun to affect the state.

First off, as noted by Gina Pieters (2016), the existence of liquid Bitcoin markets poses a significant threat to countries that rely on capital controls in order to retain a managed exchange rate.

Bitcoin creates a problem for Argentina and similar countries; it makes circumventing capital controls easier. As demonstrated in Pieters and Vivanco (2016), government attempts to regulate the globally accessible bitcoin markets are generally unsuccessful, and, as shown in Pieters (2016) and Chart 4, bitcoin exchange rates tend to reflect the market, not official exchange rates. Should the flows allowed by bitcoin become big enough, all countries will have, by default, unrestricted international capital markets.

This is not insignificant; a good fraction of the world’s population lives under capital controls, including residents of Brazil, Russia, Indonesia, Taiwan, China, and Argentina. A critical piece of the State’s monetary toolkit is being eroded.

Being highly liquid and traded globally, Bitcoin also has the practical effect of casting light on exchange rate manipulation, as discussed in another paper by Dr. Pieters. Bitcoin trades can be used to derive a passthrough estimate of the ‘street price’ of local currencies, even when the government is publishing false exchange rates. Bitcoin is fast growing into its role as a universal measuring stick.

One example: publishing information on the street value of the Bolivar is illegal in Venezuela, as the regime has a strong interest in maintaining a tight grip on the narratives around their currency. The most popular exchangerate-tracking website in Venezeula, DolarToday (run out of Miami) uses LocalBitcoins trades to derive an implicit USD-Bolivar Soberano street price.

**Source: https://dolartoday.com

**Source: https://dolartoday.com

It’s no surprise that the world’s most vibrant p2p Bitcoin markets tend to be in States with capital controls, highly inflationary sovereign currencies, or capricious governments. This analysis by Matt Ahlborg, again relying on LocalBitcoins data, demonstrates that Bitcoin is most traded on a per capita basis in Russia, Venezuela, Colombia, Nigeria, Kenya, and Peru. It is sometimes said that currency competition is like outrunning a bear; you only have to outrun your slowest friend. The dollar is probably not threatened by the existence of Bitcoin, but the world’s couple dozen most inflationary currencies absolutely are.

As Hasu has written, Bitcoin provides a stable system of property rightswithout any reliance on the State (and the implicit threats of violence that underscore it all). This is mostly irrelevant in the West where property rights are generally respected; but it is a matter of life and death elsewhere. No small irony, then, that cryptocurrency’s staunchest critics tend to be precisely those individuals that have never had reason to mistrust their government with their savings. One’s reaction to Bitcoin is a shibboleth; it reveals whether an individual is aware of the vicious effects of inflation and an unreliable banking system. The loudest Bitcoin deniers simply reveal their ignorance and anglocentrism.

Indeed, new findings from Raskin, Saleh, and Yermack evaluating currency crises in Turkey and Argentina confirm that the cryptocurrency has its most immediate applicability outside the developed world.

At first blush, Nakamoto’s vision did not pan out, except insofar as a new option was created that a majority of people choose not to use. When one investigates the developing world, however, the story is a little different. […] [Turkey and Argentina] are the first currency crises since the creation of bitcoin, and therefore they offer an opportunity to investigate the impact that alternative digital currencies have on unstable sovereign currencies. Extrapolating out, this may show that Nakamoto’s vision has come to fruition. Although private digital currencies have not replaced the dollar, their mere existence may have a counterfactual impact in that they exist as a check on both fiscal and regulatory policy.

Specifically, the authors find, somewhat unsurprisingly, that “citizens gain from the existence of the private digital currency,” in particular through a new option for diversification, which “generates welfare gains for citizens.”

Critically, the authors also find that

[T]he existence of the private digital currency disciplines monetary policy by creating an alternative to local fiat. That monetary policy discipline reduces inflation and results in higher returns from investment which in turn encourages higher local investment.

As economics 101 holds, busting a monopoly (governments are effectively local monopolists in the market for money) by introducing competitors should make the market fairer for consumers. Faced with no alternative, citizens were previously forced to save in their local currency and tolerate inflation. Now with an effective off-ramp, citizens have the choice to exit the local monetary regime, at significant cost to the central bank (selling their local currency increases the velocity of money and worsens inflation). So the mere existence of Bitcoin instills monetary discipline on a central bank which might otherwise pursue a ruinous level of debasement.

Not for the faint of heart

Because of the extremely high stakes, reinventing a monetary system is a profoundly unpleasant task. It takes irrational zeal and an unwavering commitment to a firm vision of the future. Given the immensity of this task, and the existential threat it poses to the state, only the most committed could possibly take up the cause. The great sin of altcoiners is not that they backed the wrong horse, but that they did so with insufficient conviction. They sold a dream that they themselves did not truly believe.

How many cryptocurrency entrepreneurs would tell you with complete sincerity that they were building a system to last decades and face the State head on? How many would willingly face jail for their beliefs? Very few, I suspect.

The insipid tone at the top percolates throughout the organizational pyramid. Hence the distinction between the “communities” of underwater holders that urge each other to buy the dip as their coins bleed, and a resilient community that embraces the volatility and keeps the faith. Superficially, Bitcoin and its many blockchain-employing clones are similar. The main differentiator is soul. It’s not that alternative chains are immoral or opted for an inferior set of values, it’s that they are entirely nihilistic. Progress and cosmetic innovation is prided over building lasting, non-State institutions.

For sure, the profit motive drives many towards Bitcoin. Yet something far deeper and more primordial drives Bitcoiners too — the possibility of building a parallel, reliable financial system which is functional, open, and independent of governments or unaccountable corporations. Of course, this motivation does not drive Bitcoiners alone. But Bitcoin has undeniably made the most progress towards the separation of money and state, and has suffered the brunt of political attacks so far. No other project has been exposed to so much media hysteria and so many early roadblocks.

Not the case, for the would-be alternatives. Success for upstart cryptocurrency founders is an exit. The presale; the markup; the dump on retail. The allure of launching a new blockchain was simple; money has the largest TAM of any product in existence, and to own even a fraction of it all by minting a new currency and retaining some share promised Crassus-tier wealth. But wealth does not inspire, especially when it is obtained at the expense of the would-be converts. Dumping one’s presale is no way to win the dogmatic, undying support of millions of willing footsoldiers.

As Taleb says: don’t tell me what you think, show me your portfolio. What better case study than Block One, creator of EOS, the would-be Blockchain 2.0, divesting its treasury and choosing to hold 140,000 BTC on its balance sheet?

The only questions that matter

After ten years of experimentation, misallocated capital, and hubris, we have learned valuable lessons about value accrual. The scientists and engineers mistook the monetary and political revolution for a technological one. Their experiments were impregnated with an insistent prescriptivism:

“If only we can create a more efficient or performant database structure or sybil resistance algorithm, we can crack the case and create the ultimate winning cryptocurrency.” This mindset, astonishingly, is still prevalent today. But it is hopelessly flawed. These are political and social experiments first. The most important factors in minting an entirely new monetary system from scratch are not the technical implementation details, but rather the provision of compelling answers to questions like:

- what gives you the right to mint a new currency and to have disproportionate influence over its fate?

- why are you choosing to reject all of the alternatives and proposing to replace them with your own?

- from where do you derive your authority?

- how are you enshrining fairness and equality of opportunity in the distribution of this new money?

- how will you ensure that the system is free from corruption when even the U.S. Federal Reserve is vulnerable to political capture?

Bitcoin has clear answers to all these questions. Its imitators do not. Not only do they not have reasonable answers, their creators aren’t even aware that these are the appropriate questions to consider.

Above: a list of all the utility tokens that fulfilled their stated purpose and saw meaningful adoption

Above: a list of all the utility tokens that fulfilled their stated purpose and saw meaningful adoption

We know now that utility tokens are chimeras. It didn’t take a genius to spot this, but the empirical reality has set in for good now. A utility token world is analogous to one in which a frictional forex transaction is required not for interstate travel as is the case today, but from one store to the next. Utility tokens proposed a dismal regression, and we are better off now that they have been repudiated. The only cryptocurrencies worth creating are those that aim to be money; and this necessarily entails tilting at the State.

But going toe to toe with the State requires tens or hundreds of millions of diehards that believe in a stable set of values and are willing to put capital to work supporting it. Clever cryptographic primitives and tinkering with new byzantine-fault-tolerant algorithms cannot inspire and win devotion. There must be some core set of values which are prided over everything else. Most monetary pluralists in the industry justify their stance with recourse to trite cliches like being “pro innovation”. This is incoherent; if they reject incumbents like Bitcoin and agitate for some alternative project, they too will face objections from the crypto progressives to their left.

“Why settle for x blockchain 2.0? Why not p, q, or r?” The question is a compelling one. Absent deeply held shared values clearly instantiated by one’s chosen project and one’s chosen project alone, there is no defense of the crypto-progressive’s alternate chain, aside from sunk costs. Out of necessity, the progressive becomes a reactionary.

Values set Bitcoin apart

So what are these values that Bitcoiners hold dear? Bitcoinism is an emergent political and economic philosophy combining strains of Austrian economics, libertarianism, an appreciation for strong property rights, contractarianism, and a philosophy of individual self-reliance. Some libertarians will recoil at social contract theory, understanding it to be coercive (since one is not actually offered a political contract to sign at birth or at maturity). Not so with Bitcoin. No one is defaulted in: it offers a fairly explicit contract to would-be users. You have the right but not the obligation to participate in the most transparent, auditable, debasement-free, and and well-defined monetary system the world has ever known.

Other values which I would consider critical to Bitcoin include cheap validation (so anyone can participate), full auditability (so no unexpected inflation), fairness in issuance (everyone regardless of status paid “full market price” for their BTC, either on an exchange or by mining), backwards compatibility (soft forks rather than hard forks preferred), and of course the open validator set, to prevent validator collusion and the inevitable censorship it leads to. Pose the question to your favorite Bitcoin alternative. What are the values that motivate the project? If they exist, you will notice that they are generally weakly held; innovation is prided over consistency.

Thus Bitcoiners strike a profound contrast to the opportunists who envision success as a financial exit from their token project. For Bitcoiners, success consists of a day when no exit is required. Their admittedly eschatological philosophy anticipates a time when they will be able to participate in a closed loop Bitcoin economy, free from the vicissitudes of the legacy financial system. They do not dream of a financial exit, at least not in the venture sense. They crave instead a system built on a monetary standard which does not arbitrarily debase savings because monetary discretion of any sort is completely absent.

And they are serious about retaining these foundational qualities. Not only must the predefined supply schedule be kept, but it is so completely fundamental to the protocol and system of property rights that to alter it would cause the old system to cease to exist. Capped supply is not a feature of Bitcoin; the supply cap is Bitcoin. It is ontologically critical, like the consent of the governed is an inalienable component of the U.S. Constitution. Sure, you could overthrow the government and install an autocratic government identical in name, but that would not be the original. Its very substance, relying as it does on foundational values, would be changed. The ideals are not contingent. They are not a mere implementation detail. The values are the system; the system encodes the values.

And what better role model than Satoshi himself. Satoshi is the ultimate sacrificial hero — he spent an age building Bitcoin from scratch, released the code, ran the project for a brief time, and then stepped away, permanently. The coins he mined — out of necessity, to support the network when no one else would — were left untouched. To call this effort Promethean is almost painful in its aptness. Satoshi daringly stole the State’s most treasured possession — its right to unencumbered money creation — and gave it to the people in the purest way possible.

So what of the State? If the threat is so severe, why does it not intervene? Frustratingly, Bitcoiners tend to have an answer to every objection.

The reality is that a ban wouldn’t stop Bitcoin, unless you believe that the international community, increasingly trending towards chaos and an anarchic morass, would unite to tackle this threat. Imagine that! North Korea, Iran, the U.S., China, Russia, and Saudi Arabia all aligned in a common cause. And this is considered one of the best arguments against Bitcoin by its critics.

Damned if they do, damned if they don’t

Let’s say major countries colluded to ban Bitcoin. This would merely turn Bitcoin into a black market commodity. But it would not be sufficient to obliterate it. Consider for a second another widely banned commodity, reliant on significant energy for creation, produced by a mixture of industrial and informal entities, chiefly circulated on the black market, enjoyed by millions. I’m referring of course to cannabis, and you can probably obtain it from a dealer nearby — legal or not — in under 30 minutes. To believe a ban would abate Bitcoin’s popularity is comical. It would only reinforce Bitcoin’s literal raison d’être: protection from the whims of the capricious State. A State so obviously threatened by a financial commodity would reveal itself to the world as paranoid and controlling, making its true parasitic nature very clear.

Ironically, the State’s best response to Bitcoin and Bitcoin-inspired private monies is to meet the demands of the techno-Austrians and reform itself.This would require ending the debasement of currency, ending the inequality-boosting loose money regime, ceasing interference in economic cycles (which simply makes them more severe), ending the hubristic attempts to set a price for the time value of money, and ending the use of financial institutions as weapons of war.

For any of this to change in the near term seems vanishingly unlikely. The neo-Keynesian theory _du jour _is a delightfully accelerationist atrocity named “Modern Monetary Theory,” according to which the State can ostensibly purchase unbounded quantities of any good available for sale in its own currency, consequences be damned. Our current moment is one in which socialist-bordering-on-fully-collectivist politicians are elevated and hankered for by their ever more subservient constituents. Bernie; Elizabeth Warren; Ocasio Cortez; Jeremy Corbyn. In the developing world, you have Kirchnerism retaking control in Argentina, sending all financial assets spiraling towards 0 as collectivism reasserts itself. In Argentina’s typically more free-market friendly neighbor Chile, two unabashedly communist lawmakers are now setting the agenda. Venezuela — well, Venezuela. In the UK, Labour has embraced a startlingly confiscatory policy, advocating for illiberal measures like mass forced divestment. And the free markets capital of the world, Hong Kong, is under literal assault from its murderous and autocratic occupier.

Suffice to say, free markets and strong property rights — the cornerstones of functioning capitalist economies — are under global assault. This is unlikely to reverse. The global underclass, increasingly futile, craves intervention, and will tolerate gross immiseration if it means a reduction in inequality.

And our monetary institutions have surrendered any semblance of reason. Our current age brings us the entertaining if harrowing spectacle of the President of the United States openly warring with the Federal Reserve Chief over the price of money. The stakes: squeezing a little more juice out of our wholly financialized economy in time for a reelection bid. That was all it took to capture the purportedly nonpolitical Federal Reserve. Hedge funds, in a display of breathtaking paperclip-maximization, now spend millions of dollars on machine learning algorithms predicting interest rates from the eyebrow twitches of our monetary high priests as they read the chicken entrails. Money well spent.

At your disposal: the always-on financial machine

Negative interest rates are now orthodoxy at virtually all central banks in developed countries. The IMF openly speculates about how to impose ever-deeper negative rates, including the forced depreciation of _physical cash. _Regardless of whether you believe savers have a divine right to a positive yield, they certainly start to bristle when you propose confiscating their savings. If arbitrarily negative rates are permissible to achieve policy outcomes, at what point do central banks pause for breath and give savers a reprieve? Already in untrammeled territory, it seems unlikely any restraint will materialize this ends-justify-the-means approach to monetary policy.

Savers may not panic at negative 1%, reasoning that the bank is providing a useful service, after all. They may grumble at -3% and start to wonder if their monetary overlords really have it all figured out. At -5% — they pile into gold and start to wonder about that Bitcoin thing.

Because many people fail to appreciate the strength of the system, let’s summarize Bitcoin’s first decade:

- $1 billion has cumulatively been paid in transaction fees

- Miners have cumulatively collected $14 billion in exchange for their services in securing the network

- The average cost basis of all Bitcoin holders is approximately $100 billion

- The market value of all outstanding bitcoins is approximately $190 billion

- The network has settled roughly $2 trillion worth of transactions

- The Bitcoin network now produces 80 exahashes per second (that’s 8 * 10¹⁹ hashes). These hashes cost about $19.8 million dollars a day on highly specialized equipment

You may deride Bitcoin, no matter. Bitcoin will be there for you when you need it. You may not need it now; you may not need it ever. But as we plunge into a more despotic, authoritarian, and chaotic world, you may one day feel comfort knowing that the world’s highest assurance wealth protection system in history is waiting patiently for you.

Until then, it will keep ticking along.