3 Reasons I’m Investing in Bitcoin

| If you find WORDS helpful, Bitcoin donations are unnecessary but appreciated. Our goal is to spread and preserve Bitcoin writings for future generations. Read more. | Make a Donation |

3 Reasons I’m Investing in Bitcoin

By Lyn Alden

Posted July 17, 2020

Blockchain-based cryptocurrencies have been around for over a decade, since the release of Bitcoin in early 2009.

While the asset class has grown considerably, it remains relatively small and highly volatile, so deciding whether to insert a small bit of Bitcoin or other cryptocurrency exposure into a portfolio allocation can be a controversial and confusing decision.

Maybe this article will assist some investors in the decision one way or the other. Bitcoin analysis online can be very polarizing; either written by hardcore bullish enthusiasts or dismissed as a worthless ponzi scheme. As a generalist investor with a value-slant and a global macro emphasis, I’ve sought to bridge the gap a bit by sharing my view of Bitcoin, which is currently bullish.

Although I was aware of Bitcoin as a speculative small asset since around 2011, and knew someone who mined it on her computer back when that was possible (now it requires application-specific integrated circuits, due to heavy competition), I wrote my first article on cryptocurrencies back in November 2017, when the price was in the $6500-$8000 range. During the week or two writing and editing period, the price rose substantially in that big range. My conclusion at the time was neutral-to-bearish, and I didn’t buy any.

Right now, there’s already a lot of optimism backed in; bitcoins and other major cryptocurrencies are extremely expensive compared to their estimated current usage. Investors are assuming that they will achieve widespread adoption and are paying up accordingly. That means investors should apply considerable caution.

-Lyn Alden, November 2017

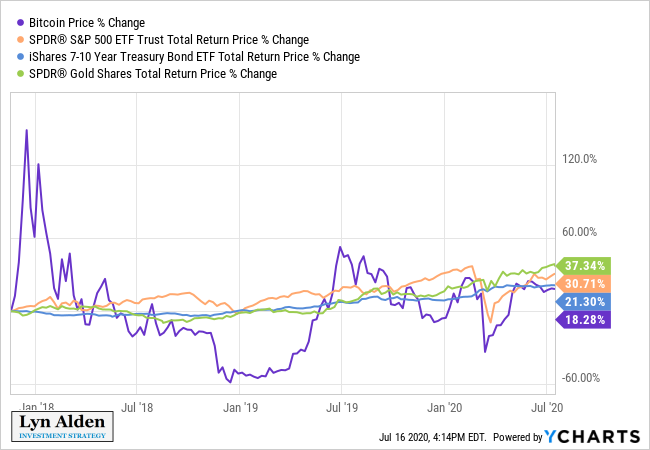

Within the next month or so after the original article, Bitcoin briefly soared to reach $20,000, but then crashed down to below $3,500 a year later, and has since recovered to bounce around in a wide trading range with little or no durable returns.

From the time of my original article nearly two and a half years ago, Bitcoin underperformed the S&P 500, gold, Treasury notes, and a variety of other asset classes, especially on a volatility-adjusted basis:

I’ve updated the article from time to time to refresh data and keep it relevant as changes happen in the industry, but other than keeping an eye on the space from time to time, I mostly ignored it.

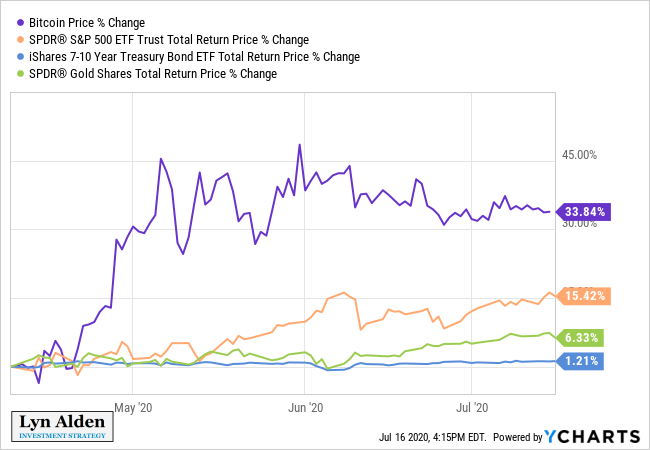

In early 2020, I revisited Bitcoin and became bullish. I recommended it as a small position in my premium research service on April 12th, and bought some bitcoins for myself on April 20th. The price was around $6,900 for that stretch of time. Since that period in April, Bitcoin quickly shot up to the $9,000+ range with 30%+ returns, but its price is highly volatile, so those gains may or may not be durable:

My base case is for Bitcoin to perform very well over the next 2 years, but we’ll see. I like it as a small position within a diversified portfolio, without much concern for periodic corrections, using capital I’m willing to risk.

As someone with an engineering and finance blended background, Bitcoin’s design has always interested me from a theoretical point of view, but it wasn’t until this period in early 2020 that I could put enough catalysts together to build a constructive case for its price action in the years ahead. As a new asset class, Bitcoin took time to build a price history and some sense of the cycles it goes through, and plenty of valuable research has been published over the years to synthesize the data.

So, I’m neither a perma-bull on Bitcoin at any price, or someone that dismisses it outright. As an investor in many asset classes, these are the three main reasons I switched from uninterested to quite bullish on Bitcoin early this year, and remain so today.

Reason 1) Scarcity + Network Effect

Bitcoin is an open source peer-to-peer software monetary system invented by an anonymous person or group named Satoshi Nakamoto that can store and transmit value.

It is decentralized; there is no singular authority that controls it, and instead it uses encryption based on blockchain technology, calculated by multiple parties on the network, to verify transactions and maintain the protocol. Incentives are given by the protocol to those that contribute computing power to verify transactions in the form of newly-“mined” coins, and/or transaction fees. In other words, by verifying and securing the blockchain, you earn some coins.

In the beginning, anyone with a decent computer could mine some coins. Now that many bitcoins have been mined and the market for mining coins has become very competitive, most people acquire coins simply by buying them from existing owners on exchanges and other platforms, while mining new coins is a specialized operation.

Bitcoin’s protocol limits it to 21 million coins in total, which gives it scarcity, and therefore potentially gives it value… if there is demand for it. There is no central authority that can unilaterally change that limit; Satoshi Nakamoto himself couldn’t add more coins to the Bitcoin protocol if he wanted to at this point. These coins are divisible into 100 million units each, like fractions of an ounce of gold.

For context, these “coins” aren’t “stored” on any device. Bitcoin is a distributed public ledger, and owners of Bitcoin can access and transmit their Bitcoin from one digital address to another digital address, as long as they have their private key, which unlocks their encrypted address. Owners store their private keys on devices, or even on paper or engraved in metal.

In fact, a private key can be stored as a seed phrase that can be remembered, and later reconstructed. You could literally commit your seed phrase to memory, destroy all devices that ever had your private key, go across an international border with nothing on your person, and then reconstruct your ability to access your Bitcoin with the memorized seed phrase later that week.

A Digital Monetary Commodity

Satoshi envisioned Bitcoin as basically a rare commodity that has one unique property.

As a thought experiment, imagine there was a base metal as scarce as gold but with the following properties:

– boring grey in colour

– not a good conductor of electricity

– not particularly strong, but not ductile or easily malleable either

– not useful for any practical or ornamental purposeand one special, magical property:

– can be transported over a communications channelIf it somehow acquired any value at all for whatever reason, then anyone wanting to transfer wealth over a long distance could buy some, transmit it, and have the recipient sell it.

-Satoshi Nakamoto, August 2010

So, Bitcoin can be thought of as a rare digital commodity that has unique attributes. Although it has no industrial use, it is scarce, durable, portable, divisible, verifiable, storable, fungible, salable, and recognized across borders, and therefore has the properties of money. Like all “potential” money, though, it needs sustained demand to have value.

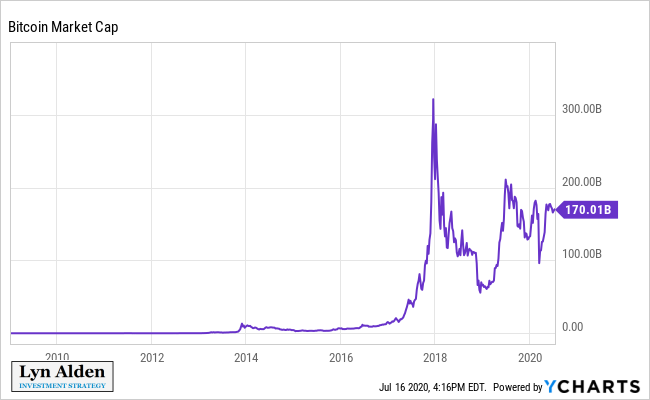

As of this writing, Bitcoin’s market capitalization is about $170 billion, or roughly the value of a large company. The total market capitalization of the entire cryptocurrency asset class is about $270 billion, including Bitcoin as the dominant share. Here’s Bitcoin’s market capitalization chart:

One of my concerns with Bitcoin back in 2017 was that, even if we grant that these digital commodity attributes are useful, and even if we acknowledge that the units of any cryptocurrency are scarce by design, anyone can now create a brand new cryptocurrency. Since Satoshi figured out the mathematical and software methods to create digital scarcity (based in part on previous work by others) and made that knowledge public, and thus solved the hard problems associated with it, any programmer and marketing team can now put together a new cryptocurrency.

There are thousands of them, now that the floodgate of knowledge has been opened. Some of them are optimized for speed. Some of them are optimized for efficiency. Some of them can be used for programmed contracts, and so forth.

So, rather than just one scarce “commodity” that has the unique property of being able to be transported over a network, there are thousands of similar commodities that have that new property. This risks the scarcity aspect of the commodity, and thus risks its value by potentially diluting it and dividing the community among multiple protocols. Each cryptocurrency is scarce, but there is no scarcity to the number of cryptocurrencies that can exist.

This is unlike, say, gold and silver. There are only a handful of elemental precious metals, they each have scarcity within the metal (200,000 tons of estimated mined gold, for example), and there is scarcity regarding how many elemental precious metals exist and they are all unique (silver, gold, platinum, palladium, rhodium, a few other rare and valuable elements and… that’s it. Nature is not making more).

There is a ratio called “Bitcoin dominance” that measures what percentage of the total cryptocurrency market capitalization that Bitcoin has. When Bitcoin was created, it was the only cryptocurrency and thus had 100% market share. Following the rise of Bitcoin, now there are thousands of different cryptocurrencies. First there was a trickle of them, and then it became a flood.

By the end of 2017, during that peak enthusiasm period for cryptocurrencies, Bitcoin’s market share briefly fell below 40%, even though it still remained the largest individual protocol. It has since risen back above 60% market share. Out of thousands of cryptocurrencies, Bitcoin has nearly two thirds of all cryptocurrency market share.

So, what gives individual cryptocurrencies potential value, is their network effect, which in Bitcoin’s case is mainly derived from its first-mover advantage, which led to a security advantage.

An analogy is that a cryptocurrency is like a social network, except instead of being about self-expression, it’s about storing and transmitting value. It’s not hard to set up a new social network website; the code to do it is well understood at this point. Anyone can make one. However, creating the next Facebook (FB) or other billion-user network is a nearly impossible challenge, and a multi-billion-dollar reward awaits any team that somehow pulls it off. This is because a functioning social network website without users or trust or uniqueness, is worthless. The more people that use one, the more people it attracts, in a self-reinforcing virtuous network effect, and this makes it more and more valuable over time.

Similarly, ever since Satoshi solved the hard parts of digital scarcity and published the method for the world to see, it’s easy to make a new cryptocurrency. The nearly impossible part is to make one that is trusted, secure, and with sustained demand, which are all traits that Bitcoin has.

When I analyzed cryptocurrencies in 2017, I was concerned with cryptocurrency market share dilution. Bitcoin’s market share was near its low point, and still falling. What if thousands of cryptocurrencies are created and used, and therefore none of them individually retain much value? Each one is scarce, but the total number of all of them is potentially infinite. Even if just ten protocols take off, that could pose a valuation problem. If the total cryptocurrency market capitalization grows to $1 trillion, but is equally-divided among the top ten protocols for example, then that would be just $100 billion in capitalization for each protocol.

In addition, there were some notable Bitcoin forks at the time, where Bitcoin Cash and subsequently Bitcoin Satoshi Vision were forked protocols of Bitcoin, that in theory could have split the community and market share. Ultimately, they didn’t catch on since then for a variety of reasons, including their weaker security levels relative to Bitcoin.

Gold vs Bitcoin

This reliance on the network effect is not unique to Bitcoin or other cryptocurrencies. Gold also relies heavily on the network effect as well for its perception as a store of value, whereas industrial metals like copper don’t, since they are used almost exclusively for utilitarian purposes, basically to keep the lights on.

Unlike Bitcoin, gold does have non-monetary industrial use, but only about 10% of its demand is industrial. The other 90% is based on bullion and jewelry demand, for which buyers view gold as a store of wealth, or a display of beauty and wealth, because it happens to have very good properties for it in the sense that it looks nice, doesn’t rust, is very rare, holds a lot of value in a small space, is divisible, lasts forever, and so forth. If gold’s demand for jewelry, coinage, and bars were to ever decrease substantially and structurally, leaving its practical industrial usage as its primary demand, the existing supply/demand balance would be thrown out and this would likely result in a much lower price.

In the West, interest in gold bullion has gradually declined somewhat over decades, while demand from the East for storing wealth has been strong. I suspect the 2020’s decade, due to monetary and fiscal policy, could renew western interest in gold, but we’ll see.

So, the argument that Bitcoin isn’t like gold because it can’t be used for anything other than money, doesn’t really hold up. Or more specifically, it’s about 10% true, referring to gold’s 10% industrial demand. With 90% of gold’s demand coming from jewelry and bullion usage, which are based on perception and sentiment and fashion (all for good reason, based on gold’s unique properties), gold would have similar problems to Bitcoin if there was ever a widespread loss of interest in it as a store of value and display of wealth.

Of course, gold’s advantage is that it has thousands of years of international history as money, in addition to its properties that make it suitable for money, so the risk of it losing that perception is low, making it historically an extremely reliable store of value with less upside and less downside risk, but not inherently all that different.

The difference is mainly that Bitcoin is newer and with a smaller market capitalization, with more explosive upside and downside potential. And as the next section explains, a cryptocurrency’s security is tied to its network effect, unlike precious metals.

Cryptocurrency Security is Tied to Adoption

A cryptocurrency’s security is tied to its network effect, and specifically tied to the market capitalization that the cryptocurrency has. If the network is weak, a group with enough computing power could potentially override all other participants on the network, and take control of the blockchain ledger. Cryptocurrencies with a small market capitalization have a small hash rate, meaning they have a small amount of computing power that is constantly operating to verify transactions and support the ledger.

Bitcoin, on the other hand, has so many devices verifying the network that they collectively consume more electricity per year than a small country, like Greece or Switzerland. The cost and computing power to try to attack the Bitcoin network is immense, and there are safeguards against it even if attempted at that scale by a nation state or other massive entity.

Any news story you have ever heard about Bitcoin being hacked or stolen, was not about Bitcoin’s protocol itself, which has never been hacked. Instead, instances of Bitcoin hacks and theft involve perpetrators breaking into systems to steal the private keys that are held there, often with lackluster security systems. If a hacker gets someone’s private keys, they can access that person’s Bitcoin holdings. This risk can be avoided by using robust security practices, such as keeping private keys in cold storage.

The rise of quantum computers could eventually pose an actual security threat to Bitcoin’s encryption, where private keys could be determined from public keys, but there are already known methods that the Bitcoin protocol can adopt when necessary in order to become more quantum resilient, since the blockchain can be updated when there is broad consensus among participants.

Bitcoin’s programmed difficulty for verifying transactions is automatically updated every two weeks, and it seeks the optimal point of profitability and security. In other words, the difficulty of the puzzle to add new blocks to the blockchain is automatically tuned up or down depending on how efficiently miners as a whole are solving those puzzles.

If Bitcoin becomes too unprofitable to mine (meaning the price falls below the cost of hardware and electricity to verify transactions and mine it), then fewer companies will mine it, and the rate of new block creation will lag its intended speed as computational power gradually falls off the network. An automatic difficulty adjustment will occur, making it require less computational power to verify transactions and mine new coins, which reduces security but is necessary to make sure that miners don’t get priced out of maintaining the network.

On the other hand, if Bitcoin becomes extremely profitable to mine (meaning the price is way above the cost of hardware and electricity to mine it), then more people will mine it, and the rate of new block creation will surpass its intended speed as more and more computational power is added to the network. An automatic difficulty adjustment will occur, making it require more computational power to verify transactions and mine new coins, which increases security of the network.

More often than not, the latter occurs, so Bitcoin’s difficulty has gone up exponentially over time, which makes its network more and more secure.

Even if a demonstrably superior cryptocurrency to Bitcoin came around (and some users argue that some of the existing protocols are already superior in many ways, based on speed or efficiency or extra features), that superior cryptocurrency would still find it nearly impossible to catch up with Bitcoin’s security lead in terms of hash rate. Simply by coming later and thus having weaker security due to a weaker network effect, they have an in-built inferiority to Bitcoin on that particular metric, and for a store of value, security is the most important metric. The fact that Bitcoin came first, is something that can’t be replicated unless the community around it somehow stumbles very badly and allows other cryptocurrencies to catch up. The gap, though, is quite wide.

An investment or speculation in a cryptocurrency, especially Bitcoin, is an investment or speculation in that cryptocurrency’s network effect. Its network effect is its ability to retain and grow its user-base and market capitalization, and by extension its ability to secure its transactions against potential attacks.

Bitcoin Strengthening Market Share and Security

Since my 2017 analysis when I was somewhat concerned with market share dilution, Bitcoin has stabilized and strengthened its market share.

The semi-popular forks did not harm it, and thousands of other coins did not continue to dilute it. It has by far the best security and leading adoption of all cryptocurrencies, cementing its role as the digital gold of the cryptocurrency market.

Compared to its 2017 low point of under 40% cryptocurrency market share, Bitcoin is back to over 60% market share.

There is a whole ecosystem built around Bitcoin, including specialist banks that borrow and lend it with interest. Many platforms allow users to trade or speculate in multiple cryptocurrencies, like Coinbase and Kraken, but there is an increasing number of platforms like Cash App and Swan Bitcoin that enable users to buy Bitcoin, but not other cryptocurrencies.

The ongoing stability of Bitcoin’s network effect is one of the reasons I became more optimistic about Bitcoin’s prospects going forward. Rather than quickly fall to upstart competitors like Myspace did to Facebook, Bitcoin has retained substantial market share, and especially hash rate, against thousands of cryptocurrency competitors for a decade now.

Currencies tend to have winner-take-most phenomena. They live or die by their demand and network effects, especially in terms of international recognition. Cryptocurrencies so far appear to be the same, where a few big winners take most of the market share and have most of the security, especially Bitcoin, and most of the other 5,000+ don’t matter. Some of them, of course, may have useful applications outside of primarily being a store of value, but as a store of value in the cryptocurrency space, it’s hard to beat Bitcoin.

During strong Bitcoin bull markets, these other cryptocurrencies may enjoy a speculative bid, briefly pushing Bitcoin back down in market share, but Bitcoin has shown considerable resilience through multiple cycles now.

Through a combination of first-mover advantage and smart design, Bitcoin’s network effect of security and user adoption is very, very hard for other cryptocurrencies to catch up with at this point. Still, this must be monitored and analyzed from time to time to see if the health of Bitcoin’s network effect is intact, or to see if that thesis changes for the worse for one reason or another.

Reason 2) The Halving Cycle

Starting from inception in January 2009, about 50 new bitcoins were produced every 10 minutes from “miners” verifying a new block of transactions on the network. However, the protocol is programmed so that this amount of new coins per block decreases over time, once a certain number of blocks are added to the blockchain.

These events are called “halvings”. The launch period (first cycle) had 50 new bitcoins every 10 minutes. The first halving occurred in November 2012, and from that point on (second cycle), miners only received 25 coins for solving a block. The second halving occurred in July 2016, and from there (third cycle) the reward fell to 12.5 new coins per block. The third halving just occurred in May 2020 (fourth cycle), and so the reward is now just 6.25 coins per new block.

The number of new coins will asymptotically approach 21 million. Every four years or so, the rate of new coin creation gets cut in half, and in the early 2030’s, over 99% of total coins will have been created. The current number that has been mined is already over 18.4 million out of the 21 million that will eventually exist.

Bitcoin has historically performed extremely well during the 12-18 months after launch and after the first two halvings. The reduction in new supply or flow of coins, in the face of constant or growing demand for coins, unsurprisingly tends to push the price up.

Here’s Bitcoin’s historical price chart in logarithmic form, with four red dots indicating the earliest price point close to launch, and the three halvings, which represent the start of the four Bitcoin market cycles so far:

Chart Source: Blockchain.com

Here we see a pretty strong pattern. During the 12-24 months after launch and the subsequent halvings, money flows into the reduced flow of coins, and the price goes up due to this restricted supply. Then after a substantial price increase, momentum speculators get on board, and then other people chase it and cause a mania, which eventually pops and crashes. Bitcoin enters a bear market for a while and then eventually stabilizes around an equilibrium trading range, until the next halving cycle cuts new supply in half again. At that point, if reasonable demand still exists from current and new users, another bull run in price is likely, as incoming money from new buyers flows into a smaller flow of new coins.

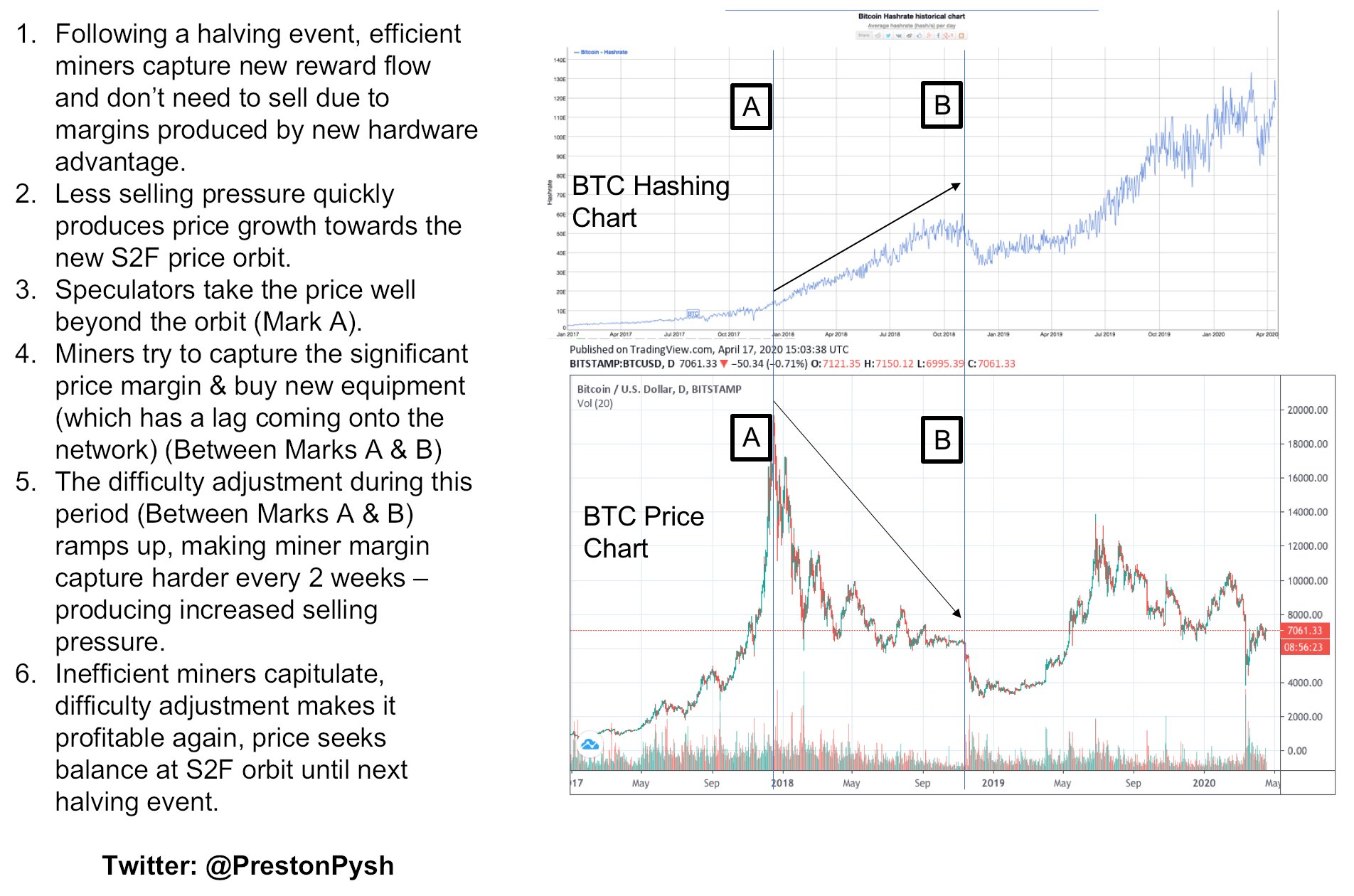

For more detail, Preston Pysh, the co-founder of the Investor’s Podcast Network, put together a chart and narrative that describes his view of the halving cycle from the perspective of the miners:

Chart Source: @PrestonPysh

Based on recent hash rate data, it appears the mining market may have gotten past the post-halving capitulation period (from May into July), and now is looking pretty healthy. Bitcoin’s difficulty adjustment reached a new high point this week, for the first time since its March sell-off.

Stock-to-Flow Model

Monetary commodities have high stock-to-flow ratios, which refers to the ratio between the amount of that commodity that is stored (aka “the stock”) and the amount of that commodity that is newly-produced each year (aka “the flow”).

Base commodities like oil and copper have very low stock-to-flow ratios. Since they have a large volume relative to price, they are costly to store and transport, so only a handful of months of supply are stored at any one time.

Monetary commodities like silver and gold have high stock-to-flow ratios. Silver’s ratio is over 20 or 30, and gold’s ratio is over 50 or 60. Specifically, the World Gold Council estimates that 200,000 tons of gold exists above ground, and annual new supply is roughly 3,000 tons, which puts the stock-to-flow ratio somewhere in the mid-60’s as a back-of-the-envelope calculation. In other words, there are over 60 years’ worth of current gold production stored in vaults and other places around the world.

As Bitcoin’s existing stock has increased over time, and as its rate of new coin production decreases after each halving period, its stock-to-flow ratio keeps increasing. In the current halving cycle, about 330,000 new coins are created per year, with 18.4 million coins in existence, meaning it currently has a stock-to-flow ratio in the upper 50’s, which puts it near gold’s stock-to-flow ratio. In 2024, after the fourth halving, Bitcoin’s stock-to-flow ratio will be over 100.

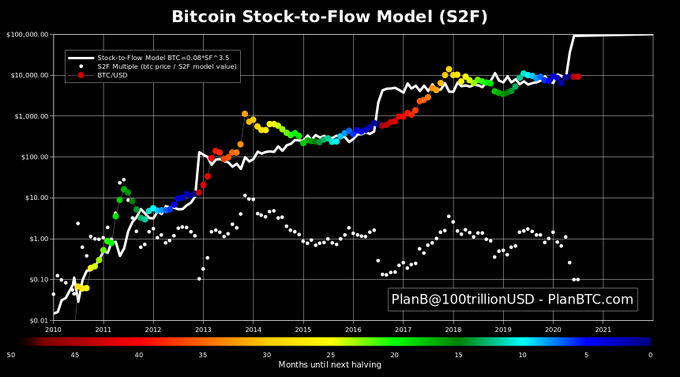

In 2019, a popular Bitcoin price model based on its stock-to-flow ratio was published by PlanB, a Dutch institutional investor. He has several versions of it, and multiple visualizations to display it, but here’s one of the representations:

Chart Source: PlanB, @100trillionUSD

The model backtests Bitcoin and compares its price history to its changing stock-to-flow ratio over time, and in turn develops a price model which it can then (potentially) be extrapolated into the future. He also has created other versions that look at the stock-to-flow ratios of gold and silver, and apply that math to Bitcoin to build a cross-asset model.

The white line in the chart above represents the price model over time, with the notable vertical moves being the three halvings that occurred. The colored dots are the actual price of Bitcoin during that timeframe, with colors changing compared to their number of months until the next halving. The actual price of Bitcoin was both above and below the white price model line in every single year since inception.

As you can see, the previously-described pattern appears. In the year or two after a halving, the price tends to enjoy a bull run, sharply overshoots the model, and then falls below the model, and then rebounds and finds equilibrium closer to the model until the next halving.

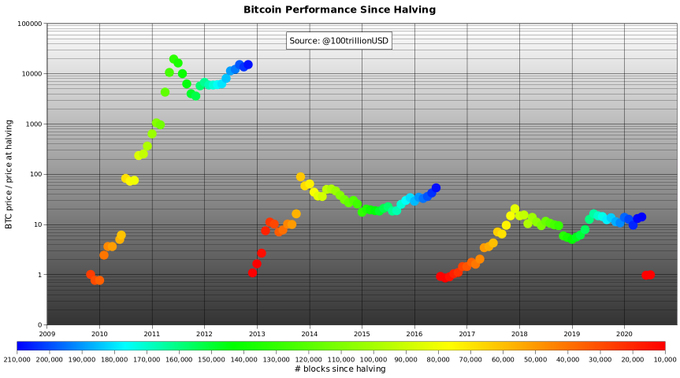

Here’s his breakdown of each halving cycle, including the launch cycle, which makes it even more clear:

Chart Source: PlanB, @100trillionUSD

Each halving cycle is less explosive than the previous one, as the size of the protocol grows in market capitalization and asset class maturity, but each cycle still goes up dramatically.

PlanB’s model extrapolation is very bullish, suggesting a six figure price level within the next 18 months in this fourth cycle, and potentially far higher in the fifth cycle. A six figure price compared to the current $9,000+ price range, is well over a tenfold increase. Will that happen? I have no idea. That’s more bullish than my base case but it’s nonetheless a useful model to see what happened in the past.

If Bitcoin reaches a six figure price level with 19 million coins in total, that would put its market cap at just under $2 trillion or more, above the largest mega-cap companies in the world today. It would, however, still be a small fraction of 1% of global net worth, and about a fifth of gold’s estimated market capitalization (roughly $10 trillion, back-of-the-envelope), so it’s not unfathomable for Bitcoin to eventually reach that height if there is enough sustained demand for it. During the late-2017 cryptocurrency mania, the total market capitalization of the cryptocurrency space reached over $800 billion, although as previously mentioned, Bitcoin’s share of that briefly fell to under 40% of the asset class, so it peaked at just over $300 billion.

While the PlanB model is accurate regarding what the price of Bitcoin did relative to its historical stock-to-flow ratio, the extent to which it will continue to follow that model is an open question. During the first decade of Bitcoin’s existence, it went from a micro-cap asset with virtually no demand, to a relatively large asset with significant niche demand, including from some institutional investors. On a percent-growth basis, the demand increase has been unbelievably fast, but is slowing.

When something becomes successful, the law of large numbers starts to kick in. It takes a small amount of money to move the needle on a small investment, but a lot of money to move the needle on a big investment. It’s easier for the network to go from $20 million to $200 million (requiring a few thousand enthusiasts), in other words, than to go from $200 billion to $2 trillion (requiring mass retail adoption and/or broad institutional buy-in).

The unknown variable for how well Bitcoin will follow such a model over this halving cycle, is the demand side. The supply of Bitcoin, including the future supply at a given date, is known due to how the protocol operates. This model’s historical period involves a very fast-growing demand for Bitcoin on a percent gain basis, going from nearly no demand to international niche demand with some initial institutional interest as well.

The launch cycle had a massive gain in percent terms from virtually zero to over $20 per Bitcoin at its peak. The second cycle, from peak-to-peak, had an increase of over 50x, where Bitcoin first reached over $1,000. The third cycle had an increase of about 20x, where Bitcoin briefly touched about $20,000. I think looking at the 2-5x range for the next peak relative to the previous cycle high makes sense here for the fourth cycle.

If demand grows more slowly in percent terms than it has in the past, the price is likely to undershoot PlanB’s historical model’s projections in the years ahead, even if it follows the same general shape. That would be my base case: bullish with an increase to new all-time highs from current levels within two years, but not necessarily a 10x increase within two years. On the other hand, we can’t rule out the bullish moonshot case if demand grows sharply and/or if some global macro currency event adds another catalyst.

All of this is just a model. I have a moderately high conviction that the general shape of the price action will play out again in this fourth cycle in line with the historical pattern, but the magnitude of that cycle is an open guess.

Game Theory

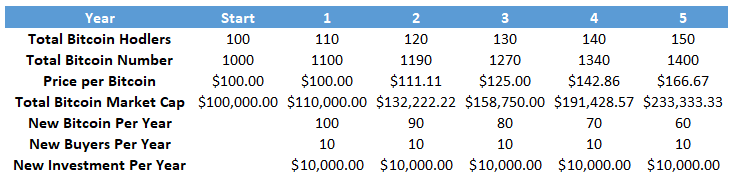

Let’s put away real numbers for a second, and assume a simple thought experiment, with made-up numbers for clarity of example.

Suppose Bitcoin has been around for a while after a period of explosive demand. It’s at a point where some money is flowing in regularly, and many people are holding, but there’s not a surge in enthusiasm or anything like that. Just a constant low-key influx of new capital. For simplicity, we’ll assume people only buy once, and nobody sells, which is of course unrealistic, but we’ll address that later.

In this example, the starting state is 100 holders of Bitcoin, with 1000 coins in existence between them (an average of 10 coins each), at a current price point of $100 per coin, resulting in a total market capitalization of $100,000.

Each year for the next five years, ten new people each want to put $1,000 into Bitcoin, totaling $10,000 in annual incoming capital, for one reason or another.

However, there is a shrinking number of new coin supply per year (and nobody is selling existing coins other than the miners that produce them). In the first year, 100 new coins are available for resale. In the second year, only 90 new coins are available. In the third year, only 80 new coins are available, and so forth. That’s our hypothetical new supply reduction for this thought experiment.

During the first year, the price doesn’t change; the ten new buyers with $10,000 in total new capital can easily buy the 100 new coins (10 coins each), and the price per coin remains $100.

During the second year, with only 90 new coins and still $10,000 in new capital that wants to come in, each buyer can only get 9 coins, at an effective price point of $111.11 per coin.

During the third year, with only 80 new coins and still $10,000 in new capital, each buyer can only get 8 coins, at an effective price point of $125 per coin.

By the fourth year with 70 new coins, that’s $142.86 per coin. By the fifth year with 60 new coins, that’s $166.67 per coin. The number of coins has increased by 40% during this five-year period, so the market capitalization also grew pretty substantially (over 130%), because both the number of coins and the per-coin price increased.

Some of those premises are of course unrealistic, and are simply used to show what happens when there is a growing user-base and constant low-key source of new buyers against a shrinking flow of new coins available.

In reality, a growing price tend to cause more demand, and vice versa. When investors see a bull market in Bitcoin, the demand increases dramatically, and when investors see a bear market in Bitcoin, the demand decreases. In addition, not all of the existing Bitcoin stock is permanently held; plenty of it is traded and sold.

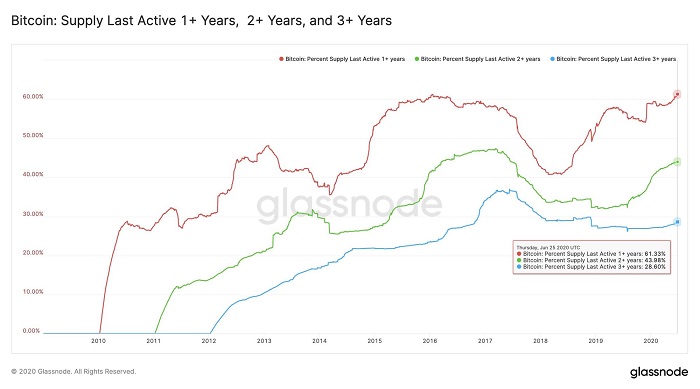

However, Glassnode has plenty of research and data regarding how long people hold their Bitcoin.

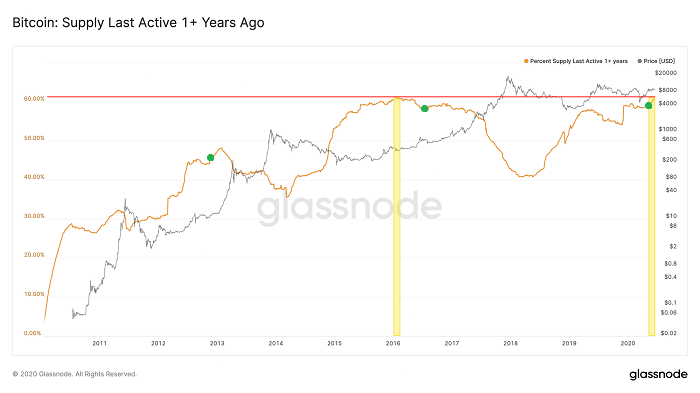

For example, they published a chart within the past few weeks that showed that over 60% of Bitcoin supply hasn’t changed addresses in the past year or more, and over 40% hasn’t moved in the past two years or more:

Chart Source: Glassnode

That’s not a perfect metric because an existing user can shift their Bitcoin from one address to another, firms that hold custody of Bitcoin for others can complicate the issue, and some percentage of early-mined Bitcoin are most likely lost due to people losing their private keys. However, it does provide useful data nonetheless.

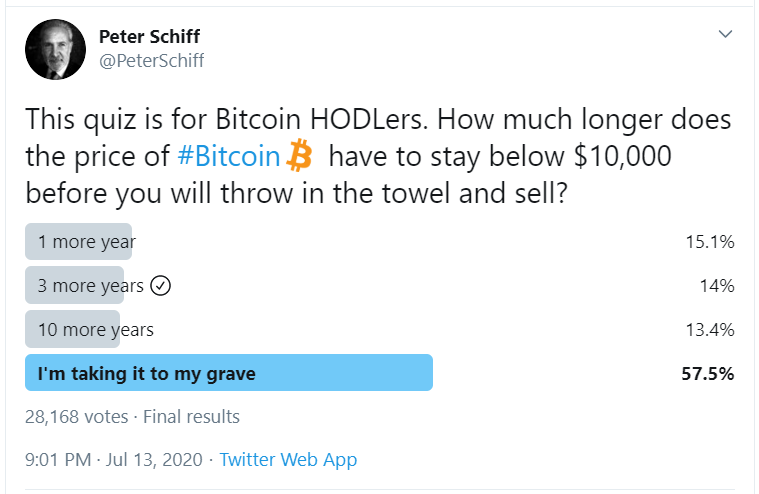

Well-known gold bull and Bitcoin bear Peter Schiff recently performed a poll among his followers with a large 28,000+ sample, and found that about 85% of people who buy-and-hold Bitcoin and that answered his poll (which we must grant is a biased sample, although I’m not sure to which bias) are willing to hold for 3 years or more even if the price remains below $10,000 that whole time.

I’m not trying to criticize or praise Peter Schiff here; just highlighting a recent sentiment sampling.

The simple thought experiment above merely captures the mathematical premise behind a stock-to-flow argument. As long as there is a mildly growing user-base of holders, and some consistent level of new demand in the face of less new supply, a reduction in new supply flow naturally leads to bullish outcomes on the price. It would take a drop-off in new or existing demand for it to be otherwise.

The additional fact that the new supply of Bitcoin gets cut in half roughly every four years rather than reduced by a smaller fixed amount each year like in the simplistic model, represents pretty smart game theory inherent in Bitcoin’s design. This approach, in my view, gave the protocol the best possible chance for successfully growing market capitalization and user adoption, for which it has thus far been wildly successful.

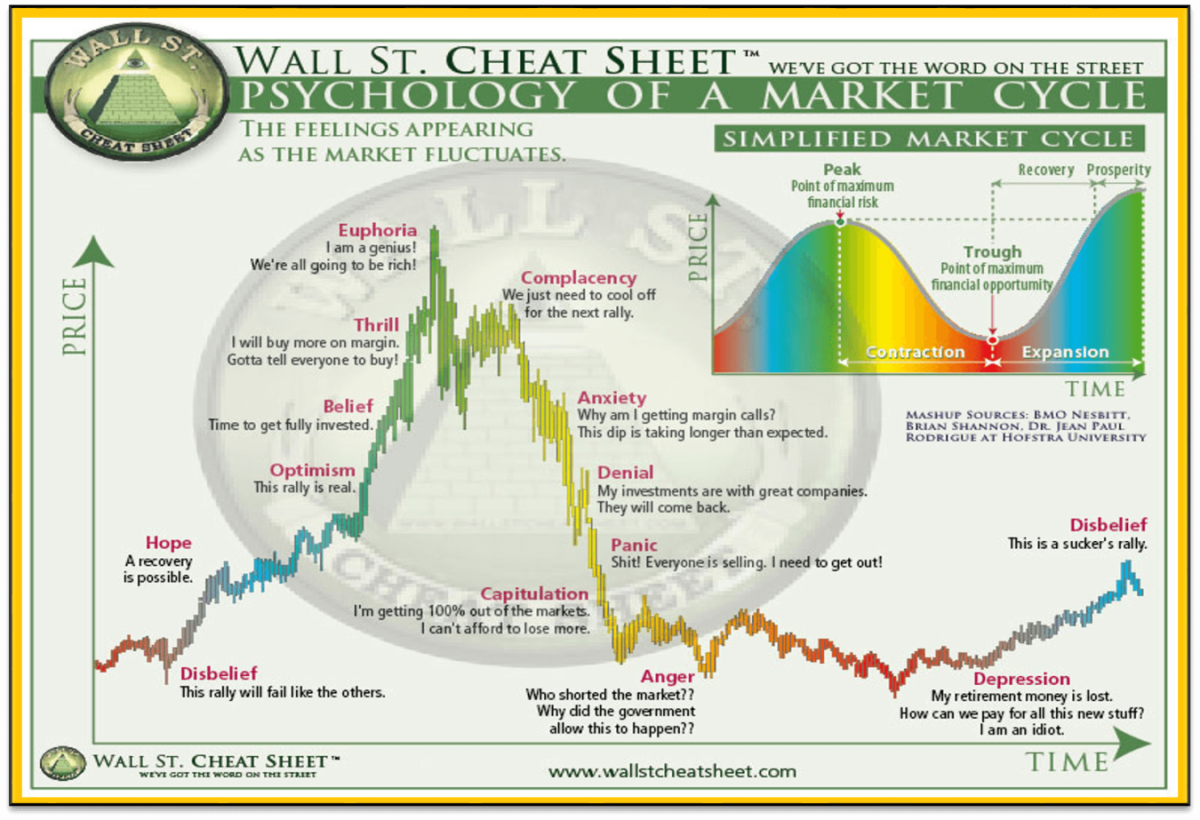

Basically, Bitcoin has a built-in 4-year bull/bear market cycle, not too much different than the stock market cycle. And these 4 years give investors plenty of time to experience the mania and despair associated with a cycle like this, which would be hard to replicate in 1-year cycles because it would all happen too quickly:

Chart Source: Wall St. Cheat Sheet

Bitcoin tends to have these occasional multi-year bear markets during the second half of each cycle, and that cuts away the speculative froth and lets Bitcoin bears pile on, pointing out that the asset hasn’t made a new high for years, and then the reduction in new supply sets the stage for the next bull-run. It then brings in new users with each cycle.

For one more Glassnode visual, here is their recent chart that compares Bitcoin’s price (gray line) to the percent of Bitcoin supply that hasn’t changed addresses in at least a year (orange line). I added green dots to indicate halvings:

Chart Source: Glassnode

Here we see a consistent trend. During the Bitcoin price spikes associated with each cycle, people trade frequently and therefore the percentage of long-term holders diminishes. During Bitcoin consolidation periods that lead into the halvings, the percent of Bitcoin supply that is inactive, starts to grow. If new demand comes into the space, it has to compete for a smaller set of available coins, which in the face of new supply cuts, tends to be bullish on a supply/demand basis for the next cycle.

And although these halving-cycle relationships are more well known among Bitcoin investors over the past year, partly thanks to PlanB’s published research, Bitcoin remains a very inefficient market. There’s lots of retail activity, institutions aren’t leading the way, and relatively few people with big money ever sit down and try to really understand the nuances of the protocol or what makes one cryptocurrency different than another cryptocurrency. Each time Bitcoin reaches a new order of magnitude for market capitalization, though, it captures another set of eyes due to increased liquidity and price history.

Bitcoin Priced in Gold

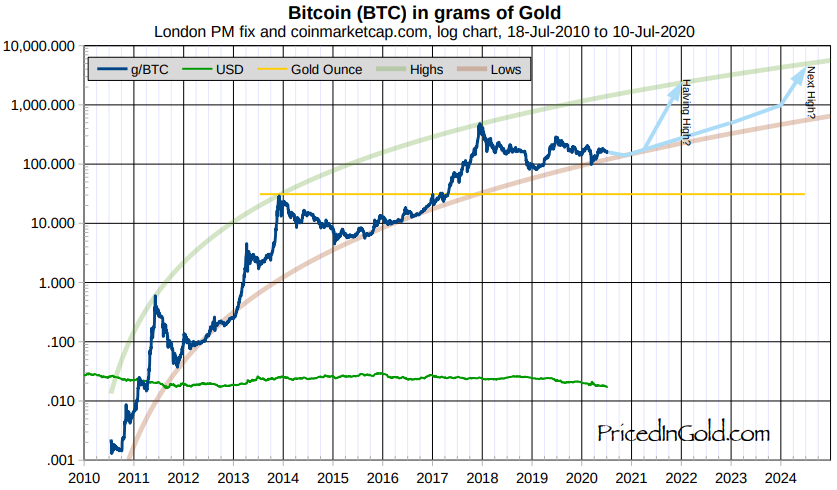

We can remove the dollar and various models from the price equation, and just look at Bitcoin priced in another scarce asset: grams of gold.

Chart Source: Charles Vollum, PricedinGold.com

Charles Vollum’s chart suggests a more than 10x increase in the years ahead if it bounces back to the top end of its historical range, which would imply a six figure dollar price (like PlanB’s model) if gold remains relatively static in dollar terms. However, he also notes that it has historically been less explosive in each cycle.

My analysis starts by noticing the relative heights and timings of the highs in mid-2011, late-2013 and late 2017. The second peak is about 48 times higher than the first, while the third peak is about 17x the second. So the rate of growth in the peaks seems to be slowing.

-Charles Vollum

If the next Bitcoin-priced-in-gold peak is 5x higher than the previous peak, as a random example that continues the diminishing pattern, that would be well into the six figures in dollar terms, assuming gold holds its value over the next few years. After the mania period with this model, it could drop back down into the five figure dollar price range for a while until the next cycle. This is all speculative, but worthy of note for folks that notice patterns.

Volatility Reduction Over Time

Charles Vollum also noticed the decline in volatility over Bitcoin’s existence, again as priced in gold (but it also applies roughly to dollars):

Next, notice the distance between the red and green lines for any given date. In 2011, the upper bound was about 84x the lower bound. A year later, the ratio was 47x. By 2015 it was 22x, and at the start of 2020 it had fallen to 12x. This is a good thing, demonstrating a decline in overall peak-to-trough volatility. If this pattern holds up, the ratio will be about 9x in mid 2024, and about 6.5x by the end of the decade. Still high by forex and bond standards, but less than 10% of the 2011 volatility!

-Charles Vollum

Since Bitcoin started from a tiny base and grew into a meaningful size, in my view its volatility has been a feature, rather than a bug. In some years, it has been down over 80%, while in other years, it has gone up over 1,000%. This feature makes it speculative for most people, rather than having a reputation as a reliable store of value that gold enjoys, since it’s relatively uncommon for gold to have a double-digit percent drawdown year, let alone a double-digit percent drawdown day like Bitcoin sometimes has.

If, over the next 5+ years, Bitcoin’s market capitalization becomes larger and more widely-held, its notable volatility can decrease, like a small-cap growth company emerging into a large-cap blue-chip company.

In the meantime, Bitcoin’s volatility can be managed by using appropriate position sizes relative to an investor’s level of knowledge and conviction in the asset, and relative to their personal financial situation and specific investment goals.

Bitcoin’s volatility is not for the feint of heart, but then again, a 2% portfolio position in something is rarely worth losing sleep over even if it gets cut in half, and yet can still provide meaningful returns if it goes up, say, 3-5x or more.

Intentional Design

Whether it ultimately succeeds or fails, Bitcoin is a beautifully-constructed protocol. Genius is apparent in its design to most people who study it in depth, in terms of the way it blends math, computer science, cyber security, monetary economics, and game theory.

Rather than just a fixed set of coins released to the public, or a fixed perpetual rate of new supply, or any other possible permutation that Satoshi could have designed, this is the specific method he chose to initiate, which is now self-perpetuating. Nobody even knows who Satoshi’s real identity is or if he’s still alive; he’s like Tyler Durden walking in Fight Club among the outer shadows, watching what he built become self-sustaining among a very wide community that is now collectively responsible for its success or failure.

The regular halving events consistently reduce the flow of new coins, meaning that as long as there is a persistent user-base that likes to hold a lot of the existing coins, even if the annual new interest in Bitcoin from new buyers remains just constant (rather than growing), Bitcoin’s price is likely to rise in value over the course of a halving cycle. This in turns attracts more attention, and entices new buyers during the cycle.

The thought put into its architecture likely played a strong role for why Bitcoin reached relatively wide adoption and achieved a twelve-figure market capitalization, rather than come and go as a novel thing that a few cypherpunk programmers found fascinating. For it to fail, Bitcoin’s user-base would need to stagnate, go sideways, and ultimately go down in a sustained fashion for quite a while. Its death has been prematurely described or greatly exaggerated on many occasions, and yet here it is, chugging along and still growing, over 11 years into its existence, most likely thanks in part to the halving cycles in addition to its first-mover advantage that helped it build the most computational security.

In other words, in addition to solving the challenging technical problems associated with digital scarcity and creating the first cryptocurrency, Satoshi also chose a smart set of timing and quantity numbers (out of a nearly infinite set that he could have chosen from, if not carefully thought out) to maximize the incentive structure and game theory associated with his new protocol. Or, he was brilliantly lucky with his choices.

There are arguments for how it can change, like competitor protocols that use proof-of-stake rather than proof-of-work to verify transactions, or the adoption of encryption improvements to make it more quantum-resilient, but ultimately the network effect and price action will dictate which cryptocurrencies win out. So far, that’s Bitcoin. It’s not nearly the fastest cryptocurrency, it’s not nearly the most energy-efficient cryptocurrency, and it’s not the most feature-heavy cryptocurrency, but it’s the most secure and the most trusted cryptocurrency with the widest network effect and first-mover advantage.

How Bitcoin behaves over the next two years, compared to its performance after previous halvings, is a pretty big test for its third halving and fourth overall cycle. We’ll see if it stalls here and breaks down vs the historical pattern, or keeps pushing higher and wider as it has in the previous three cycles.

I don’t have the answer, but my base outlook is bullish, with several catalysts in its favor and no firm catalyst as to why this cycle should be different than the prior cycles in terms of general direction and shape, even if I wouldn’t really try to guess the magnitude.

Reason 3) An Ideal Macro Backdrop

In Satoshi’s genesis block for Bitcoin that initiated the blockchain, he put in a news headline from that week:

The Times 03/Jan/2009 Chancellor on brink of second bailout for banks

-Bitcoin Genesis Block

Bitcoin was conceived and launched during 2008 and 2009; the heart of the global financial crisis, with widespread bank failure, large government bailouts, and international adoption of quantitative easing as a policy tool by central banks. His protocol was an attempt to store and transmit value in a way that was both verifiable and scarce, like a digital gold in contrast to the idea of bailouts and money-printing.

That crisis took years to play out. U.S. deficits were elevated for over 5 years, and quantitative easing didn’t end until late 2014. Europe experienced a delayed sovereign debt crisis in 2012. That whole financial crisis was a process, rather than an event.

Over a decade later, we have an even larger crisis on our hands, with larger bailouts, bigger quantitative easing, and direct cash handouts to companies and consumers which are paid for by central bank deficit monetization.

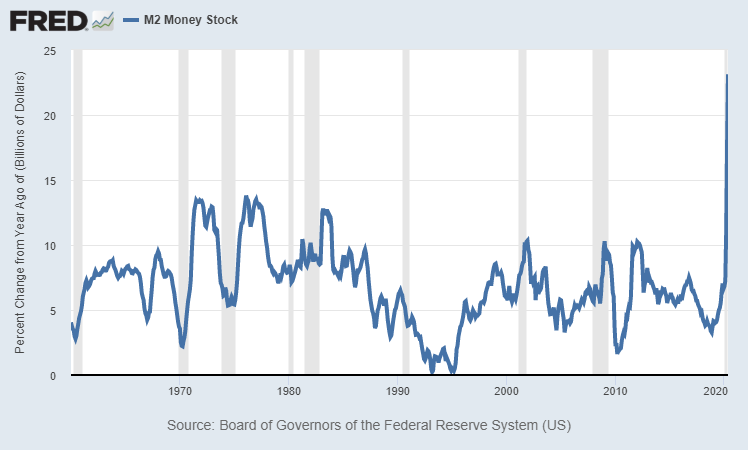

The broad money supply in the United States, for example, has gone up massively. Here is the year-over-year percent change rate:

Chart Source: St. Louis Fed

The U.S. federal government is set to run a deficit somewhere in the ballpark of 20% of GDP this year, depending on the size of their next fiscal injection, which is by far the largest deficit since World War II. And most of this deficit is being monetized by the Federal Reserve, by creating money to buy Treasuries from primary dealers and elsewhere on the secondary market, to ensure that this explosive supply of Treasuries does not overwhelm actual demand.

The dichotomy between quantitative easing that central banks around the world are doing, and the quantitative tightening that Bitcoin just experienced with its third halving, makes for a great snapshot of the difference between scarcity or the lack thereof. Dollars, euro, yen, and other fiat currencies are in limitless abundance and their supply is growing quickly, while things like gold and silver and Bitcoin are inherently scarce.

This is an era of near-zero interest rates, even negative nominal interest rates in some cases, and vast money-printing. Key interest rates and sovereign bond yields throughout the developed world are below their central banks’ inflation targets. The fast creation of currency has demonstrably found its way into asset prices. Stock prices, bond prices, gold prices, and real estate prices, have all been pushed up over the past 25 years.

Even a 1% spillover into Bitcoin from the tens of trillions’ worth of zero-yielding bonds and cash assets, if it were to occur, would be far larger than Bitcoin’s entire current market capitalization.

I have several articles describing the money-printing and currency devaluation that is likely to occur throughout the 2020’s decade:

- The Subtle Risks of Treasury Bonds

- “Fixing” the Debt Problem

- QE, MMT, and Inflation/Deflation: A Primer

- Why This is Unlike the Great Depression

In early May 2020, Paul Tudor Jones became publicly bullish and went long Bitcoin, describing it as a hedge against money-printing and inflation. He drew comparisons between Bitcoin in the 2020’s and gold in the early 1970’s.

Smaller hedge funds have already been dabbling in Bitcoin, and Tudor Jones may be the largest investor to date to get into it. There are now firms that have services directed at getting institutional investors on board with Bitcoin, whether they be hedge funds, pensions, family offices, or RIA Firms, by providing them the enterprise-grade security and execution they need, in an asset class that has historically been focused mainly on retail adoption. Even an asset manager as large as Fidelity now has a group dedicated to providing institutional cryptocurrency solutions.

And speaking of retail, the onboarding platforms for Bitcoin are getting easier to use. When I first looked at Bitcoin in 2011, and then again in 2017, and then again in early 2020, it was like a new era each time in terms of the usability and depth of the surrounding ecosystem.

Some major businesses are already on board, apart from the ones that grew from crypto-origins like Coinbase. Square’s (SQ) Cash App enables the purchase of Bitcoin, for example. Robinhood, which has enjoyed an influx of millions of new users this year, has built-in cryptocurrency trading, making an easy transition for Robinhood users if they happen to shift bullishness from stocks to cryptos. Paypal/Venmo (PYPL) might roll it out one day as well.

So, if Bitcoin’s halving cycle, or the fiscal/monetary policy backdrop, lead to bull market in Bitcoin within the next couple years, there are plenty of access points for retail and institutional investors to chase that momentum, potentially leading to the same explosive price outcome that the previous three halving cycles had. Again, I’m not saying that’s a certainty, because ultimately it comes down to how much demand there is, but I certainly think it’s a significant possibility.

Final Thoughts

At the current time, I view Bitcoin as an asymmetric bet for a small part of a diversified portfolio, based on a) Bitcoin’s demonstrated network effect and security, b) where we are in Bitcoin’s programmed halving cycle, and c) the unusual macro backdrop that favors Bitcoin as a potential hedge.

If a few percentage points of a portfolio are allocated to it, there is a limited risk of loss. If Bitcoin’s price gets cut in half or somehow loses its value entirely over the next two years, and this fourth cycle fails to launch and totally breaks down and completely diverges from the three previous launch/halving cycles, then the bet for this period will have been a dud. On the other hand, it’s not out of the question for Bitcoin to triple, quadruple, or have a potential moonshot price action from current levels over that period if it plays out anything remotely like the previous three launch/halving cycles.

What will happen in this cycle? I don’t know. But the more I study the way the protocol works, and by observing the ecosystem around it over the years, I am increasingly bullish on it as a calculated speculation with a two-year viewpoint for now, and potentially for much longer than that.

Additional Note: Ways to Buy Bitcoin

Some people have asked me what I think the best places to buy Bitcoin are, so I’m adding this last section.

Plenty of people have strong feelings about where to buy it or what companies they want to do business with; ultimately it comes down to your country of residence, how much you want to buy, how hands-on you want to be with it, and whether you want to accumulate it or trade it. There are trade-offs for convenience, security, and fees for various choices.

Exchanges like Kraken and Binance and Coinbase are popular entry points for people into buying some Bitcoin, especially if they want to trade it. Do your homework, and find one that meets your criteria that operates in your jurisdiction.

I think Swan Bitcoin is great for accumulating Bitcoin, especially if you want to dollar-cost average into it, and I use it myself. I have a referral code as well: folks that sign up at swanbitcoin.com/alden/ can earn $10 in free Bitcoin if they start accumulating through that platform. It can be stored for free with their custodian, or automatically transferred to your wallet. For many people, this is the method I would personally recommend checking out.

The Grayscale Bitcoin Trust (GBTC) is a publicly-traded trust that holds Bitcoin, and is therefore a hands-off method that can be purchased through an existing brokerage account. It has some disadvantages, like relatively high fees, a tendency to trade for a sizable premium over NAV, and centralized custody, but it’s one of the few options available for investors if they want to hold a small allocation to Bitcoin within a tax-advantaged account.

Ultimately, it comes down individual needs. In general, if you want to minimize fees and maximize security for a large Bitcoin purchase, then maintaining your own Bitcoin wallet and private keys is the rock-solid way to go, but has a learning curve. If you want to just buy a bit and maintain some exposure and maybe trade it a bit, some of the exchanges are a good way to get into it. For folks that want to have some long-term exposure to it, Swan Bitcoin is a great place to start.