WORDS is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

WORDS is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

Donate & Download the January 2020 Journal PDF

Remember, if you see something, say something. Send us your favorite Bitcoin commentary.

Bitcoin’s increasing price resistance uphill, short- and long-term

By Harold Christopher Burger

Posted December 30, 2019

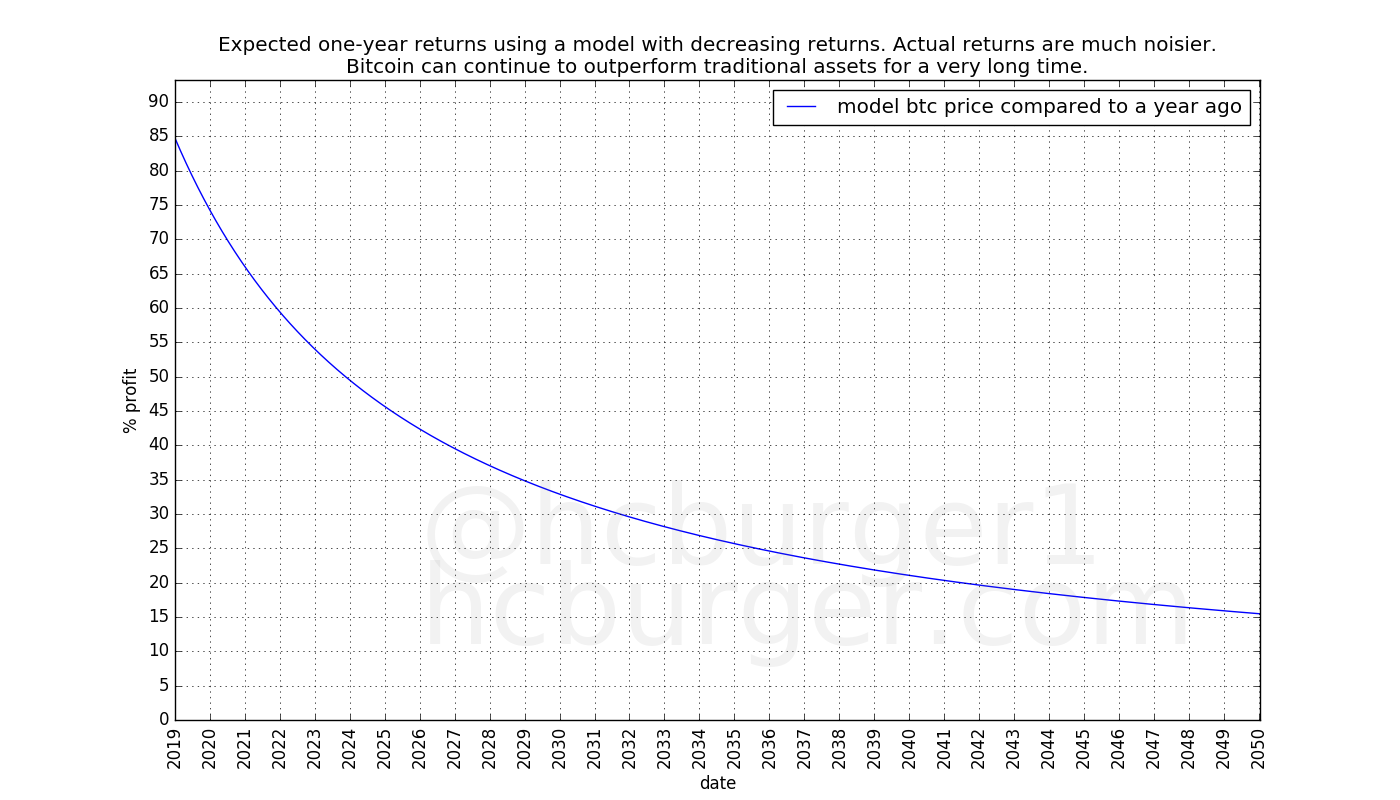

What can we say about bitcoin’s future price? In “Bitcoin’s natural long-term power-law corridor of growth” I have proposed a mathematical model for bitcoin’s price evolution which uses a simple equation using only time as an input variable. This article will not use a precise mathematical model. Rather, we will make a number of empirical observations regarding bitcoin’s price evolution. Two main observations are made:

- The case for the fact that bitcoin’s price returns are diminishing over time (i.e. price growth is slowing) is strengthened.

- Bitcoin’s shorter-term price movements are becoming tamer over time: Fluctuations are becoming less extreme in the short-term.

These two points can be explained by the fact that it takes more and more capital to increase the price of bitcoin, and that it becomes more and more difficult to find more capital. Moving the price of bitcoin from $0.1 to $1 was possible with relatively few dollars. Moving the price of bitcoin from $1000 to $10000 required much more capital. This effect slows the potential growth of bitcoin in both the long- and short-term.

The price of bitcoin is facing more and more resistance on its path upwards. To a lesser extent, the same is true for downward price movements.

Investors should expect lower long-term gains than in the past, but also tamer and slower bull markets. Overall, bitcoin’s price volatility indeed seems to decrease with time. Price growth here should be understood as being in percentage terms.

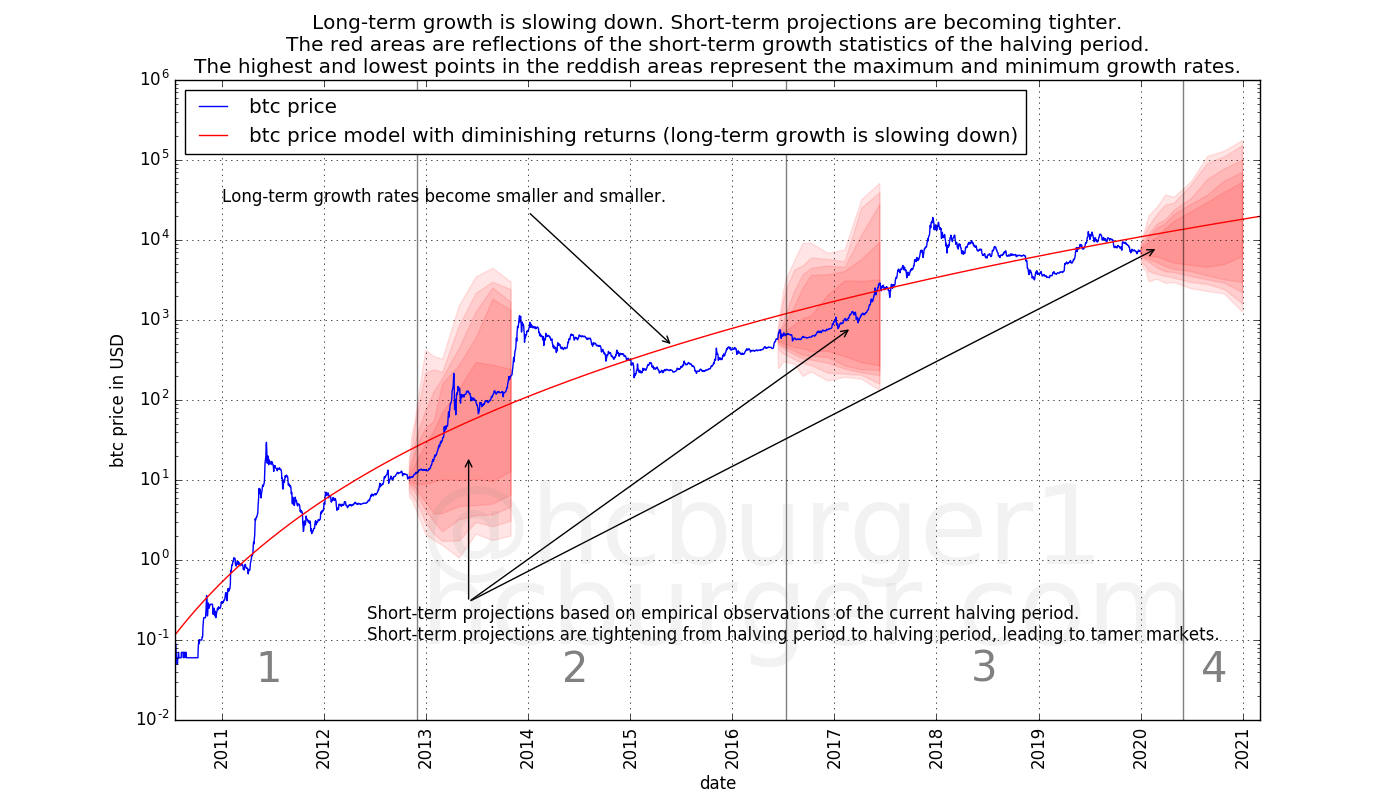

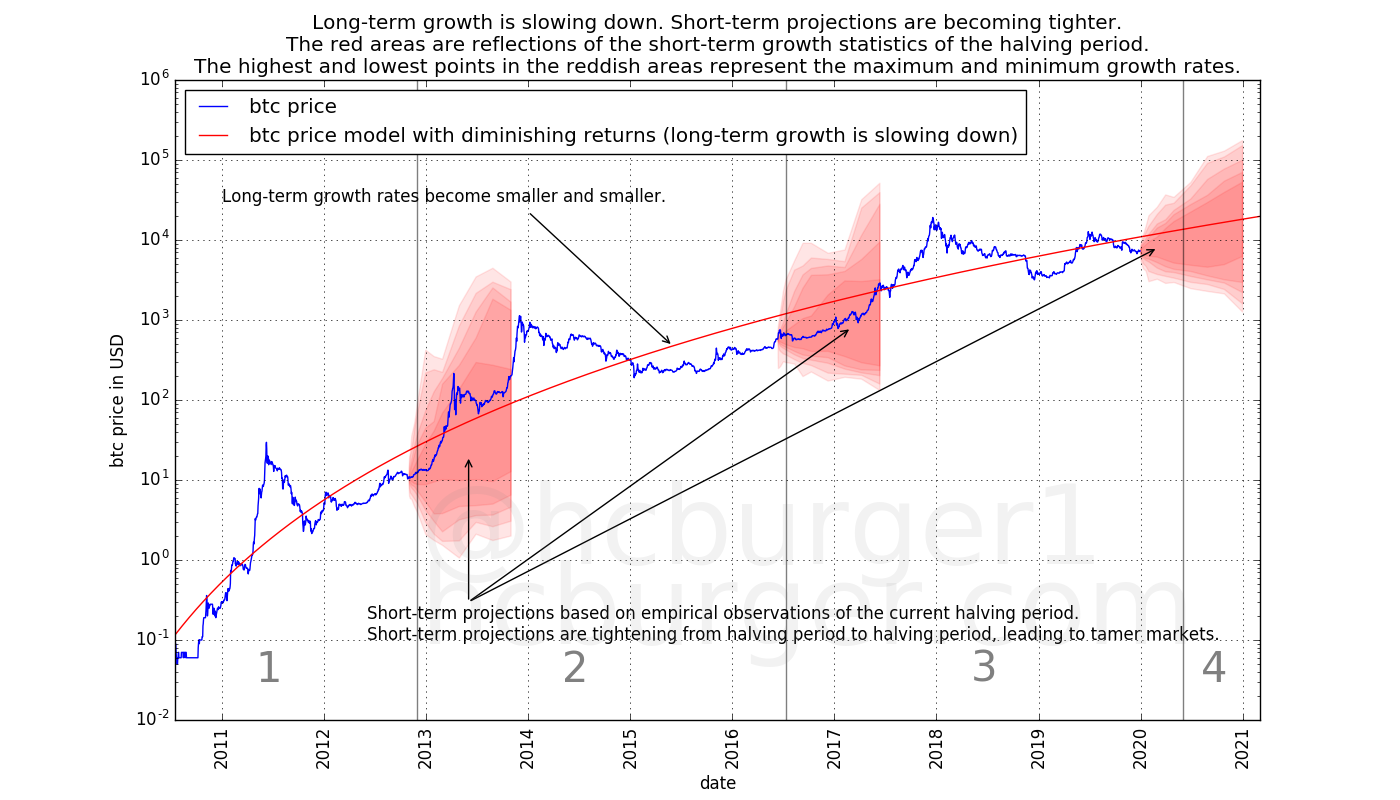

The red zones are reflections of the statistics of short-term growth rates observed within the halving period. The highest and lowest points in the reddish areas represent the maximum and minimum growth rates observed. The maximum and minimum growth rates are estimated over several hodling periods, represented horizontally. Darker areas indicate percentiles. The exact process is described further below in this article.

The red zones are reflections of the statistics of short-term growth rates observed within the halving period. The highest and lowest points in the reddish areas represent the maximum and minimum growth rates observed. The maximum and minimum growth rates are estimated over several hodling periods, represented horizontally. Darker areas indicate percentiles. The exact process is described further below in this article.

Diminishing or non-diminishing returns?

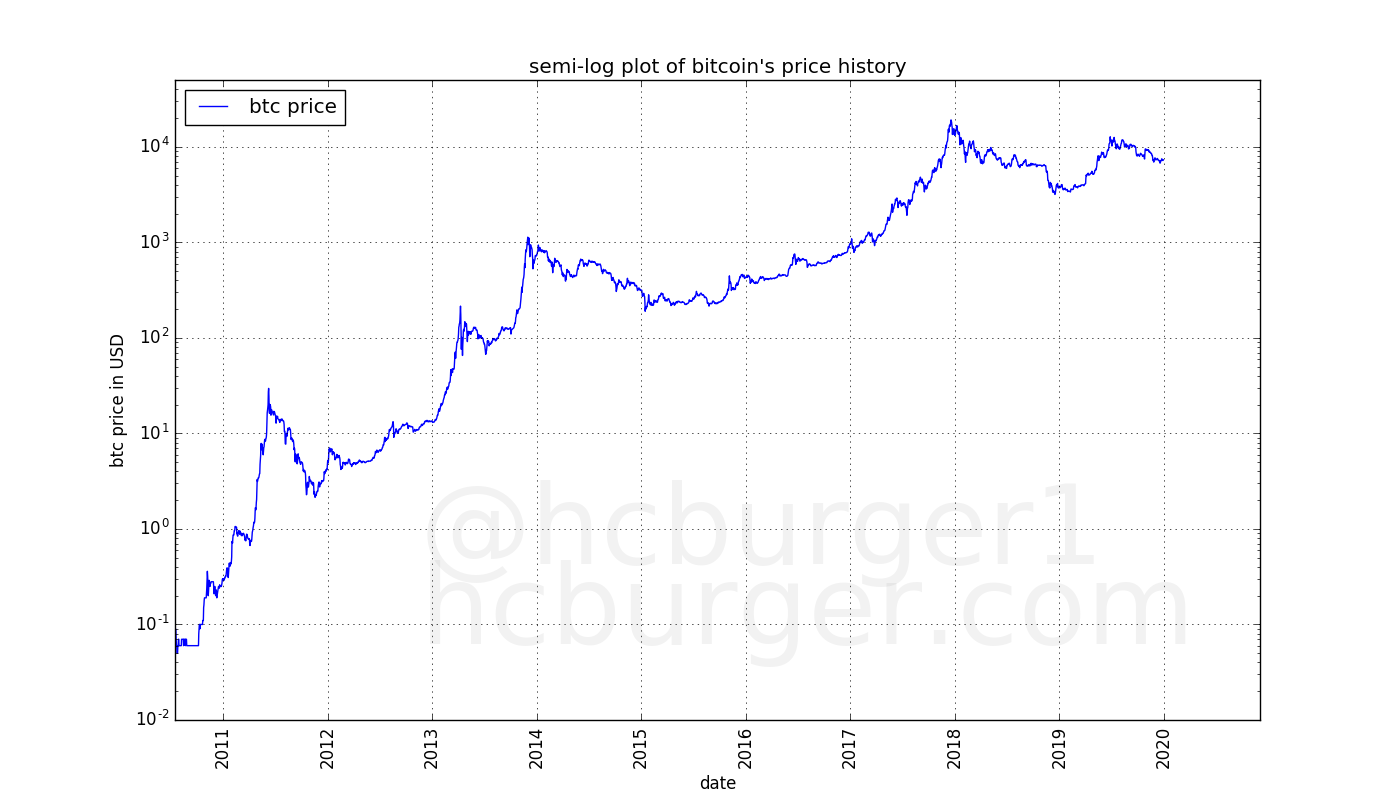

Bitcoin’s price history is best looked at by using a logarithmic scale for the price, giving us as so-called semi-log plot, in which the x-axis represents time and is linear, and the y-axis displays the price of bitcoin, and is scaled logarithmically.

Using a logarithmic scale gives us the advantage of being able to observe bitcoin’s full price history in a single plot. It also has the property that equi-distant movements on the y-axis indicate price changes that are identical in percentage terms. E.g. the price movement from $1 to $10 per bitcoin takes up the same distance on the y-scale as the price movement from $100 to $1000. This property is extremely useful but is not always perfectly understood.

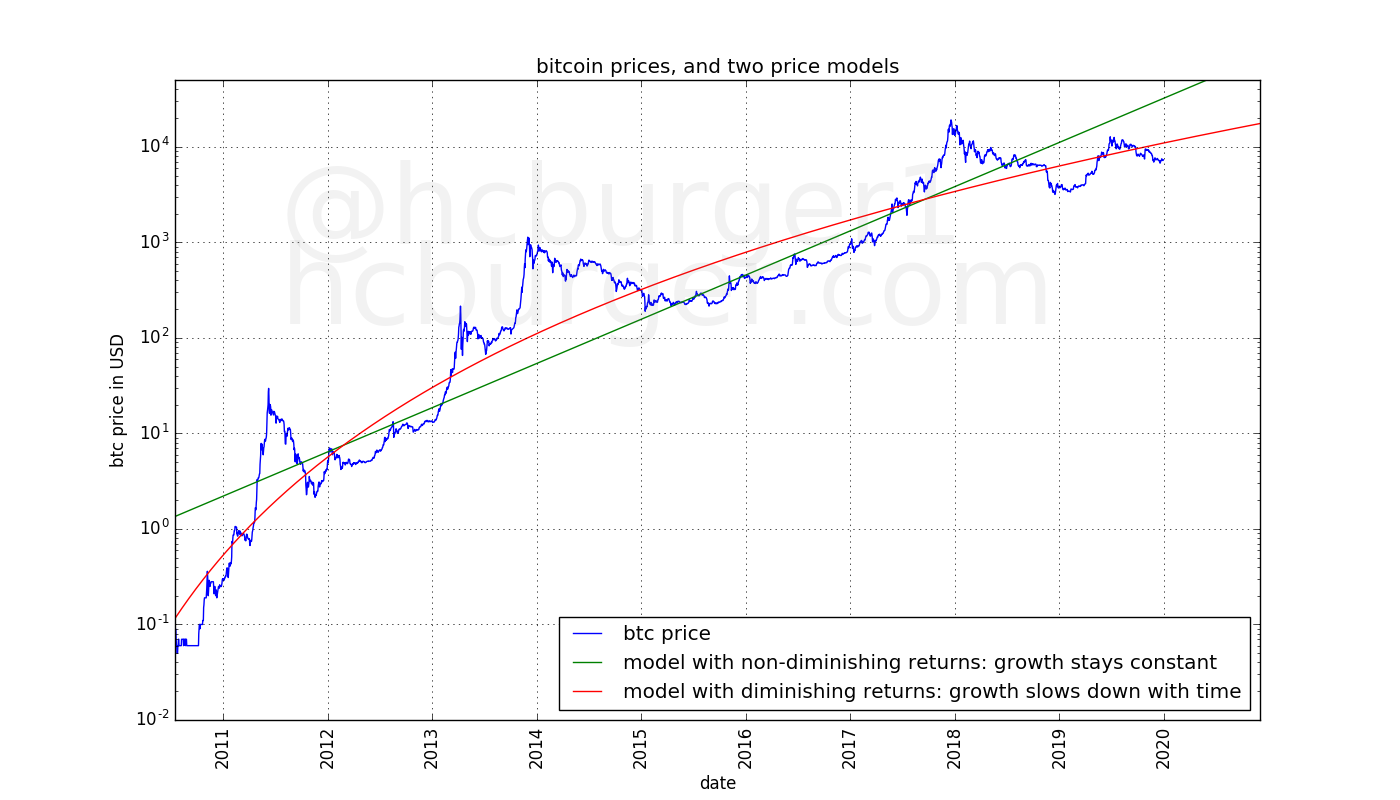

To better understand the properties of a semi-log plot, let’s look at two models:

- one with non-diminishing returns (equal expected growth rates over time)

- one with diminishing returns (growth rates become smaller over time)

I used the equation described in the previous article for the model with diminishing returns, but a different model with slowing growth rates could have been used as well for the purposes of this article.

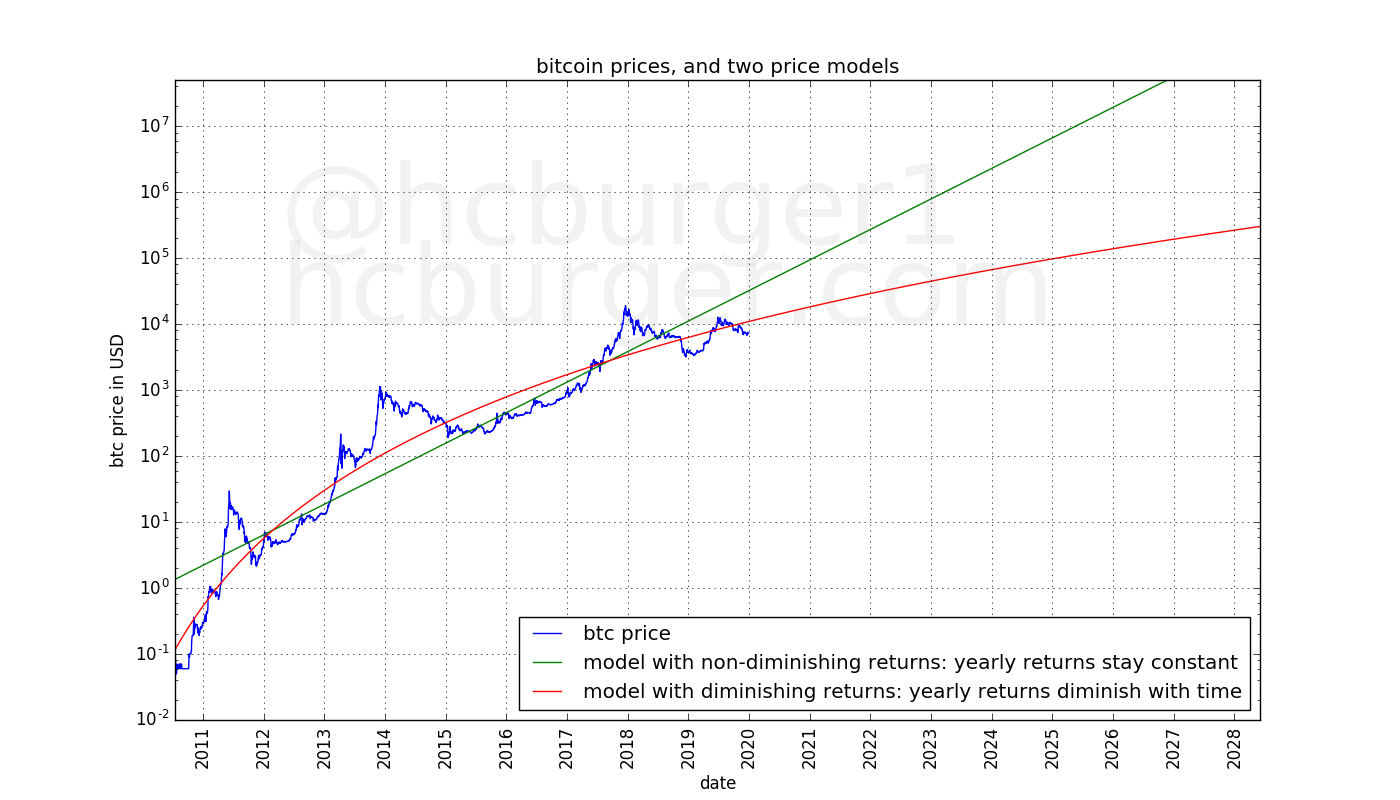

The model with non-diminishing returns displays like a straight line in the semi-log plot, whereas the model with diminishing returns displays like a curve that initially grows quickly, and then more slowly.

Which model should we prefer? The difference between the two is important, as the two predict wildly different prices in the future.

In the previous article, the choice for a model with diminishing returns was mostly motivated by the fact that the bitcoin price curve in the semi-log plot appears to be slowing. Also, the regression error for the model with diminishing returns is “good”: It is about 5.3 times lower than for the model with non-diminishing returns. The model with diminishing returns is therefore empirically better at modeling the data. This already tells us that bitcoin’s long-term growth has diminishing returns, but in this article, we will make some observations that give additional weight to the conclusion that bitcoin’s upward price movements face greater and greater resistance.

Expected returns, long term

Diminishing returns means that bitcoin’s growth is slowing. Non-diminishing returns means that bitcoin’s growth is not slowing down, i.e. the expected growth rate stays the same over time. To better understand the difference between the two, let’s take the perspective of fictional investors.

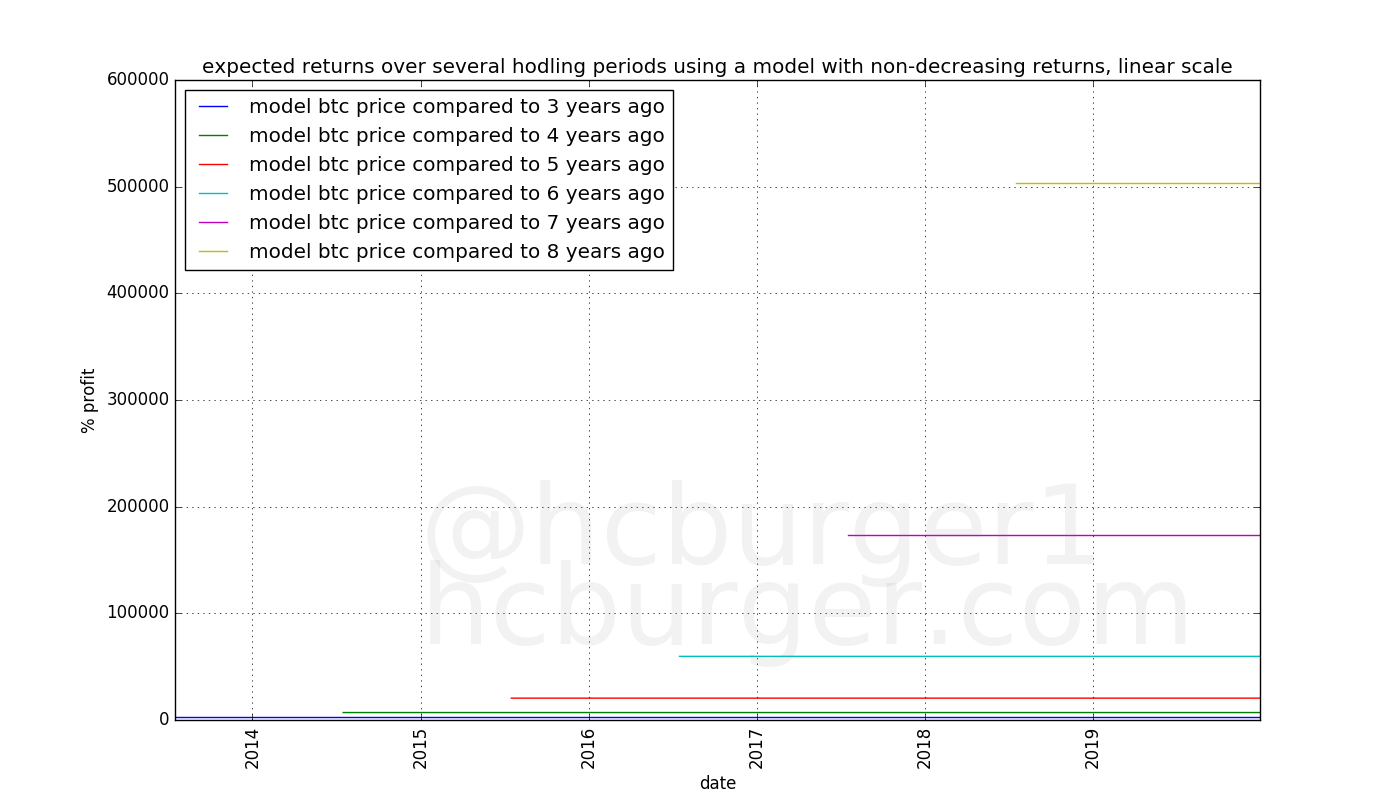

A model with non-diminishing returns

Let’s assume that bitcoin’s price follows a non-diminishing model. How much money can an investor expect to make? The answer depends on the amount of time the investor held his bitcoin before selling them (the “hodling period”). The longer the hodling period, the higher the expected return. What is interesting is that for the model with non-diminishing returns, the profit the investor can expect to make does not depend on when he invested.

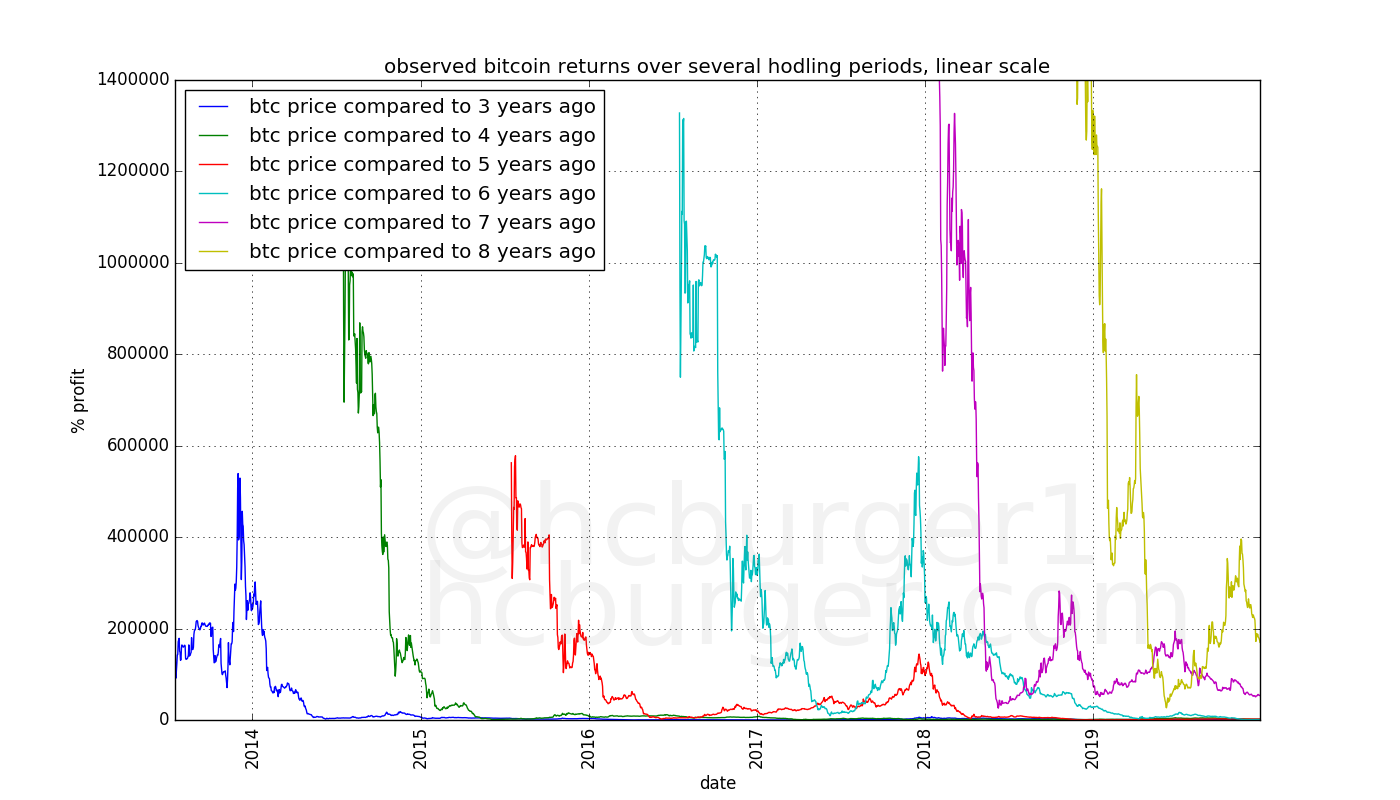

This is demonstrated in the plot below. Each colored line represents one hodling period. The x-value of each point on the line represents the time at which the investor sold his bitcoin. The y-value represents the percent profit he made from his investment.

The longer the hodling period, the later the starting point of the line representing that hodling period. This is because bitcoin’s price history is limited and we assume that it was not possible to invest in bitcoin before the 17th of July 2010. According to this, it is not possible to have held bitcoin for eight years before mid-2018, which is why the yellow line above starts in mid-2018.

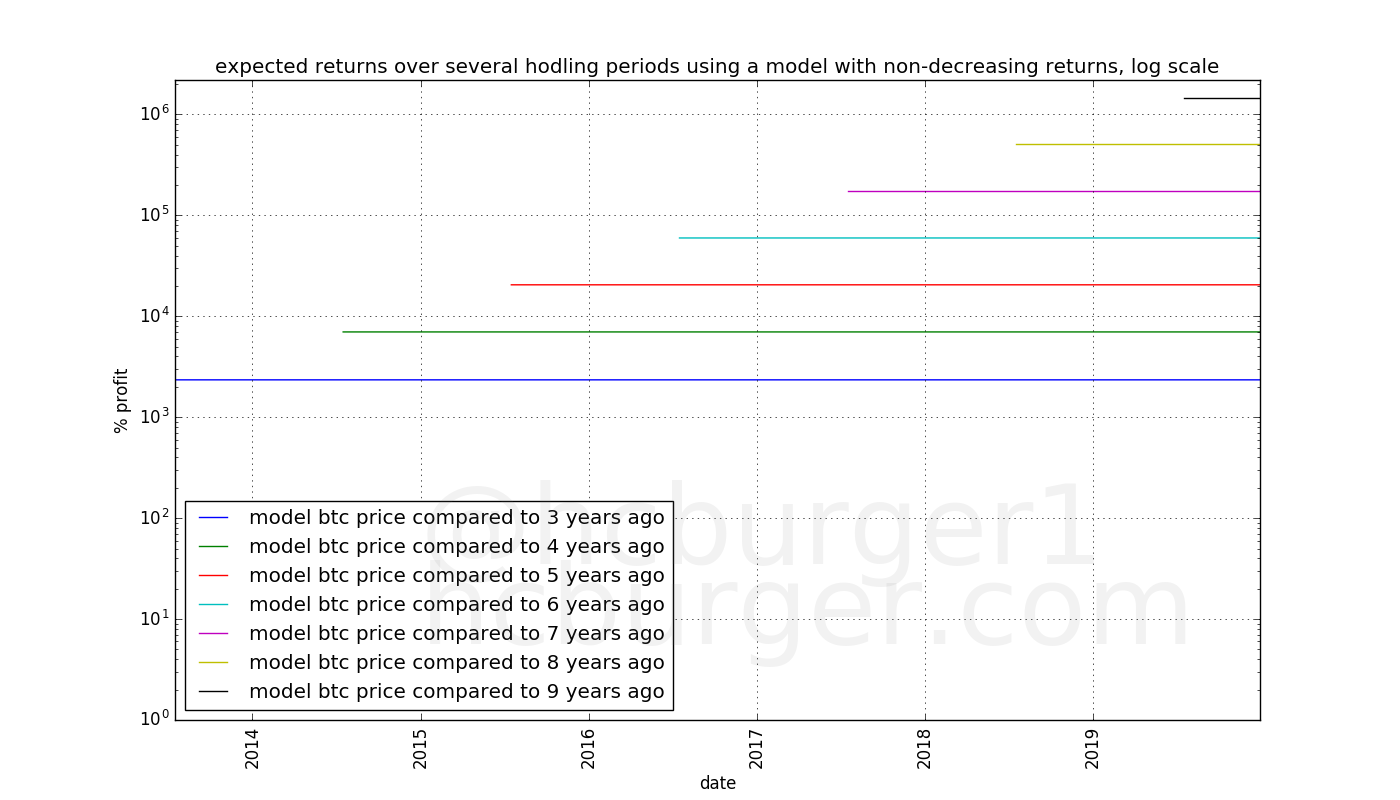

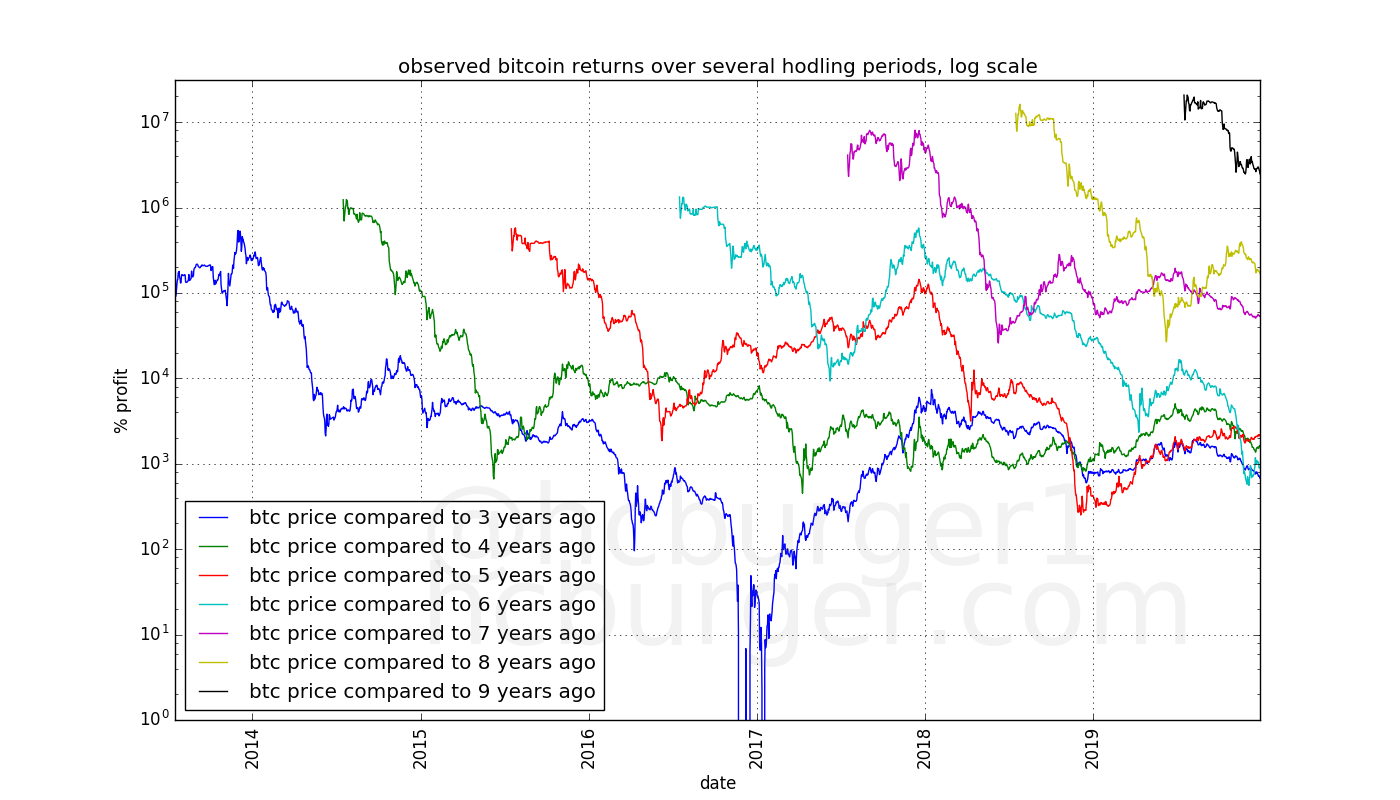

We can display the same data in a semi-log plot:

We see that according to this model, an investor who bought bitcoin and sold them 3 years later would have made a profit of approximately 2500% no matter when this investor bought his bitcoin. The same holds true for any other hodling period, but the returns are higher for longer hodling periods.

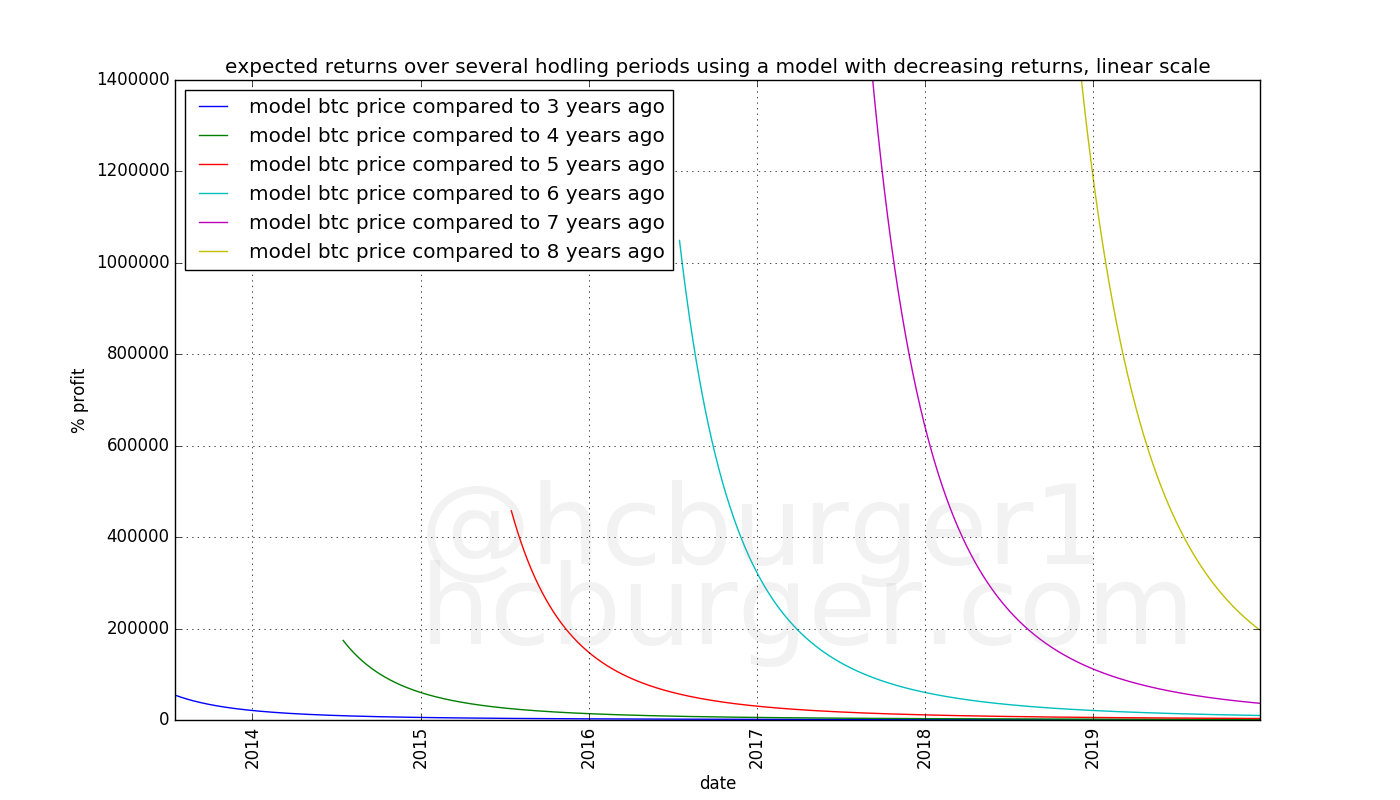

A model with diminishing returns

Using a model with diminishing returns, the situation is different: The expected returns depends on when one invested. The lines in the below plot drop sharply, which means that for the same hodling period, buying earlier gives higher expected returns.

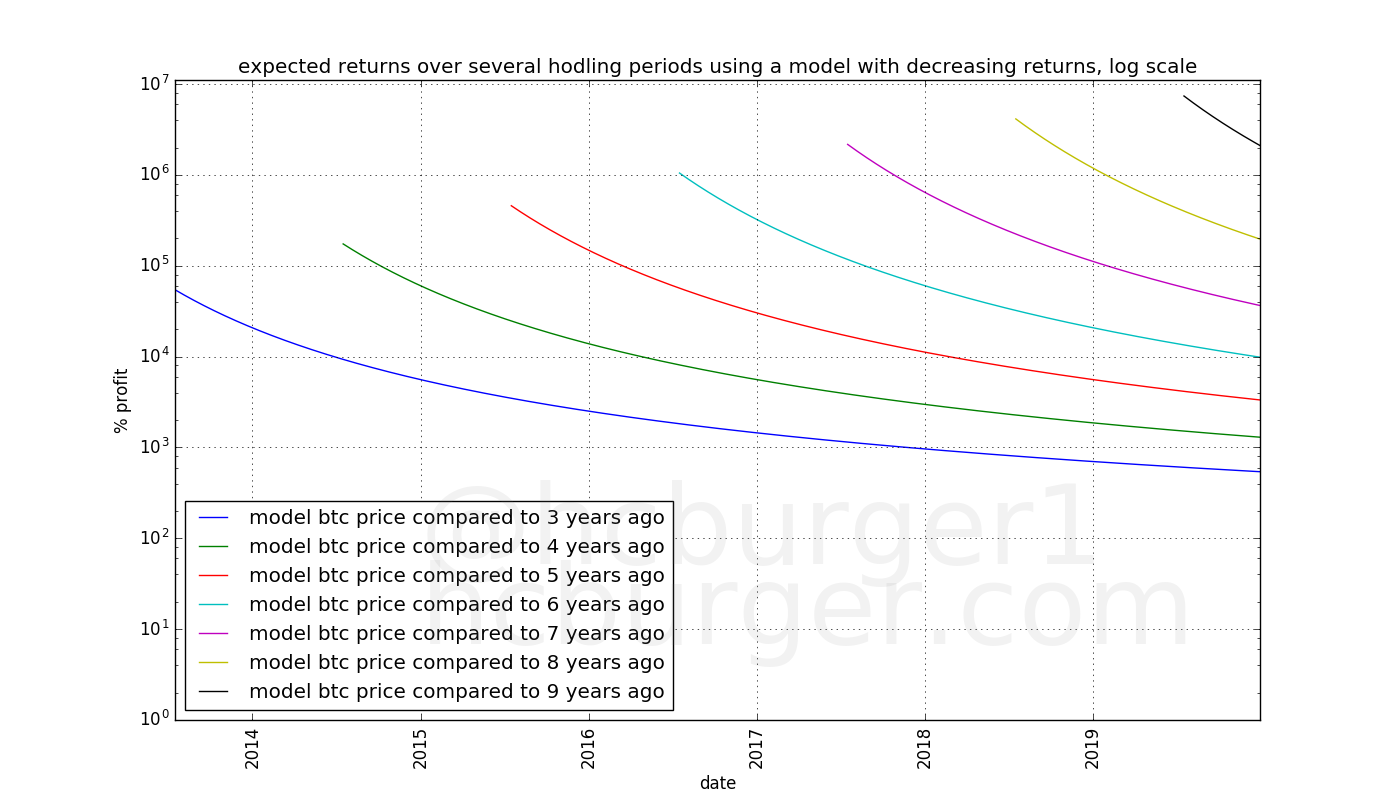

A semi-log plot again makes the data easier to read:

Investor A who bought bitcoin in mid-2011 and sold them three years later in mid-2014 would have made about 10000% profit.

Investor B who bought bitcoin in January 2015 and sold them three years later in January 2018 would have made “only” about 1000% profit, or 10 times less than investor A.

The situation is similar, but even more pronounced for longer hodling periods. A 10x decline in returns occurs faster. Investors A and B invested three and a half years apart, with a 10x difference in returns. For an 8-year hodling period, a 10x decline in returns occurs in about a year.

(Note: For the model with diminishing returns, I used the same model as in my previous article , but the exact choice of the model is not very important here, as the specific numbers are not as interesting as the principle itself.)

Actual returns

The profiles of the expected returns are very different for the model with diminishing compared to the model with non-diminishing returns. The difference is extremely important to anyone who invests in bitcoin. Which of the two models better reflects reality?

To answer this question, we will perform the same exercise as before, but using bitcoin’s actual price history:

What is immediately noticeable are sharp drops in the return curves, which is in agreement with the model with diminishing returns. What is also immediately noticeable is that the curves are much more noisy than those based on model (i.e. simulated) data. The noisiness is due to the wild price swings for which bitcoin is so famous.

In the semi-log chart, we notice very low returns for the 3-year hodlers around the 2017 mark. This is because the price around 2017 was about $1000, approximately the same as during the previous all-time-high, around 2014. Someone who bought at that all-time-high and sold three years later could have made a small loss.

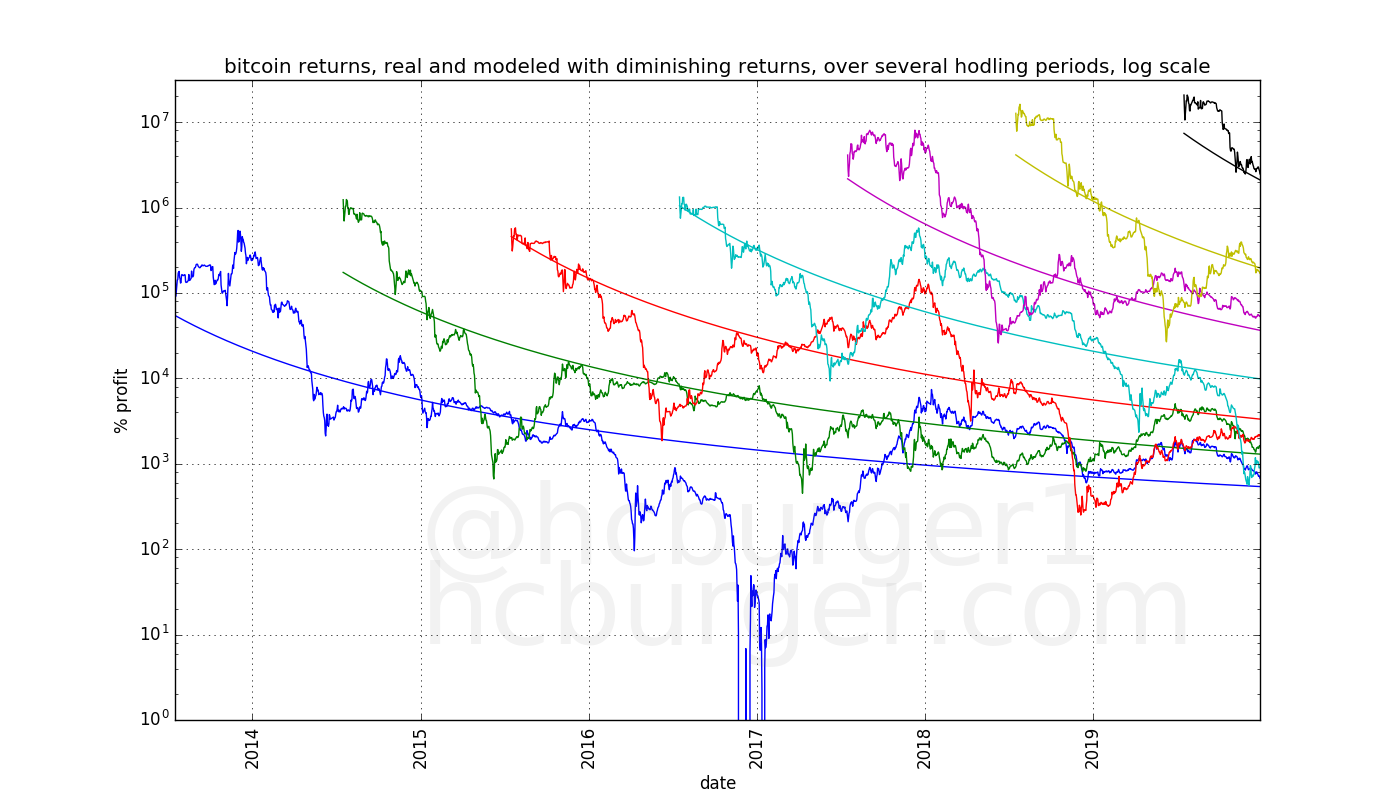

Let us now compare the real return curves to those based on model data using a model with diminishing returns. The same color-code is used for the length of the hodling periods:

We see that the real return curves are modeled adequately by the model with diminishing returns, but we have to take into account that there is quite a lot of noise.

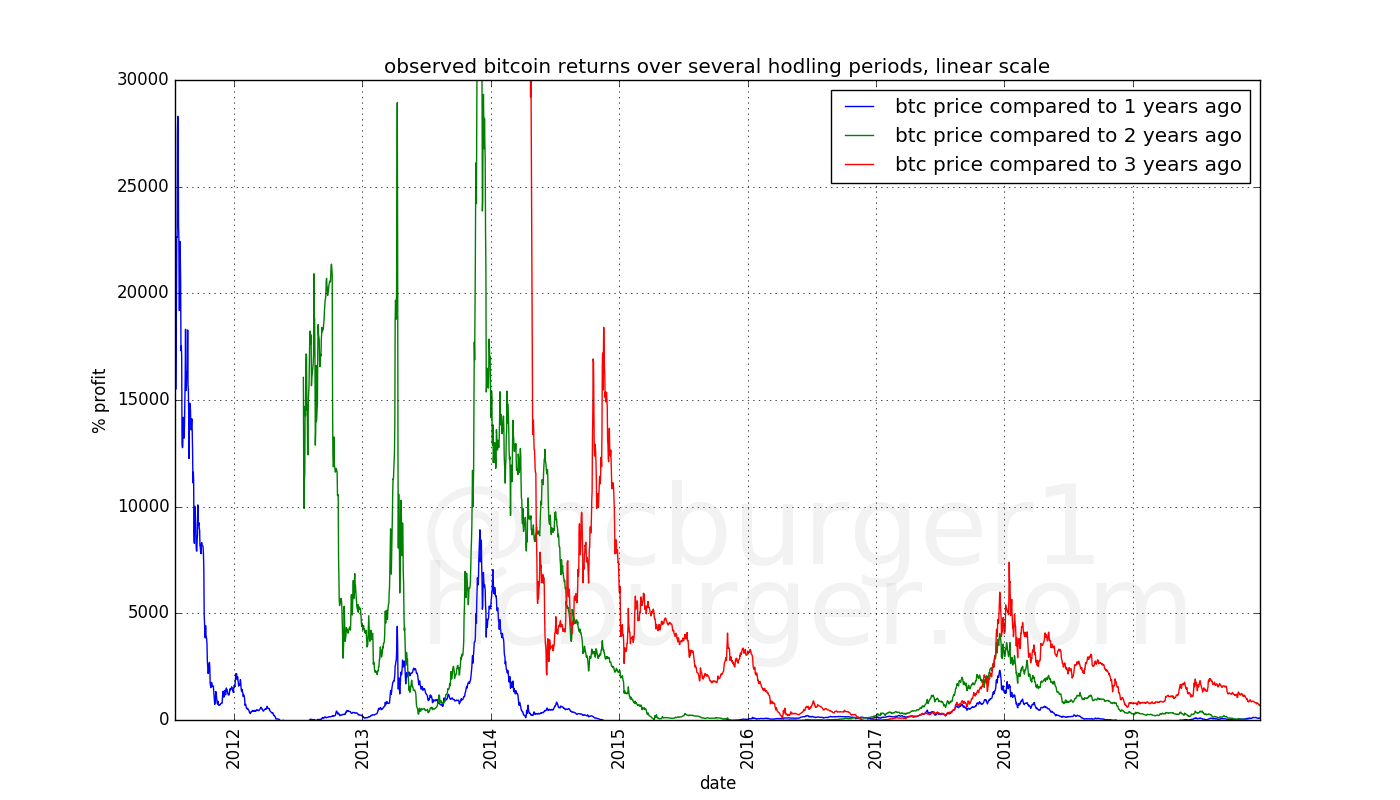

We can also repeat the experiment for shorter hodling periods, and see a similar, but more noisy, pattern.

The return curves above show us that by the end of the year 2014 at the latest, the nature of bitcoin’s diminishing returns should have become apparent. Later data confirmed that trend.

Conclusions regarding long-term trends

The return curves empirically favor a bitcoin price model with returns that diminish over time. Looking at the three- and four-year return curves, this effect would have been observed at the latest by the end of the year 2014. Newer data has only been confirming this conclusion.

The effects of diminishing returns, combined with price volatility, are:

- The expected returns for all hodlers diminish over time

- The expected returns for long-term hodlers become closer to those of shorter-term hodlers. Due to price volatility, this also means that short-term holders can sometimes have higher returns than long-term hodlers.

The conclusions regarding long-term diminishing returns were already drawn in “Bitcoin’s natural long-term power-law corridor of growth” but we have looked at this effect in a novel way in this article, and have also seen that the effect would have been visible as early as 2014, or maybe even earlier. Also different from the previous article is that we arrive to similar conclusions without using a precise model. The general conclusions are therefore independent of the exact choice of the model.

Why is the price growing slower and slower?

Given the observation that bitcoin’s price growth exhibits diminishing returns, can we come up with a plausible ad-hoc explanation?

Probably the simplest explanation is that increasing the price of bitcoin by a certain amount in percentage terms requires more and more fiat currency. To illustrate: Increasing the price of bitcoin by 100% took relatively little capital when the price of bitcoin was $0.1. It requires much more capital to move the price of bitcoin from e.g. $10000 to $20000.

Attracting ever more capital becomes ever more difficult, or at least, takes more and more time. Perhaps a single individual with modest funds could have moved the price from $0.1 to $0.2, but it would take a very wealthy individual to move the price from $10000 to $20000. Alternatively, the price could be moved from $10000 to $20000 by a greater number of individuals.

Attracting more and more people to invest in bitcoin, or finding a few exceptionally wealthy individuals takes more and more time.

Short-term price changes

Does the above explanation for slower long-term growth rates also have an effect on shorter-term growth rates? This is something that has not been thoroughly considered in “Bitcoin’s natural long-term power-law corridor of growth”. Yet, higher bitcoin prices should make it more difficult to move the price in the short-term, too. This would mean that short-term price swings should become more tame over time, leading both to overall lower volatility and also potentially slower bull markets.

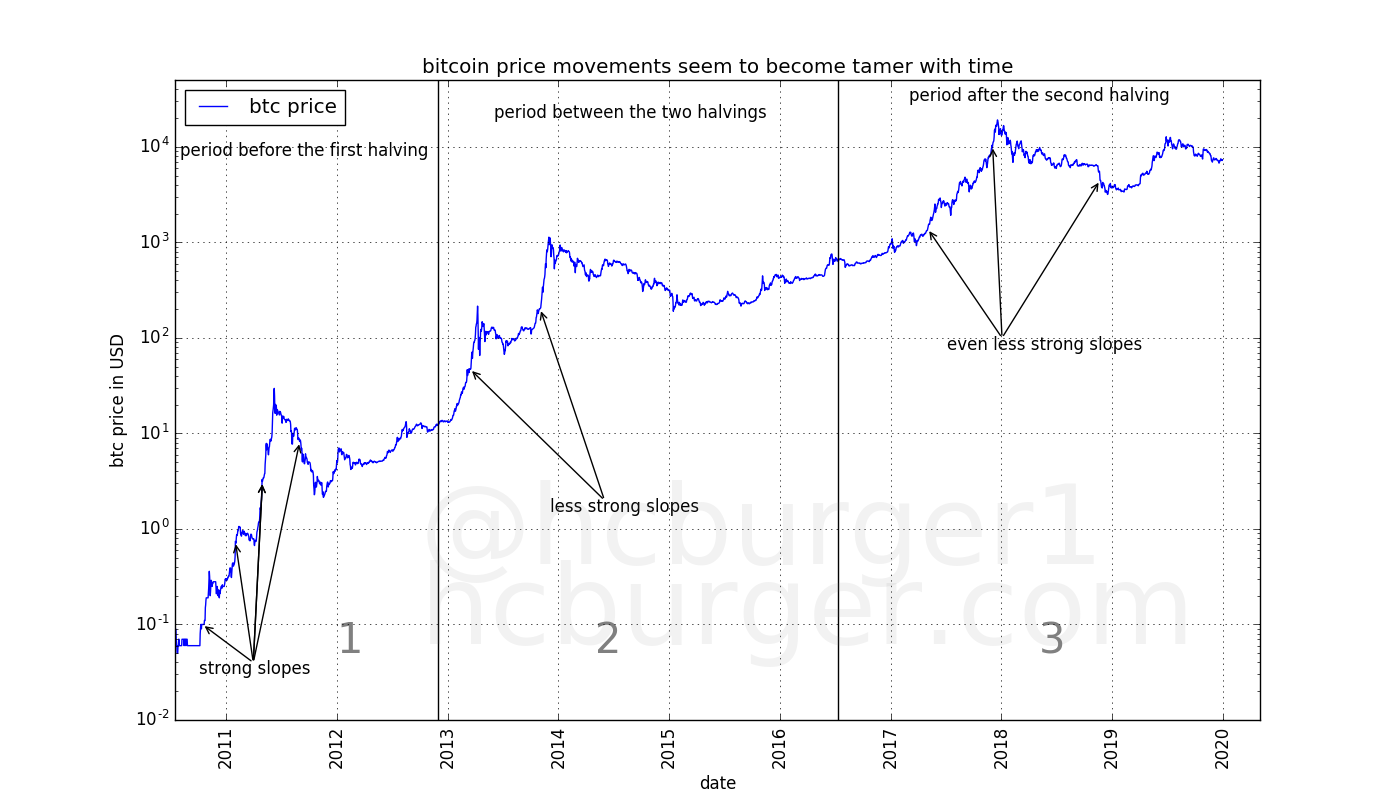

To answer this question, let’s divide bitcoin’s price history into three parts, one for each halving period:

- the period before the first halving (“halving period 1”),

- the period after the first halving and before the second halving (“halving period 2”), and

- the period after the second halving (“halving period 3”).

We observe the strongest price swings during bitcoin’s bull markets. The corrections following a bull market also have strong (downward) price swings. At first sight, it would appear that these shorter-term price movements become slower in the later periods, which also leads to bull markets taking longer and longer to develop:

Let’s consider the slopes of the price curve. A given slope corresponds to a given price change in percentage terms, due to the nature of semi-log plots. Instead of talking about price changes in percentage terms, we can talk about differences in the log price. The two are completely equivalent.

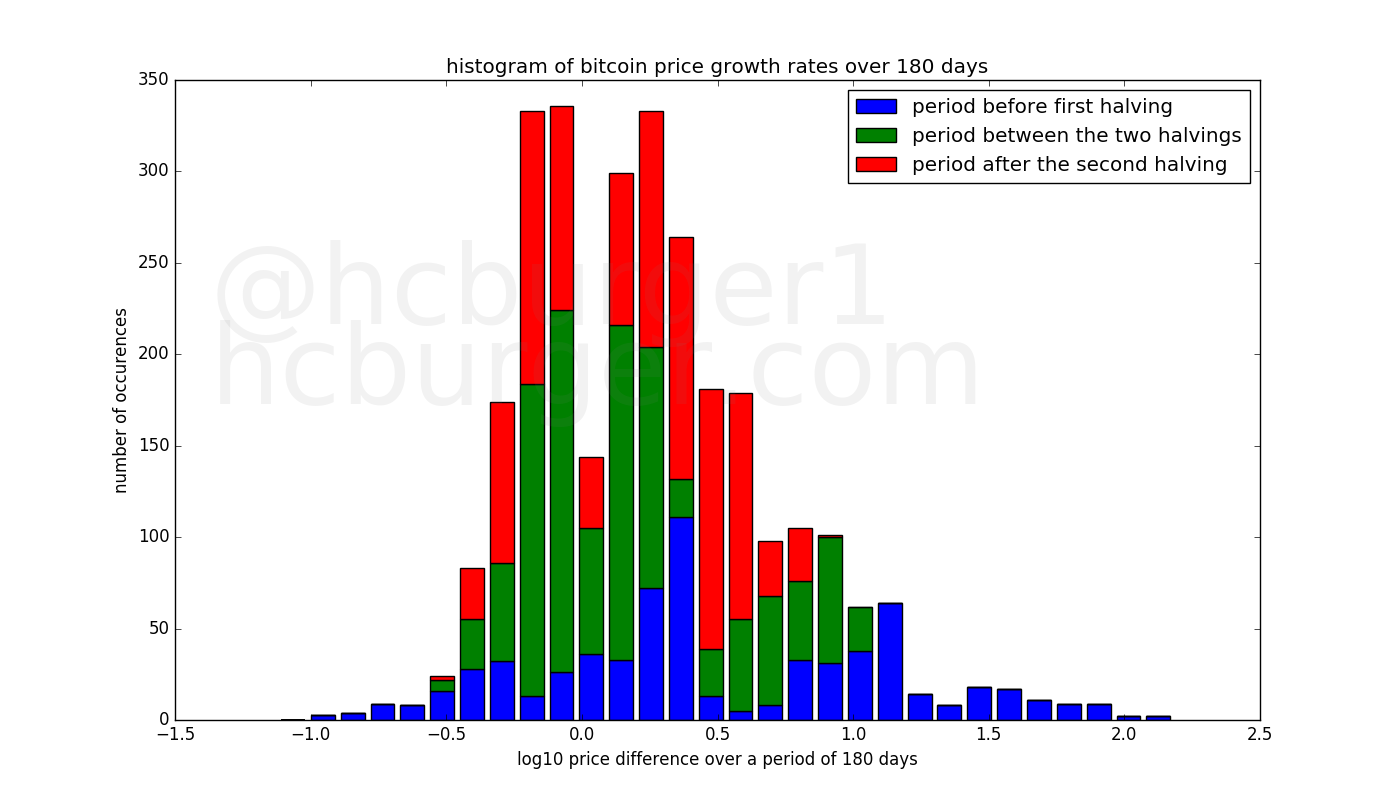

In each period, let’s consider the slopes of bitcoin’s price movement over a particular timeframe, e.g. 180 days. For each 180 day timeframe, we will look at the difference between the log price at the beginning and the log price at the end of that timeframe. We then count how often this difference falls into a particular range. The result is a histogram of bitcoin log price growth rates over 180 days. The growth rates are equivalent to slopes in the semi-log plot of the price history. Negative log price changes mean that the price has been declining.

The histogram of the 180 day growth rates for the three halving periods can be displayed in a table:

(Period 1 corresponds to the period before the first having, period 2 to the period between the two halvings, and period 3 to the period after the second halving).

What becomes immediately apparent is that the earlier halving periods have more extreme growth rates, in both the positive and negative direction. For example, the first period had 180-day growth rates of between -1.01 and -0.57 and also between 1.08 and 2.18, whereas the later halving periods do not. The second halving period has 24 instances of 180-day growth rates of between 0.97 and 1.08, whereas the third has none.

The same data can be displayed visually, allowing for easier inspection:

The blue bars representing the distribution of the growth rates of the first halving period are more spread out than the green and red bars representing the two other periods. A greater vertical size of a bar indicates a higher count in that bin. The earliest halving period is the most spread out, the second less so, and the third halving period the least.

Alternatively to the histogram, we can also consider the statistics of the 180-day growth rates for the three periods. The first number is expressed in log10 terms, whereas the number in parenthesis is expressed in percentage terms.

Halving period 1 (before the first halving):

- max growth rate: 2.156613 (14242 %)

- 90th percentile growth rate: 1.410404 (2473 %)

- 10th percentile growth rate: -0.352216 (-56 %)

- min growth rate: -0.996782 (-90 %)

Halving period 2 (between the two halvings):

- max growth rate: 1.079093 (1100 %)

- 90th percentile growth rate: 0.810624 (547 %)

- 10th percentile growth rate: -0.225461 (-40 %)

- min growth rate: -0.518089 (-70 %)

Halving period 3 (after the second halving):

- max growth rate: 0.862816 (629 %)

- 90th percentile growth rate: 0.586342 (286 %)

- 10th percentile growth rate: -0.251239 (-44 %)

- min growth rate: -0.465312 (-66 %)

The maximum growth rate over a 180-day hodling period was 14242% in the first halving period, 1100% in the second, and 629% in the third halving period. The strongest negative growth rates over a 180-day hodling period was 90% in the first halving period, 70% in the second, and 66% in the third halving period, indicating that downward swings (over a 180-day span) have also become tamer over time.

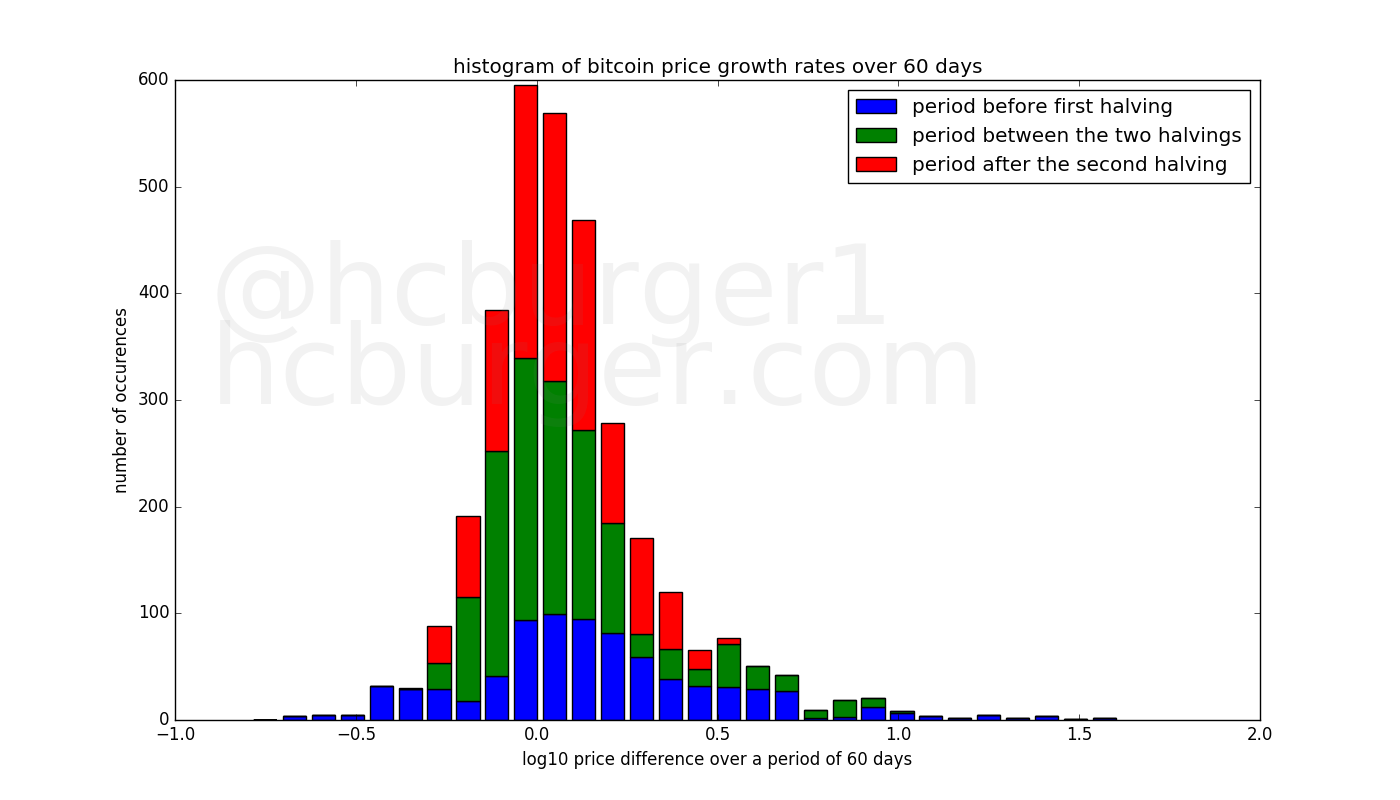

Similar observations can be made when the 180-day holding period is changed, e.g. to 60 days:

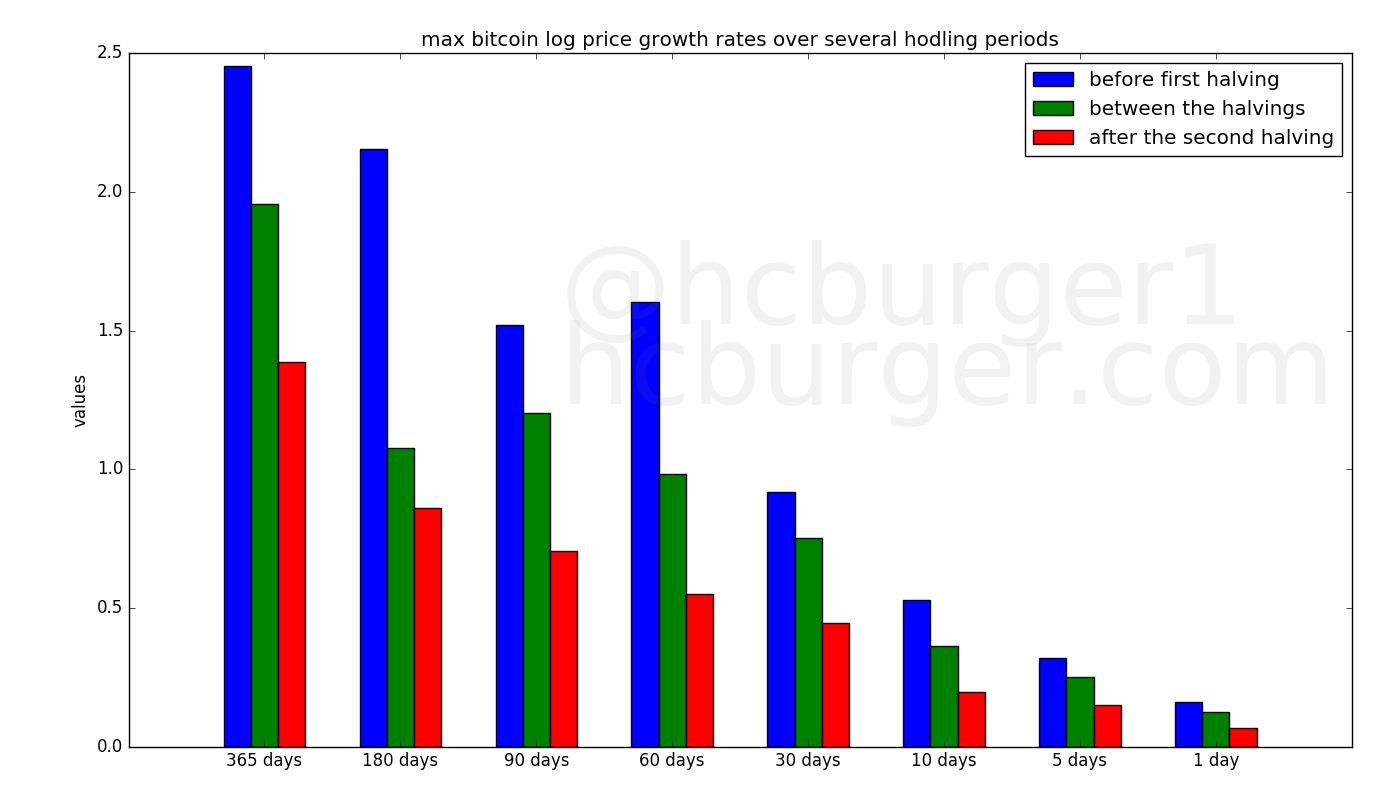

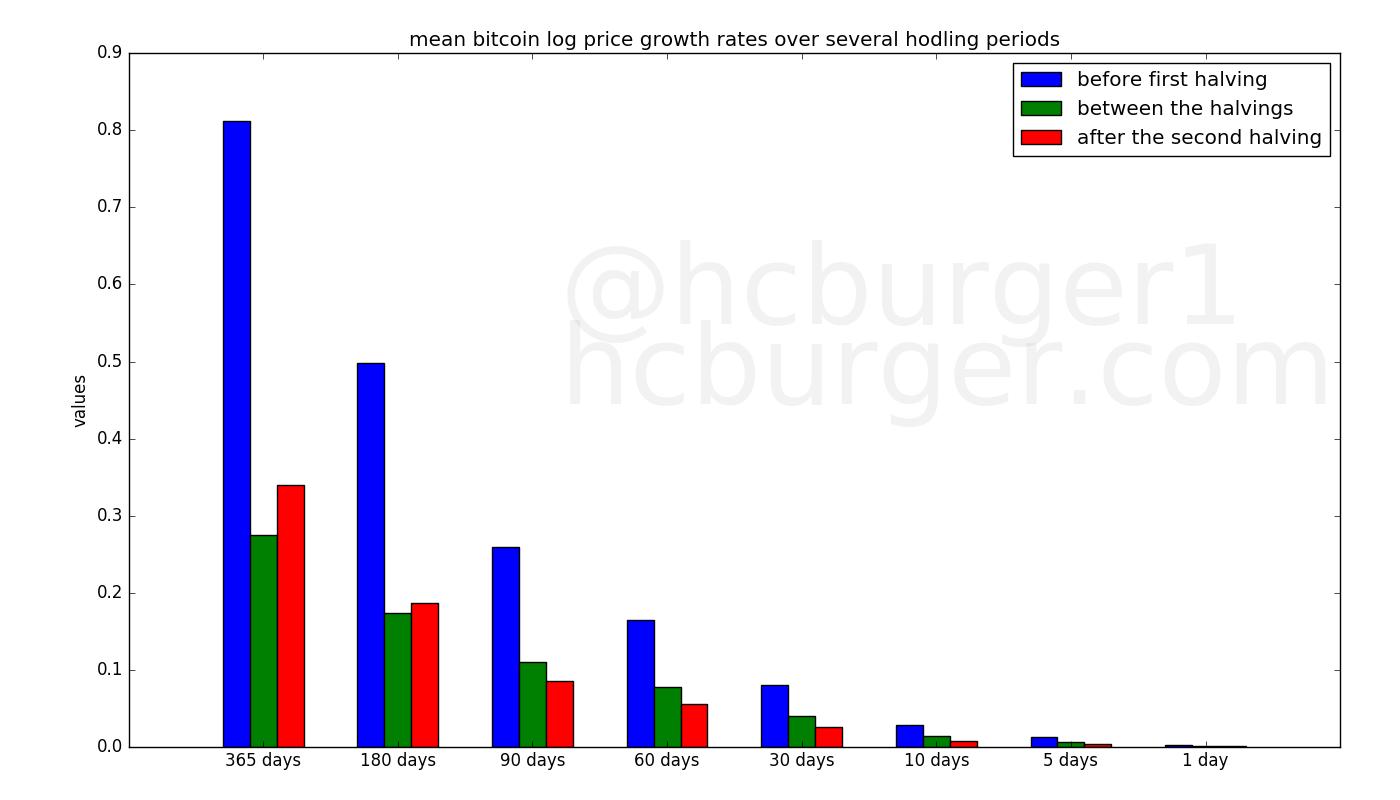

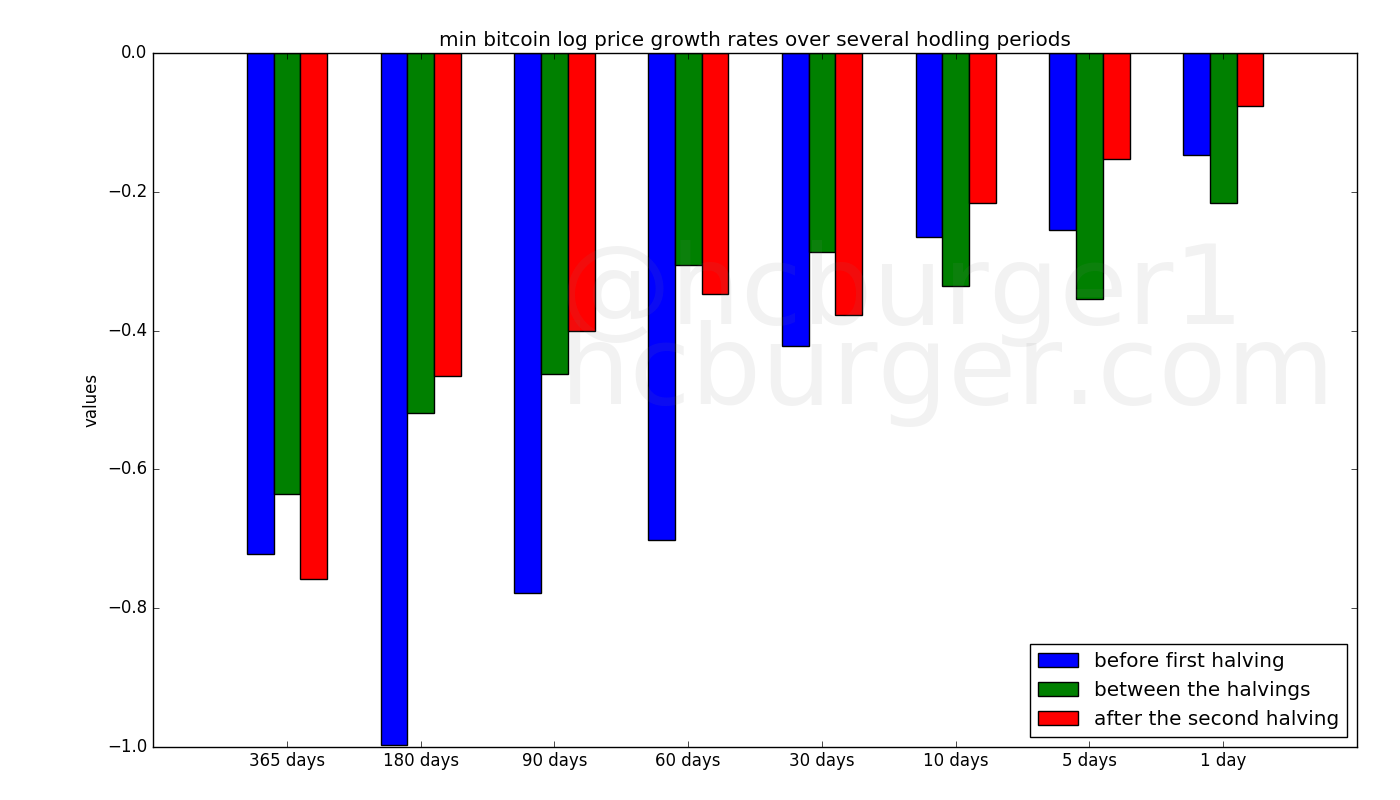

The maximum growth rate over several hodling periods systematically declines over the three bitcoin halving periods:

The mean growth rates over most hodling periods also declines over the three halving periods. This is just a reflection of the fact that the price of bitcoin has been increasing at a slower and slower rate.

The value of the minimum growth rate over several hodling periods also tends to decrease over the three halving periods, though this effect is less marked than for the maximum growth rate.

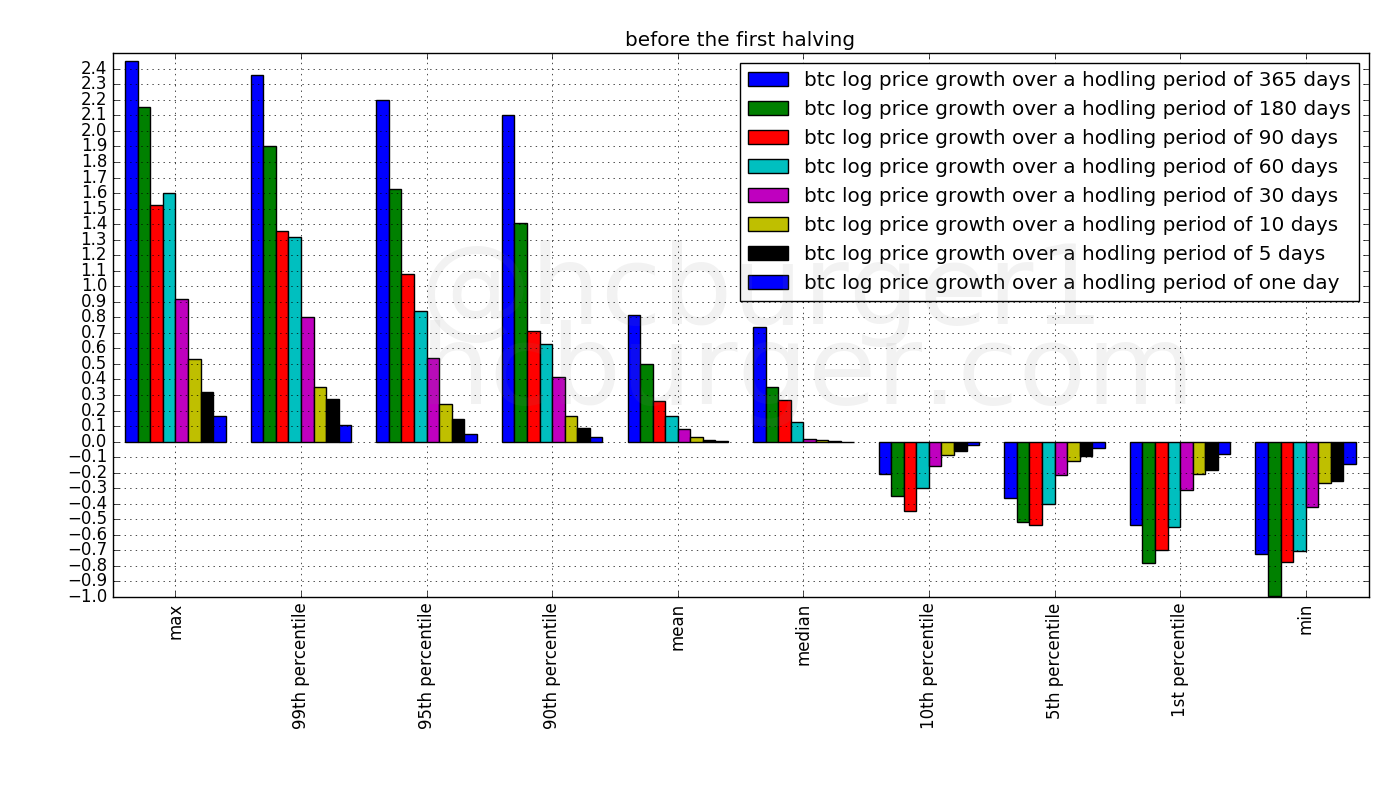

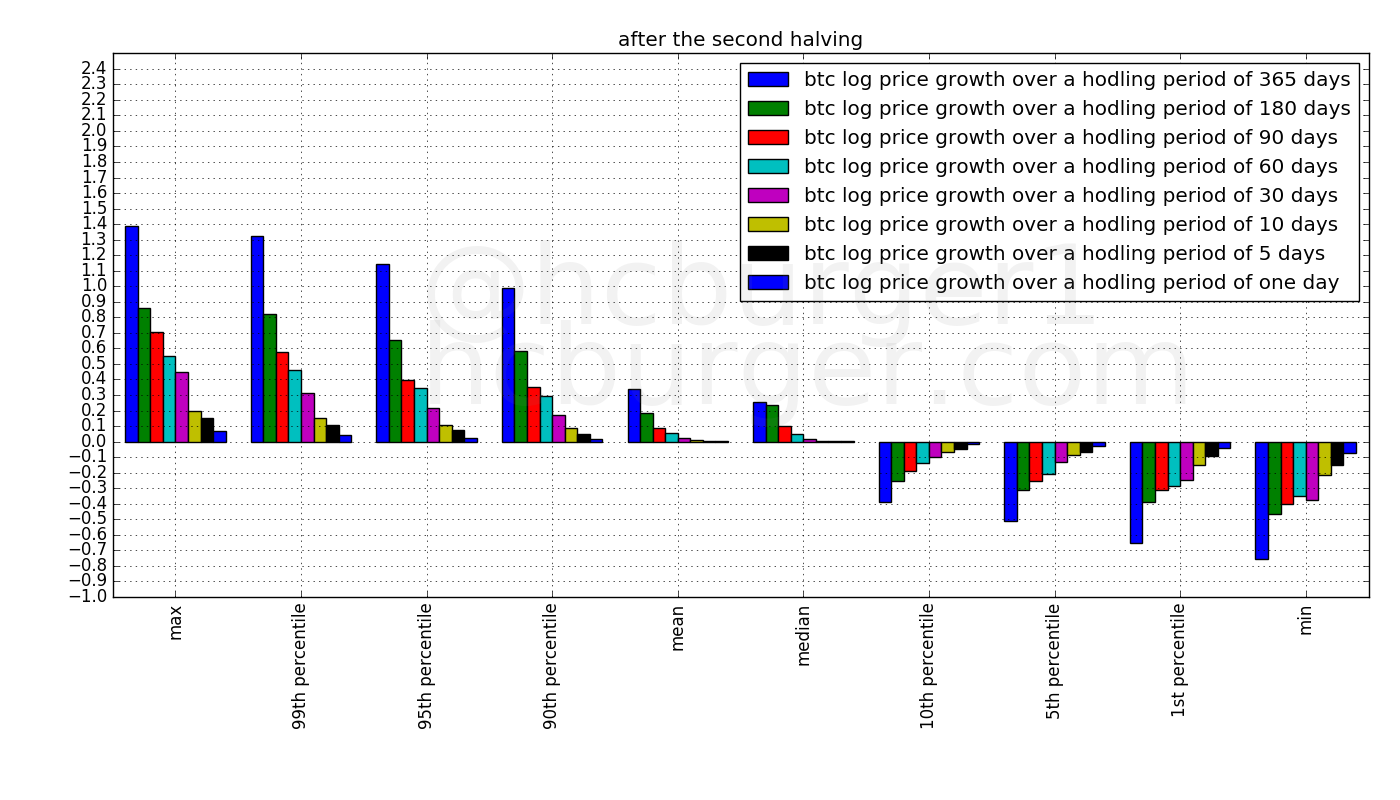

Let’s now make one plot per halving period. Each plot contains several statistics over several hodling periods. The percentiles are statistics that lie between the min and the max, so that e.g. the 90th percentile can be used as a form of “attenuated max”, or the 10th percentile as a form of “attenuated min”. The 50th percentile is the same as the median.

The following plot displays the statistics for the first halving period:

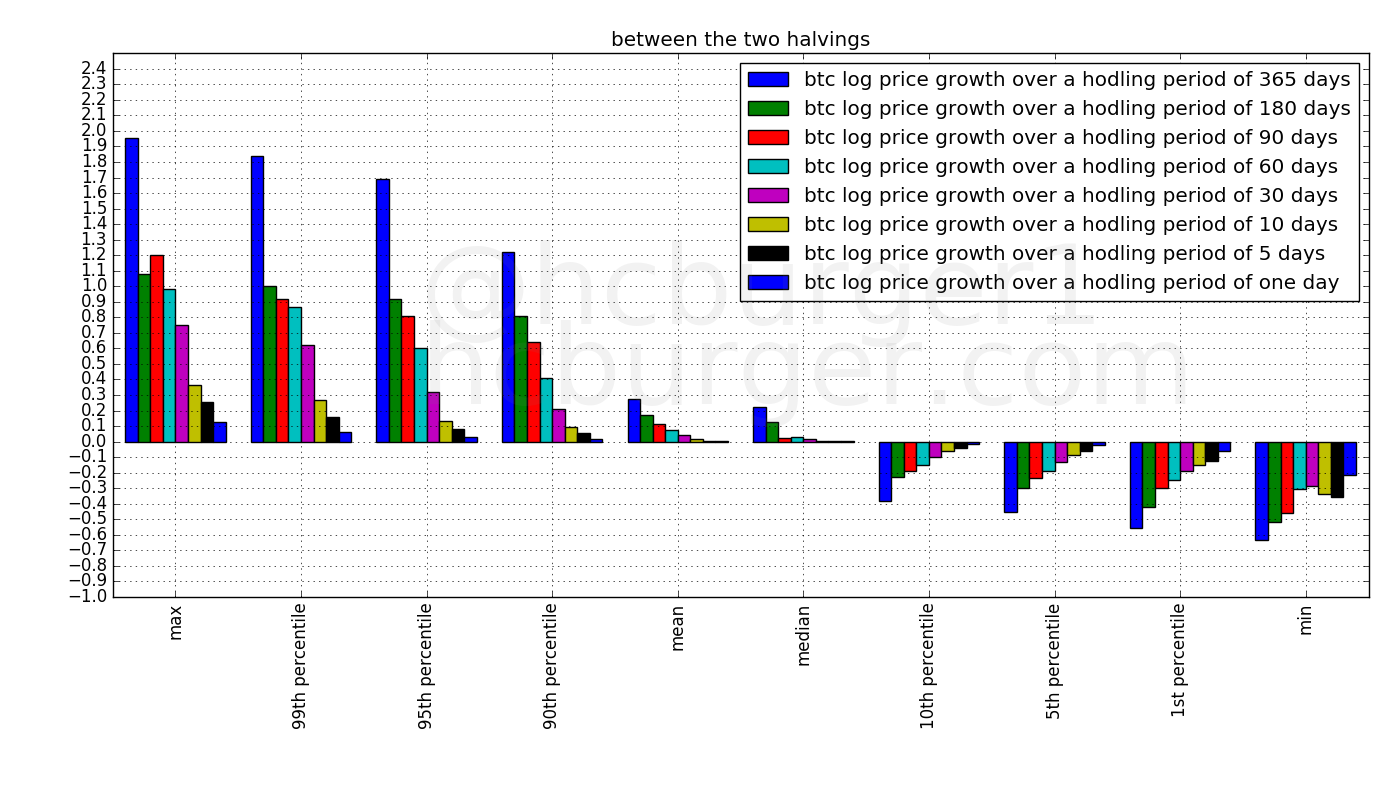

The next plot displays the statistics for the second halving period. The y-axis still uses the same scale. The fact that almost all bars have shorter length means that the statistics over most hodling periods have been attenuated.

The statistics are further attenuated from the second to the third halving period:

These three plots confirm that the positive growth rates over relatively short hodling periods become smaller and smaller in each succeeding halving period. To a lesser extent, negative growth rates also become smaller over time.

These observations are in agreement with our explanation that it takes ever more capital to cause price fluctuations, and hence price fluctuations become tamer. We should expect this trend to continue in the future.

The statistics computed above can also be represented graphically. In the following plot, we display the statistics of each halving period at the end of that halving period, anchored at the price at that given time. The vertical width of the red regions represents the difference between the min and the max growth rates. The red regions have a horizontal width of 365 days because that is the longest short-term hodling period we have considered. Darker red tones just represent different percentiles.

This is another convenient representation showing that the statistics over the short term have become tamer in successive halving periods.

Future price developments

We have two ways of looking at price predictions and models. Assessing whether:

- the long-term projections are realistic

- the short-term projections are realistic.

Let’s look at a few potential scenarios.

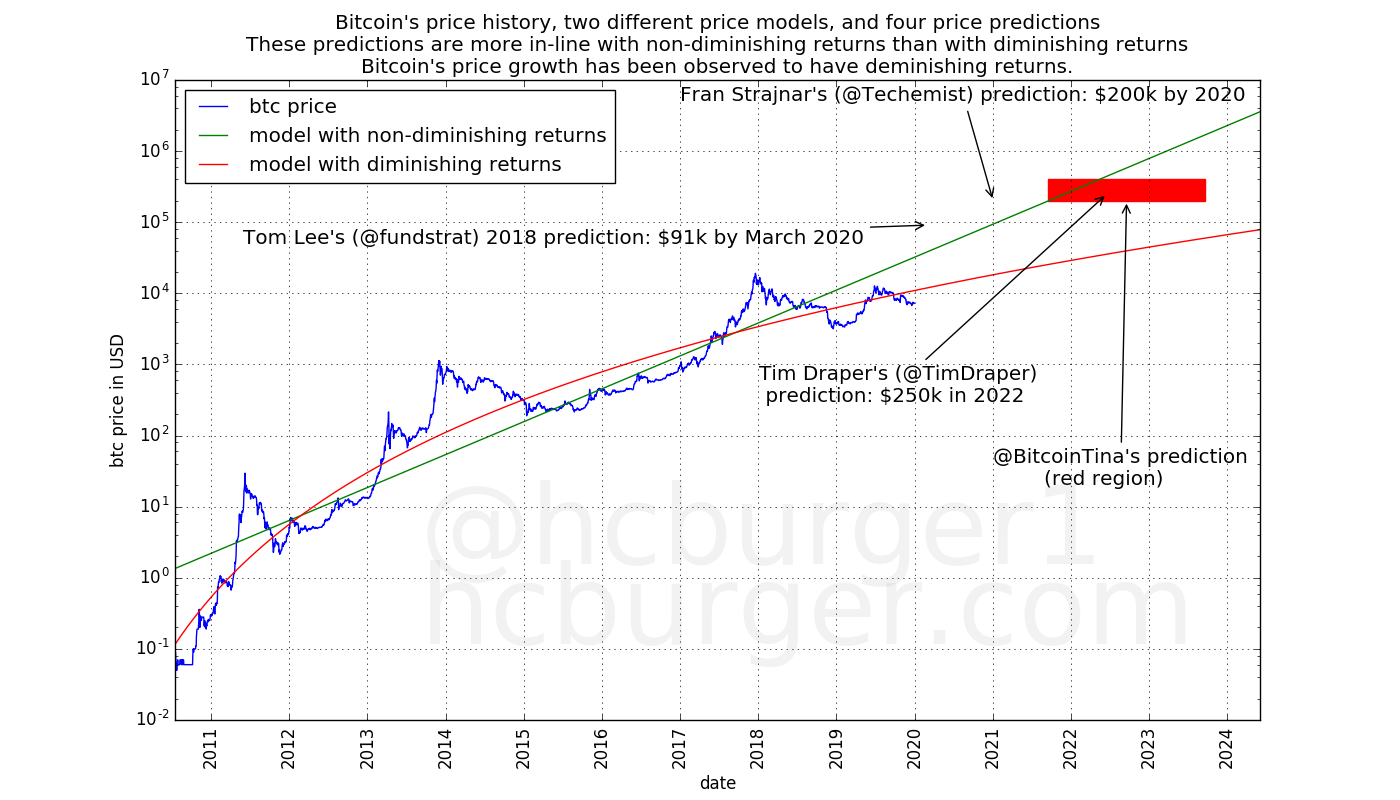

Predictions made by individuals

It appears that it is believed by some that bitcoin’s price will grow with non-diminishing returns, leading to some price predictions being made that are more in-line with the model with non-diminishing returns than with the model with diminishing returns:

Source of the predictions for Tom Lee and Fran Strajnar, Tim Draper, and BitcoinTina.

Since these predictions are not in line with diminishing returns, and we have empirically observed long-term price growth to be diminishing, it would be surprising for any of these predictions to come true.

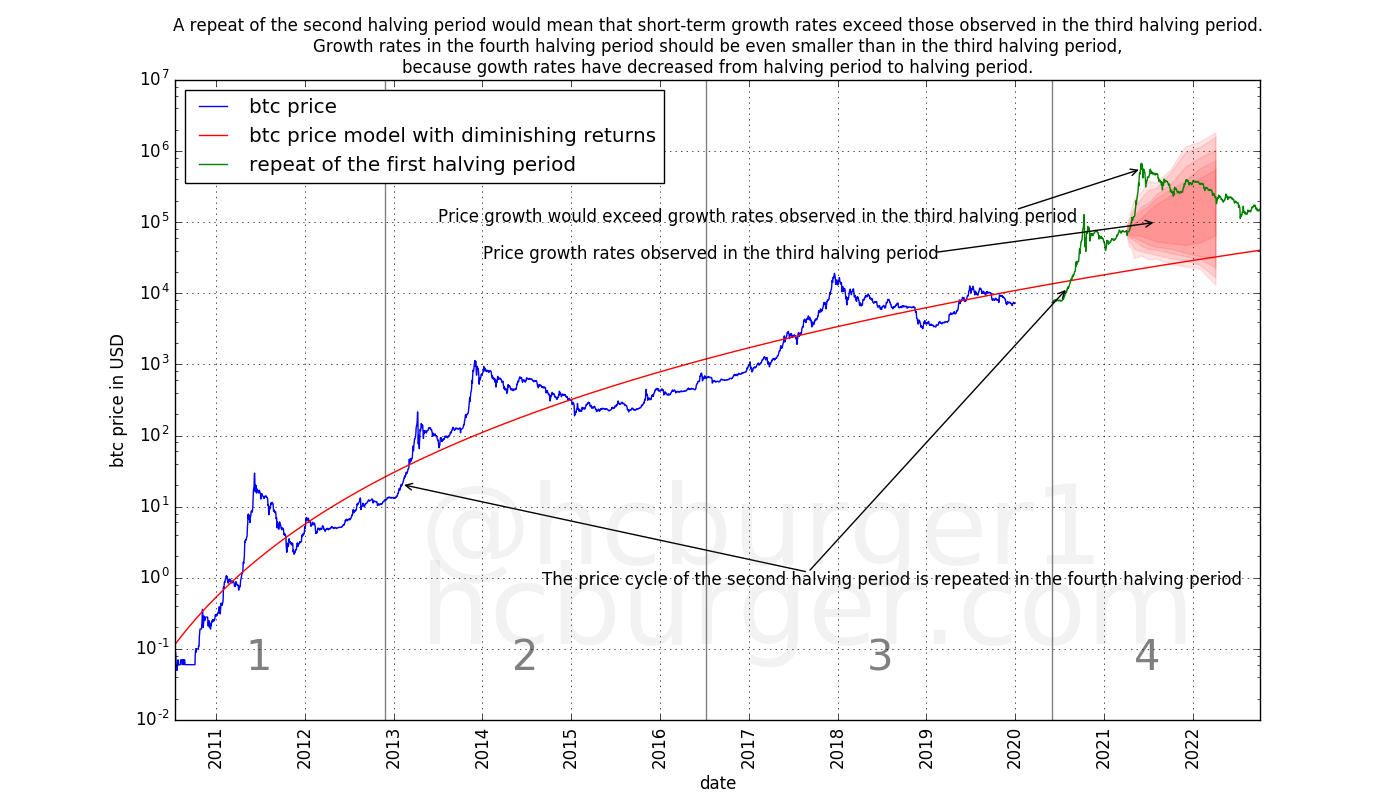

Cycle repeats

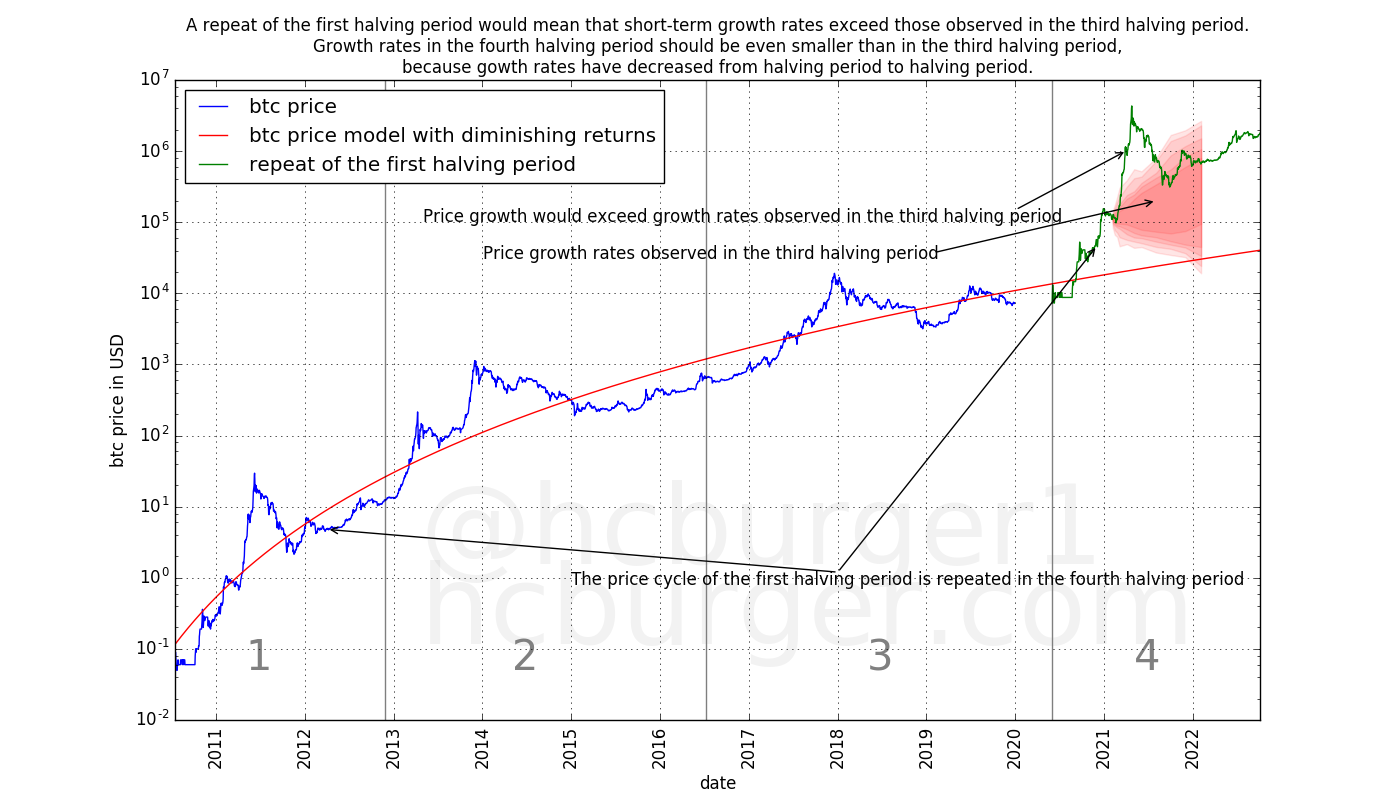

We can also ask ourselves if it is possible for history to repeat itself. E.g. could the price movements observed in the first halving period repeat themselves after the next halving?

For that to be possible, the hypothetical price movements should at least agree with the statistics observed in the third halving period. In fact, we expect the statistics of the price movements in the fourth halving period to be even more tame than those observed in the third period. However, we have not observed any statistics for the fourth having period, so we’re going to work with statistics from the third halving period for now.

The above plot shows a repeat of the first halving period after the third halving. We see that price movements are too extreme and lie outside the range observed in the third halving period. We should therefore consider a scenario with such strong short-term price fluctuations as unlikely.

What about a repeat of the second halving cycle? The same conclusion holds: the short-term price fluctuations seem to be too strong.

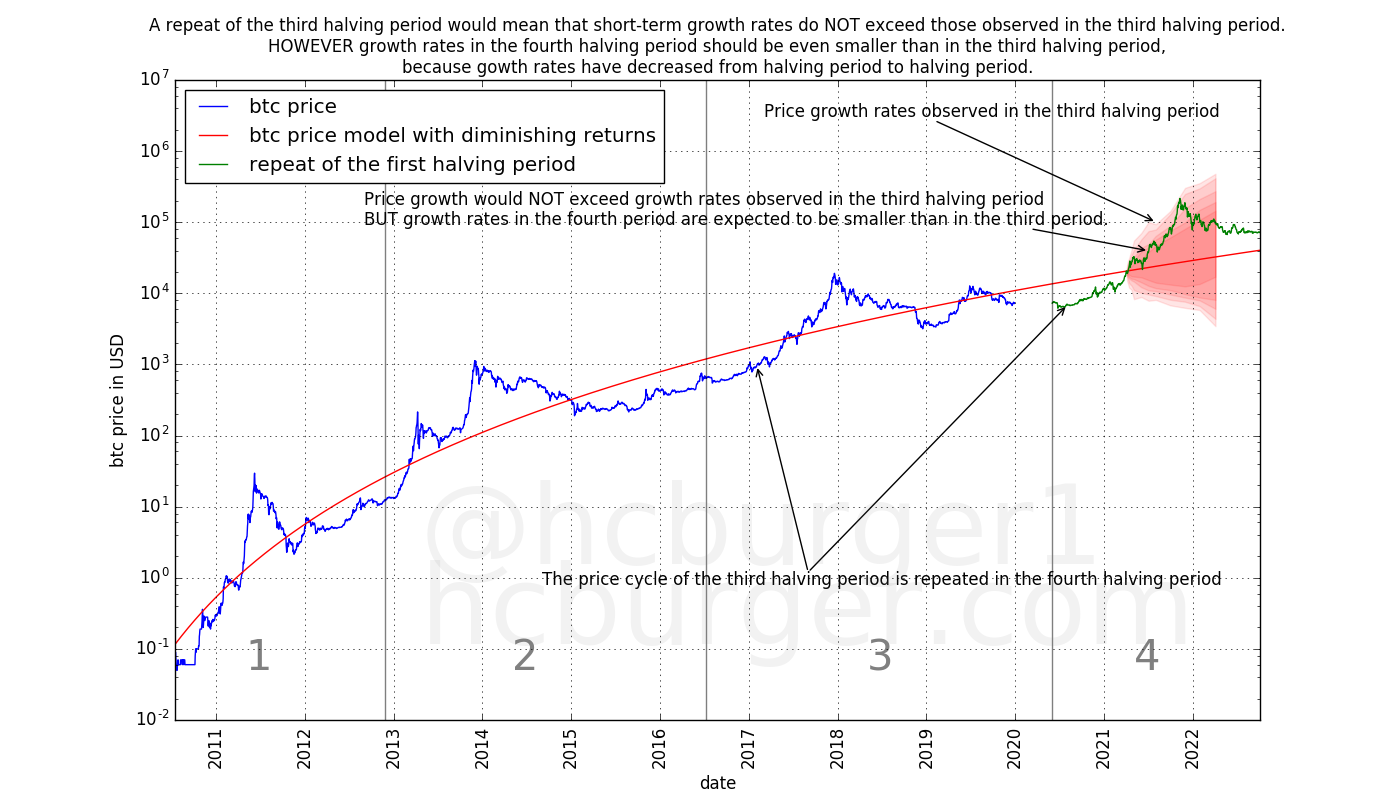

Would a repeat of the third halving cycle be possible? The below plot shows that the price movements are (obviously) in agreement with the statistics observed in the third halving period.

However, short-term price movement statistics should be tamer in the fourth halving period than in the third, for the same reason as statistics in the third period are tamer than in the second period.

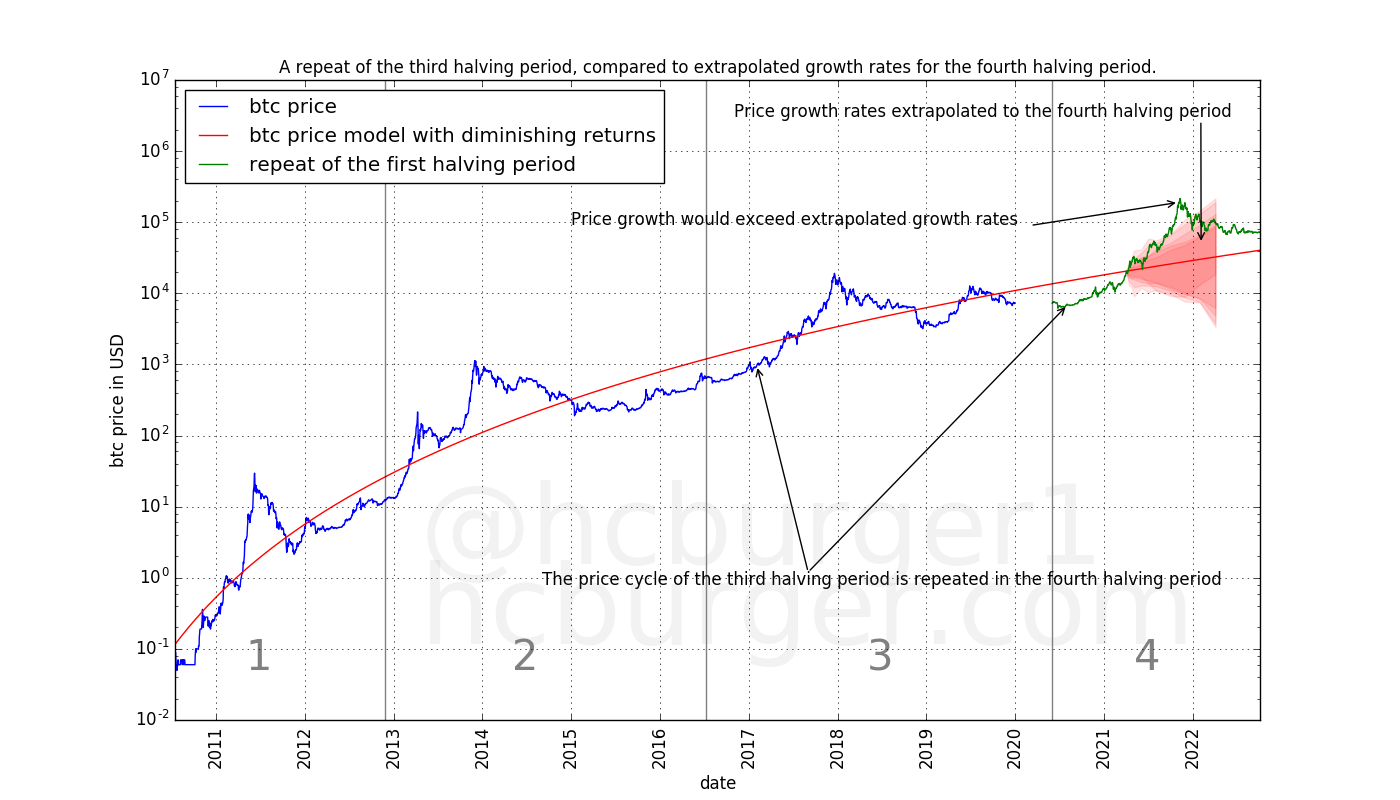

We will use a simple method to obtain extrapolated statistics for the fourth halving period, and compare the price movements of the third halving period to those statistics. The extrapolation method works as follows. For a given statistic, it computes the reduction factors from: 1) the first halving period to the second halving period and 2) the second to the third halving period. This average factor is then used to extrapolate the statistic from the third halving period to the fourth.

Using this extrapolation method, the price movements of the third halving period would be too extreme.

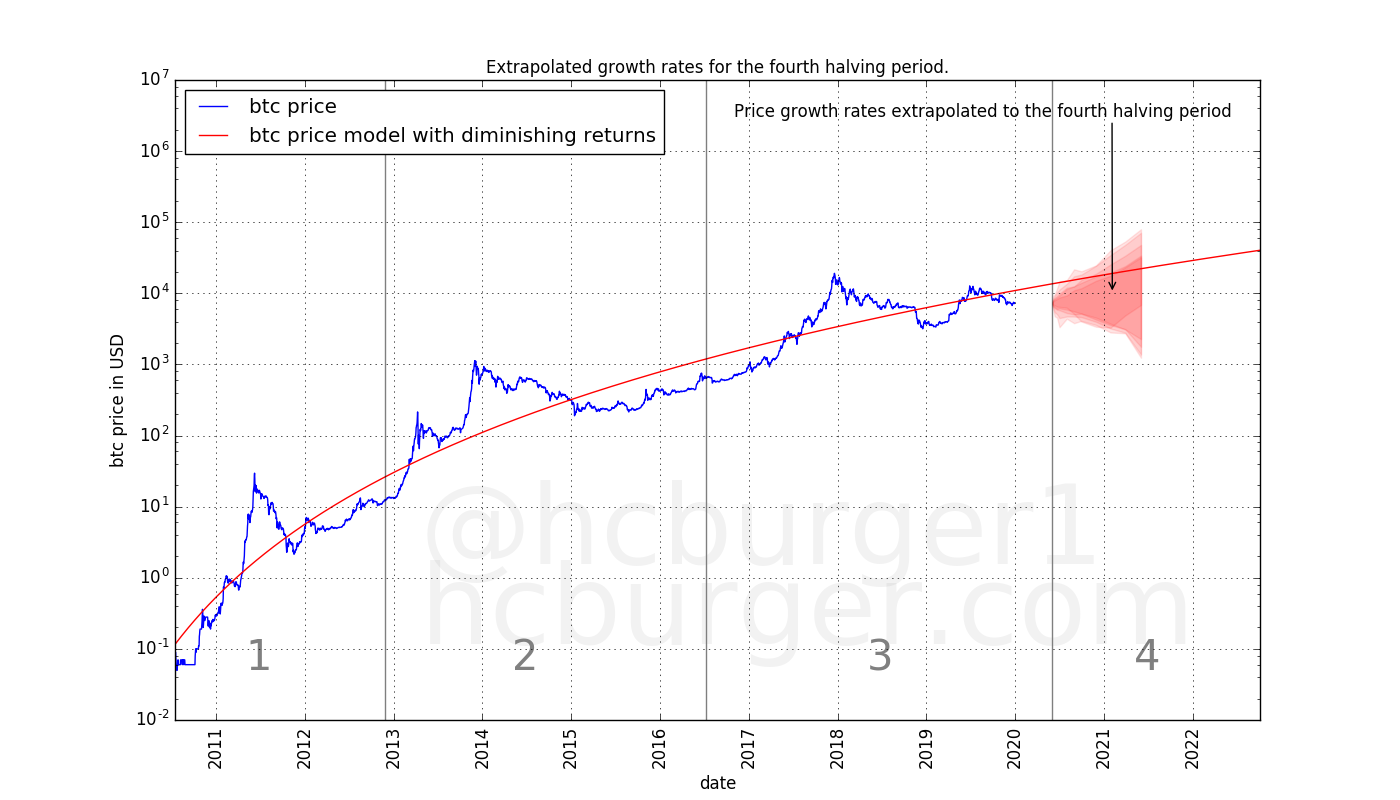

Assuming 0 price growth until the third halving, and using extrapolated statistics for the fourth halving period, we get the following possible price movements.

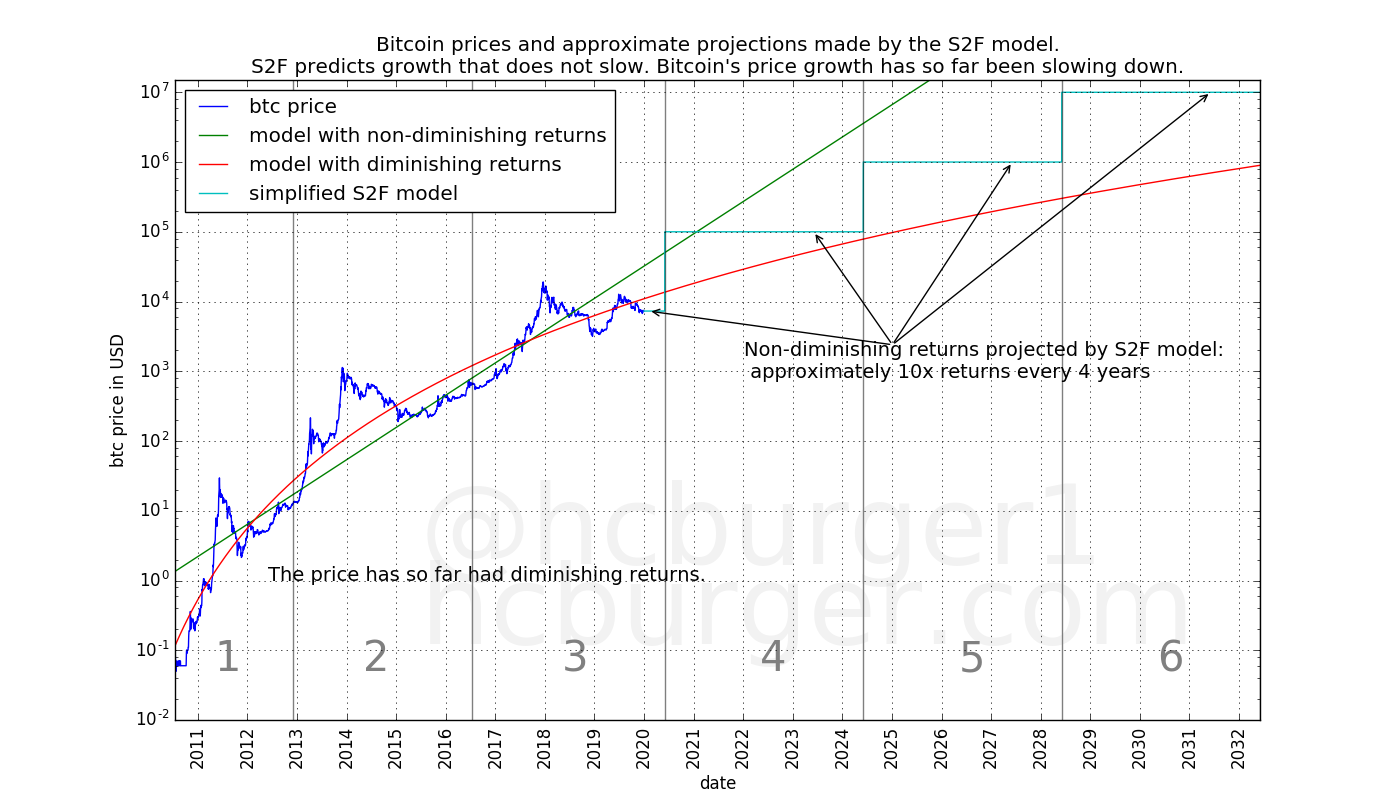

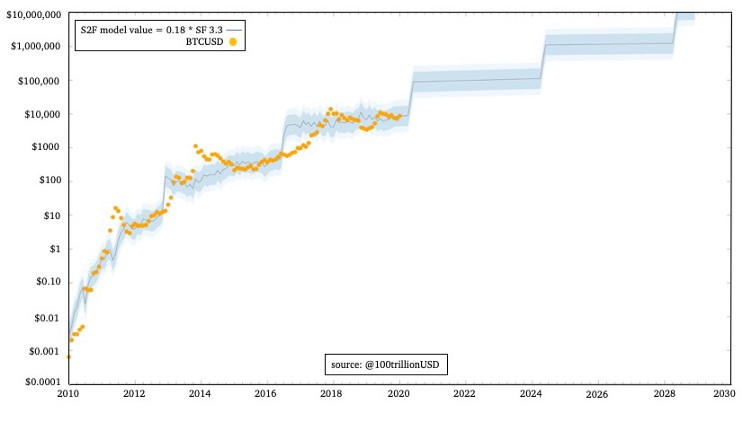

Stock-to-Flow model

A model proposed by planB called the stock-to-flow model (S2F for short) models the price of bitcoin using its scarcity, defined as the newly created stock divided by the already existing stock. Price predictions made by this model predict prices in the $100k range for the next halving period, with prices increasing approximately by a factor of 10 for each subsequent halving period:

for a given period of time (here: 4 years), is a model with non-diminishing returns. Such a model therefore makes claims about the future that are opposed to the observations of long-term diminishing returns we have made in this article, and the expectation expressed in this article that the trend of diminishing returns should continue.

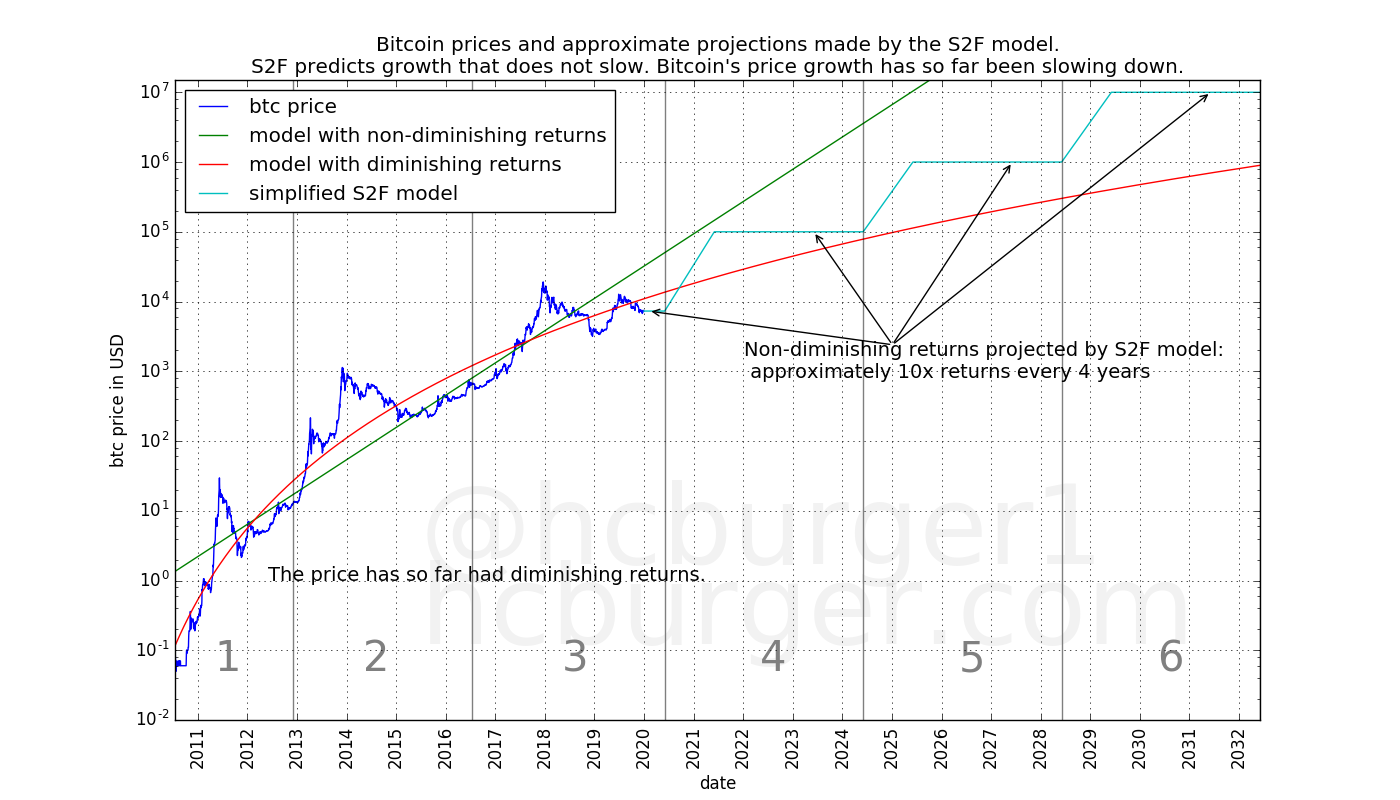

In the short-term, we should not expect the price to move in a step-wise function as displayed by the cyan line (nor does the S2F model claim that the price should evolve in such an abrupt manner). As an experiment, let us consider the following smoother hypothetical future price curve:

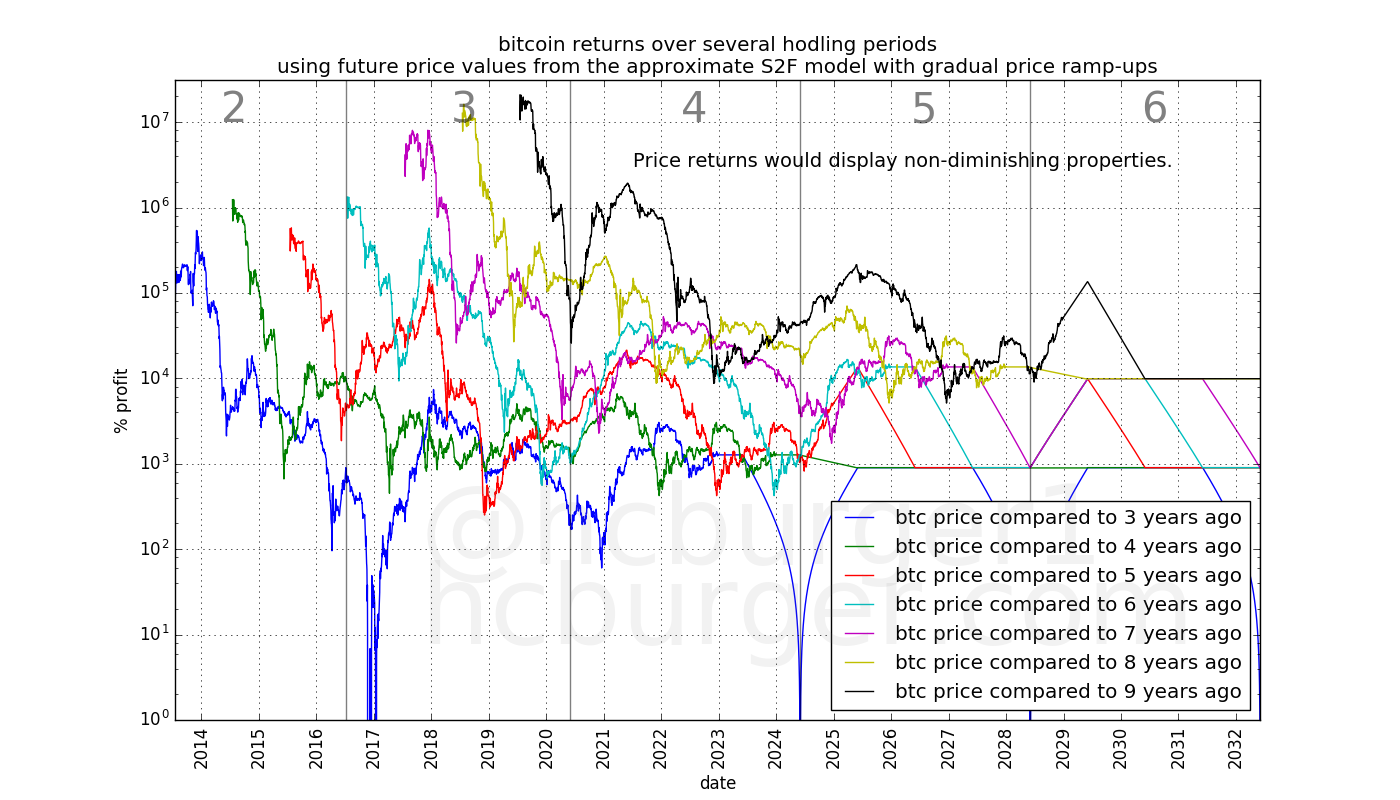

Looking at the return curves that such a price curve would generate, we see that returns at the beginning of the future halving periods (4, 5, and 6) tend to increase. Increasing returns can happen, due to volatility in the price, but should not be expected to happen systematically. We also see that returns for e.g. the three- and four-year hodling periods are more or less flat, at 1000%, reflecting the 10x price increase between halving periods predicted by the S2F model.

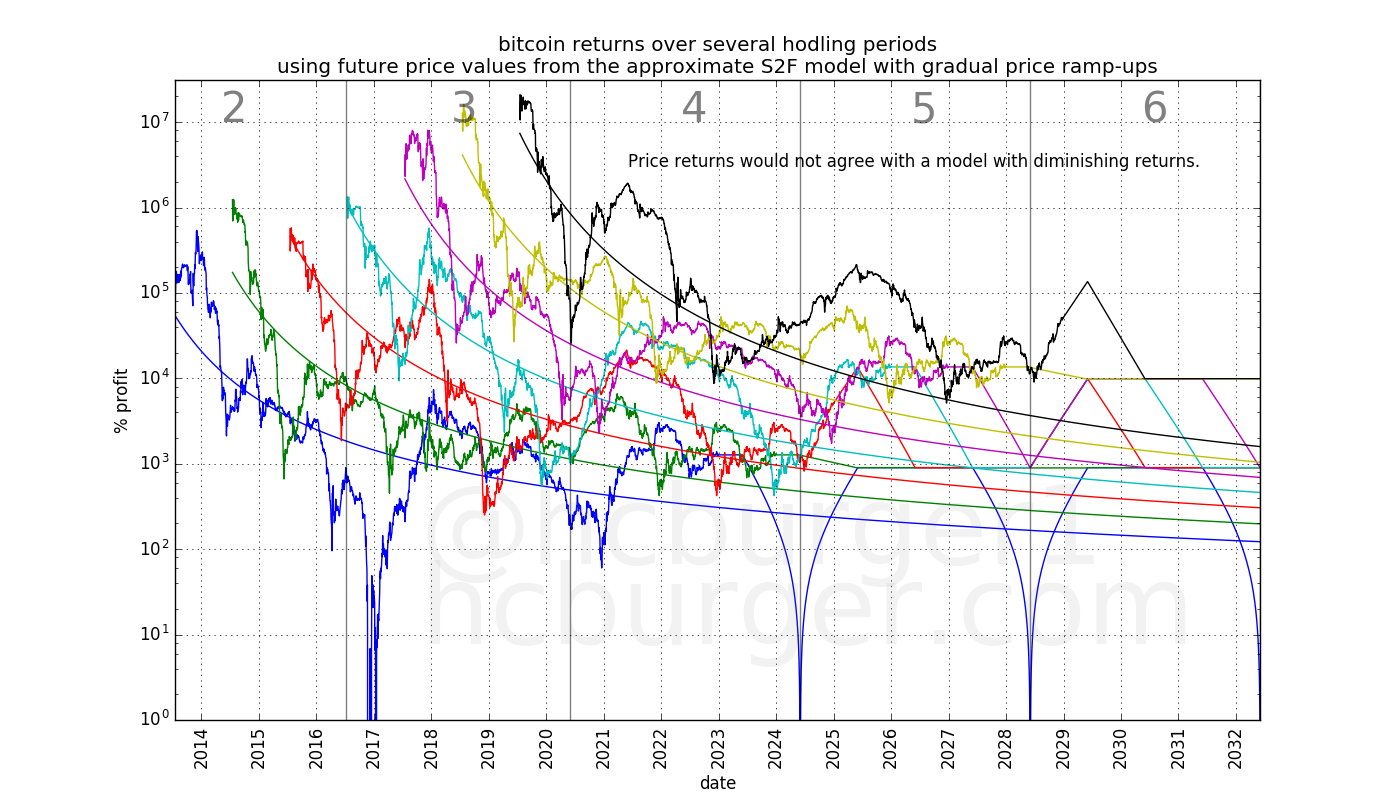

Overlaying the return curves generated by the model with diminishing returns shows these disagreements more clearly:

- The S2F model has return curves that are partially increasing, which is not expected in the model with diminishing returns

- The S2F model has return curves that are mostly flat for shorter hodling periods, which indicates non-diminishing returns, whereas in this article we have observed historically diminishing returns.

This is not a statement that the S2F model is incorrect, but it does show that for the S2F model to hold as currently formulated, return curves need to change compared to how they have behaved up to now: they need to transition from being diminishing to being non-diminishing.

Also, it is not quite correct to say that the S2F model has non-diminishing returns: In the early history, returns as modeled by the S2F model are indeed diminishing. The returns only diminish up to a certain point, though (approximately a 10x return every 4 years).

The future is still bright

Even though diminishing returns lead to predictions that are less optimistic than predictions based on non-diminishing returns, bitcoin can still have very strong growth for many years to come, and continue to outperform most traditional assets.

Discussion

What this article does not state

This article has made no numerical predictions. No predictions are made regarding the rate of decrease of the long-term price growth rate. Also, no prediction has been made regarding how much volatility is expected to decrease in the future. No statement has been made regarding whether both should tend toward 0 or not.

Potential counter-arguments

Bitcoin’s price growth has at various times been described as being either:

- constant,

- accelerating, or

- resembling an S-curve.

We see no empirical evidence for any of the above. Bitcoin’s price growth has been diminishing from the start.

Why would this property not hold anymore? One might argue that past performance is not an indication of future performance, and therefore that the fact that bitcoin’s returns have so far been diminishing does not mean that they will continue to be diminishing in the future. In other words: bitcoin’s returns could become non-diminishing in the future. As arguments against this statement we can say that:

- We have so far seen no sign that bitcoin is starting to show non-diminishing returns.

- A new, as of yet unknown, mechanism would need to take hold in order to counteract the fact that it becomes ever more difficult to attract ever more capital.

Reasons for slowing growth

We have stated that an increased price of bitcoin leads to more capital being required for even more price increases. We took a shortcut in that explanation: What matters is not only the price, but also the number of bitcoins traded. If few bitcoins are traded, other things being equal, the price of these bitcoins is easier to change than if many bitcoins are traded. One could therefore say that the depth of orderbooks (in fiat terms) really matters, rather than the price itself. So far, orderbook depth has increased along with price.

An alternative way of looking at diminishing returns is the following. The price of bitcoin depends on supply and demand, like anything else. The supply is driven by the willingness of hodlers to part with their bitcoin for a given price. Initial investors were unwilling to part with their bitcoin for anything less than very high returns. These initial sky-high returns attracted more investors, some of which are willing to part with their bitcoins for lower returns (“good enough” returns).

Mathematically, bitcoin’s price growth does not display memorylessness. Memoryless growth would mean that price growth does not depend on its price, which would mean non-diminishing growth. Memoryless/non-diminishing growth would be very surprising, as it would mean that bitcoin’s price has no effect at all on its expected growth rate. We should therefore not expect non-diminishing returns in bitcoin’s price growth, nor do we observe it empirically.

It is also not clear if higher price / deeper orderbooks is the only factor reducing price volatility in the short term. Another reason for reduced volatility might simply be time itself: as time goes by, traders find more and more profitably exploitable patterns. Exploiting these patterns leads to reduced volatility. Yet another reason might be the number of bitcoin traders. The more traders attempt to exploit patterns, the more stable the price is expected to be.

Conclusion

Bitcoin’s price has faced increasing resistance when moving upwards, leading to diminishing returns. Long-term, the price has grown slower and slower. Short-term, volatility has decreased, and bull markets have taken longer to develop and pop. These observations agree with the logic that as the price of bitcoin increases, price movements require ever more capital. For this reason, these two trends are expected to continue in the future. If these trends continue into the future, it will invalidate predictions and models that are based on expectations of non-diminishing returns, which will prove to be too optimistic.

Disclaimer: This article is not financial advice.

Related work / Prior art

I am deeply grateful, and also apologetic, to dave the wave, for pointing out to me that he observed both long- and short- term diminishing growth patterns in bitcoin for more than a year.

In a first article, Dave noted:

“As Bitcoin becomes more liquid, it becomes less volatile. Given the principle of the growth curve, this increasing price stability should incrementally come into fruition, with subsequent cycles, as the real volatility of those cycles diminish. These subsequent cycles also see the law of diminishing returns coming into effect though at this relatively early stage of the curve, future returns are projected to remain on quite a different scale to that of traditional asset classes.”

In a later article, Dave noted:

“And this is something you’d expect in a maturing, more liquid market — the general principle being that with more liquidity, comes less volatility. Also predictable, on the basis of the log growth curve model, is a longer base than previously — not only is volatility in the medium term reducing [hence a less volatile base], but so too is volatility reducing on the over-all long-term macro chart of Bitcoin.”

The similarities in the conclusions in Dave’s and this article are striking.

Acknowledgements

This article was inspired by two independent discussions I had. Once with BitcoinEcon, who was pondering whether future bull markets might span longer timeframes than previous ones. This discussion led me to the idea of inspecting short-term growth rates in the various halving cycles. The other with InTheLoop, in which we were discussing how much faith one can really put into any predictive model. This led me to the idea of seeing how far we can go without any model.

Thanks IntheLoop and BitcoinEcon for the great discussions!

Slice The Pie

By 6102

Posted January 1, 2020

What even is orange pie? This dumb tweet inspired this short article…

“The carpenter can’t run out of inches The stadium can’t run out of points The airline can’t run out of FF miles And the USA can’t run out of dollar” - Stephanie Kelton

Understanding

There is a common belief that the USA can just print as much money as it wants. Ignoring the complex nature in which money is actually created (debt, treasury notes etc) this is true, the USA can print as many dollars as it likes.

Misunderstanding

This is completely misunderstood by many to mean that the USA can buy anything it likes. This is categorically false. This misunderstanding comes from the fact that an individual acquiring more dollars sees his buying power increase, because those dollars come from his peers, and thus their loss is his gain. He does not increase the supply of dollars, he increases his holding of dollars. In contrast, when a country prints more dollars it is simply increasing the supply of dollars. This does nothing to increase the buying power of the country. As a result of this misunderstanding, many people mistakenly believe that the USA can’t default on its debts.

“This is the United States Government … you never have to default because you print the money. “ - Trump

“The United States can pay any debt it has because we can always print more money to do that so there is zero probability of default.” - Greenspan

Why doesn’t printing money help?

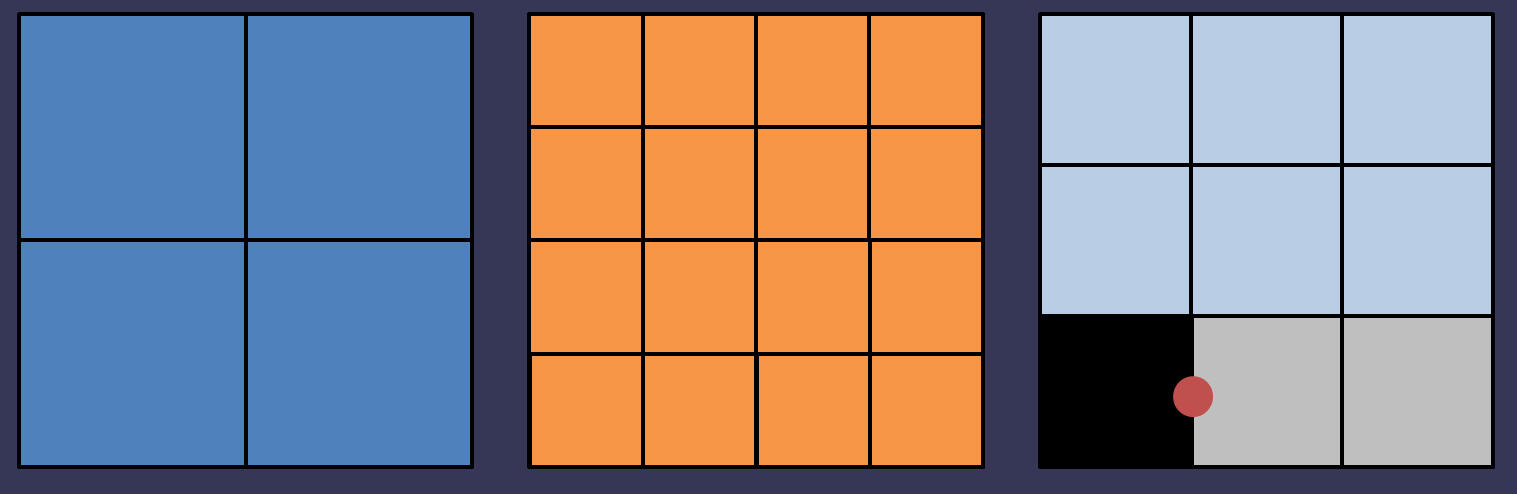

| Money is a tool used to measure value. Like any useful measuring tool it should be reliable, if all else is constant then measuring the same thing twice should yield the same result twice. Increasing the money supply effectively distorts the measuring tool. If you double the money supply then you will simply half the value of each unit of money. Consider two pies, Blue(berry) Pie | Orange Pie (wtf) |

Blue(berry) pie is split into 4 equal slices, while Orange pie is split into 16.

Assuming that both pies are equally delicious (this is unlikely, apologies to any orange pie lovers) what is the relative value of a slice of blueberry pie to a slice of orange pie? 4:1 (A slice of blueberry pie is equivalent to 4 slices of orange pie) Money is equivalent to the number of slices of the pie. You can slice the pie into more pieces, but the value of each slice will be worth less. To complicate matters, governments have a tendency to continue slicing the pie while you are holding it! They call it ‘inflation’.

Remember, Money is a tool used to measure value. Like any good measuring tool it should be reliable, if all else is constant measuring the same thing twice should yield the same result twice. Inflation breaks the reliability of money. A dollar 50 years ago would get you a whole lot more than a dollar today. That is because the value of the dollar has decreased, and it has done so due to inflation (printing more money). Consider the policy of those who slice the pie you hold pieces of.

An Introduction to the Efficient Market Hypothesis for Bitcoiners

What the EMH does and does not say

By Nic Carter

Posted January 4, 2020

Curbstone brokerage on Broad Street in Manhattan, 1902 (Public domain image from the United States Library of Congress)

As we approach the Bitcoin halving due in May 2020, a heated debate has raged among Bitcoiners about whether the issuance change is being anticipated by the market or not. Those who downplay the purported impact of the issuance change tend to make references to market efficiency. This concept has thus become a source of great rancor and debate. The disagreements are often intractable, as strawman versions of the EMH are presented, and the parties cannot converge on shared definitions. Mutually understood concepts are a prerequisite to a useful debate. Since the concept is widely misunderstood, I thought I’d explain it from scratch, assuming little prior financial knowledge.

Origins of the EMH

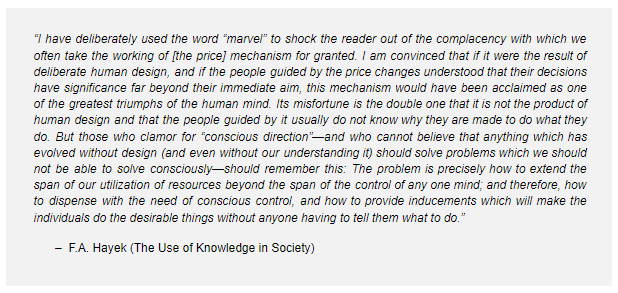

The efficient market hypothesis has been attributed to several thinkers, among them Benoit Mandlebröt, Louis Bachelier, Friedrich Hayek, and Paul Samuelson. Hayek’s The Use of Knowledge in Society is useful background reading for the concept, although it never makes reference to the EMH specifically. His seminal essay argues in favor of distributed, market-based economies, in contrast to centrally planned ones. The key insight: markets are information-aggregation mechanisms that no central planner, no matter how skilled or well-resourced, can match. Consider the following passage (emphasis my own):

[T]here is beyond question a body of very important but unorganized knowledge which cannot possibly be called scientific in the sense of knowledge of general rules: the knowledge of the particular circumstances of time and place. It is with respect to this that practically every individual has some advantage over all others because he possesses unique information of which beneficial use might be made, but of which use can be made only if the decisions depending on it are left to him or are made with his active coöperation.

[…] And the shipper who earns his living from using otherwise empty or half-filled journeys of tramp-steamers, or the estate agent whose whole knowledge is almost exclusively one of temporary opportunities, or the arbitrageur who gains from local differences of commodity prices, are all performing eminently useful functions based on special knowledge of circumstances of the fleeting moment not known to others.

In the bolded section you can begin to see how Hayek views markets: as forces that aggregate a multitude of different views and expectations into prices. Hayek understands market-derived prices as information — a particularly high signal source of information at that. The beauty of markets, to Hayek, is that simply by selfishly acting according to their own interests, individuals participating in the economy create signals in the form of prices. The EMH orients this perspective specifically towards financial assets, holding that investors collectively surface relevant information which is incorporated into prices through the mechanism of trades.

Following a series of studies about stock returns like Samuelson’s 1965 Proof that Properly Anticipated Prices Fluctuate Randomly, the EMH was finally codified for good in 1970 by legendary finance academic Eugene Fama (you may have heard of the Fama-French model). In a paper entitled Efficient Capital Markets: A Review of Theory and Empirical Work, Fama defines an efficient market as “a market in which prices always “fully reflect” available information.” If you were stop reading here, you’d already have a better understanding of what is meant by efficient markets than the caricatures presented on Twitter. The EMH is not a mystical claim. It’s simply the view that market prices reflect available information. This is why academics often refer to them as ‘informationally’ efficient markets. The efficiency refers to information proliferation.

What does this actually mean? It simply means that if there is new information which is relevant to the asset being traded, this information tends to be incorporated into the price of that asset with rapidity. And if there are future events which you might reasonably imagine would affect price, they tend to be incorporated into the price when known. Markets don’t wait for (knowable) events to happen — they anticipate them. This means, if a weather forecast predicts that a hurricane will emerge and wipe out sugarcane plantations next week, speculators will bid up the price of sugar today, anticipating the supply shock. Now, of course, when there are unpredictable exogenous shocks (imagine that the hurricane materialized with no warning), then price can only react in real time, as the information becomes known. The speed of information incorporation is one of the tests of efficiency.

While the EMH is a simple idea, it tells us a great deal about how markets operate. Markets are efficient if prices rapidly incorporate new information. Forecastable, market-moving events taking place in the future tend to be incorporated in price beforehand. Importantly, one consequence of the EMH is that, once all relevant information is incorporated into price, you are left with only random fluctuations, called ‘noise’. What this means is that while asset prices will still jitter about, even in the presence of no new fundamental information, these fluctuations contain no information of their own.

And lastly, the difficulty of surfacing unique new information (not already included in price) tends to vary with the sophistication of market participants and the liquidity of the asset. This explains why you might be able to find an edge in an obscure micro cap stock, but probably not in predicting the price of Apple.

Since Fama’s paper, and thanks to popular books on the topic like Burton Malkiel’s A Random Walk Down Wall Street, a heated debate has raged over whether active management is worth it. Indeed, since efficient markets posit that consistent edges are very difficult to find, many investors have come to question whether actively traded vehicles like hedge and mutual funds make sense. In the last decade, trillions of dollars have flowed out of such ‘active,’ stock-picking strategies, and into passive vehicles, which simply seek to track the performance of the entire market, or a specific sector. This is one of the most critical debates happening in finance right now, and it’s mostly due to the growing realization that markets are, indeed, generally efficient.

The EMH described

I take slight exception to the ‘hypothesis’ component of the EMH. If it were up to me, I’d call it the efficient markets model, not hypothesis. This is because it doesn’t really contain a hypothesis. It doesn’t really make a specific testable claim about the world. As stated, the EMH posits that market prices reflect available information (which, as we have noted, is the purpose of markets in the first place). Interestingly, Fama in his 1970 paper calls it the efficient market model, not hypothesis. It seems he has the same intuition.

I would also go as far as to consider EMH somewhat tautological. Recalling Hayek, we know that (free) markets measure society’s net informational stance over various assets. So if we replace ‘market prices’ with ‘concentrated information outputs’ in the EMH construction bolded above, we get the following:

Concentrated information outputs reflect available information

That certainly sounds tautological. But that doesn’t make the model any less useful_._ Conversely, it means that contesting the EMH is to question the nature of markets themselves. And indeed, most critiques of the EMH (I will cover a few later in this piece) generally cover instances where markets are not clearing, for some reason or other. So if you accept that EMH is tautological, ‘efficient markets’ also starts to sound redundant. Indeed, the default state of (free) markets is to be efficient, because this is why we have markets. Markets compensate anyone for finding relevant information. If they weren’t default-efficient, then we wouldn’t bother with them.

Referring to it as a model makes it very clear that it’s just an abstraction of the world, a description of the way markets should (and generally do) work, but by no means an iron law. It’s just a useful way to think about markets.

Let me be clear! I do not believe in the “strong form” of the EMH. No finance professional I know does. It is generally a straw man. The strong form holds that markets reflect all information, all the time. If this were true, no hedge funds or active managers would exist. No one would bother poring over Apple’s quarterly reports, or evaluating the prospects for oil discovery in the Permian basin. Clearly, given that we have a large active asset management industry, in which lots of very bright individuals constantly seek to surface new information about various assets, the strong form doesn’t hold.

Truthfully, the EMH is not something you ‘believe in,’ or not. The choice is to understand markets as useful information-discovery mechanisms, or reject the usefulness of markets altogether.

There are of course conditions which lead to market inefficiency. Fama acknowledges as much in his 1970 paper, calling out transaction costs, the costs of acquiring relevant information, and disagreement among investors as potential impairments to market efficiency. I’ll discuss two here: the costs of surfacing material information, and frictions inherent in actually expressing market views.

If the EMH generally holds, how are funds compensated for finding information?

So what explains the fact that there is a large (albeit shrinking) industry involved in active investing, despite the fact that markets are generally efficient? If market-relevant information is generally encoded in prices, then there is no profit from finding new information and trading against it. But clearly, many individuals and firms do actively attempt to surface new information. This presents a bit of a paradox.

This brings us to another one of my favorite papers, On the Impossibility of Efficient Markets, by Grossman and Stiglitz. The authors point out that gathering information is costly, not free. They then note that since EMH posits that all information is immediately expressed in prices, there would be no compensation from incurring costs to surface new information under that model. Thus markets cannot be perfectly efficient: information asymmetries must exist, as there must be a way to compensate informed traders. Their model introduces the useful variable of information cost into the standard model of market efficiency. It follows from their model that if information becomes more costly, markets become less efficient, and vice versa. So whether or not markets reflect their fundamentals is at least partially a function of the difficulty of surfacing that relevant information.

The authors conclude:

We have argued that because information is costly, prices cannot perfectly reflect the information which is available, since if it did, those who spent resources to obtain it would receive no compensation. There is a fundamental conflict between the efficiency with which markets spread information and the incentives to acquire information.

A rather delightful implication of Grossman and Stiglitz is that, to render arbitraging prices back to where they ‘should’ be a profitable activity, there has to be a cohort of traders who are perennially knocking prices out of whack. Fischer Black (he of the Black Scholes formula) gives us an answer, with a lovely paper pithily entitled Noise in the Journal of Finance. He identifies unsophisticated ‘noise’ traders: those who trade on noise, rather than information. Noise can be found anywhere. Just mosey on to Tradingview and see the plethora of indicators that people swear by. Black divides market players into two cohorts:

People who trade on noise are willing to trade even though from an objective point of view they would be better off not trading. Perhaps they think the noise they are trading on is information. Or perhaps they just like to trade.

With a lot of noise traders in the market, it now pays for those with information to trade. Most of the time, the noise traders as a group will lose money by trading, while information traders as a group will make money.

Noise, in Black’s view, “makes financial markets possible.” The existence of noise traders gives professional firms like hedge funds liquidity, and valuable counterparts to trade against. In the poker analogy, noise traders are the fish. They make the game profitable for the sharks, even in the presence of a rake. Ask any former online poker player — as the scene became more competitive, and unsophisticated players left, it stopped being as profitable to play.

The noise theory resolves the ‘apparent impossibility’ of efficient markets as pointed out by Grossman and Stiglitz. The existence of noise as introduced by unsophisticated traders gives sophisticated traders a considerable financial incentive to introduce information into prices. So you can thank the degens overtrading on Bitmex — they are the ones compensating funds for allocating resources to Bitcoin and surfacing relevant information quickly.

If the EMH generally holds, how do you explain instances where markets do not clear?

This is another good question. There are copious examples of situations where arbitrage opportunities were easy to identify, yet where the arbitrage could not be closed for some reason. The most famous of these examples is arguably the trade which caused the demise of Long Term Capital Management. It was a pair trade on bonds which were effectively identical but were differently priced (partially due to the Russian default in 1998). LTCM was betting that the prices of the bonds would converge. However, many other hedge funds had made that same bet with leverage, and as the bonds failed to converge in a timely manner, LPs in some of the hedge funds redeemed, the funds faced margin calls, and were thus forced to liquidate this positions. This kicked off a feedback loop causing additional squeezes: the cheaper bonds were sold off, and the pricier instruments kept rallying as shorts were covered. LTCM was betting on market efficiency and the convergence of these instruments; but because of market stress and the winding down of pent-up leverage, they weren’t able to complete the trade, and the fund blew up.

This phenomenon is examined in a 1997 paper from Shleifer and Vishny entitled The Limits of Arbitrage. Shleifer and Vishny point out that arbitrage is not normally done by the market, generically, but rather is a task delegated to specialized institutions (funds, typically). As such, arbitrage is costly: requiring freely available capital. There’s a paradox: great arbitrage opportunities come about when the market is under stress (this is when you get many stocks trading at a low price-to-book, for instance). But during times of market stress, capital is least available. Thus the arbitrageurs, who require capital to operate, are worst equipped to perform the required arbitrage when they are most needed. These are the limits of arbitrage. As the authors state:

When arbitrage requires capital, arbitrageurs can become most constrained when they have the best opportunities, i.e., when the mispricing they have bet against gets even worse. Moreover, the fear of this scenario would make them more cautious when they put on their initial trades, and hence less effective in bringing about market efficiency.

Take the simple example of a value-based hedge fund which has raised outside capital. They will tell LPs (investors in the hedge fund) of their intention to pursue contrarian bets — buying value stocks when they are cheap, for instance. Let’s say the market declines and they buy a basket of stocks whose valuations have contracted and have low P/E ratios. However, imagine that the market subsequently declines another 40%. Their LPs are now staring at a loss and ask to redeem. This is the worst possible time: the fund has to sell the stocks at a loss, even if they have a high conviction on making money on them in the long term. They would much rather be buying the (now very discounted) stocks, whose valuations are even more attractive. To make things worse, liquidating those positions forces them down further, punishing other funds making the same trade.

Shleifer and Vishny therefore find that:

[P]erformance‐based arbitrage is particularly ineffective in extreme circumstances, where prices are significantly out of line and arbitrageurs are fully invested. In these circumstances, arbitrageurs might bail out of the market when their participation is most needed.

The limits to arbitrage caveat about EMH actually explains a lot of situations where people will describe market conditions and lament that information is not being incorporated. This is often taken as a slight against the EMH. But of course we cannot expect malfunctioning markets to operate properly. So when Dentacoin’s multi-billion dollar putative market cap is touted as an example of market efficiency not holding, consider that it likely had a minuscule float, ownership was extremely concentrated, and obtaining a borrow for a short was impossible. This means that market participants cannot meaningfully express their views on the asset.

A fuller conception

Mindful of these constraints (issues of market structure, costly information, limits to arbitrage), we can devise a more complete version of the EMH which includes these caveats. You might therefore devise a modified EMH that sounds a bit like this:

Free markets reflect available information to the extent that price-setting entities are willing and mechanically able to act upon it.

- Free markets: because state-controlled markets may not clear (for instance, markets for currencies with capital controls do not give reliable signals, since selling is effectively constrained)

- Price-setting entities: because minnows don’t ultimately matter most of the time. A small number of well-capitalized participants can suffice to incorporate material information into price

- To the extent that they are willing: this covers the ‘costly information’ caveat. If information is more costly to obtain than it is worth to instrumentalize (for instance, in the case of discovering accounting fraud in a micro-cap stock), then it won’t be included in price

- Mechanically able: this covers cases where limits to arbitrage exist. If there is a liquidity crisis, or the markets are not functioning properly, for whatever reason, and funds cannot operationalize their views on the market, inefficiency may occur

So when most financial professionals talk about the EMH, they generally imply a modified, slightly caveated version like the one above. Almost never do they mean the ‘strong form’ of the EMH.

Interestingly, by caveating the EMH, we have stumbled on an alternative conception entirely. The model I have described here somewhat resembles Andrew Lo’s adaptive market hypothesis. Indeed, while I am very happy to maintain that most (liquid) markets are efficient, most of the time, the adaptive market model far more closely captures my views on the markets than any of the generic EMH formulations. Many active managers that I know are at least familiar with Lo’s work. The theory is fully developed in his book, but you can get a condensed version in his 2004 paper.

In short, Lo attempts to harmonize findings from behavioral economics finding apparent irrationality on the part of investors, with the orthodox EMH school. He calls it the adaptive market hypothesis because he relies on an evolutionary approach to markets. Taking Black’s insight further, Lo divides market participants into ‘species’, giving us a view of market efficiency which departs from the mainstream:

Prices reflect as much information as dictated by the combination of environmental conditions and the number and nature of “species” in the economy or, to use the appropriate biological term, the ecology.

Lo describes profit opportunities from information asymmetries as ‘resources’, leading to formulations like the following:

If multiple species (or the members of a single highly populous species) are competing for rather scarce resources within a single market, that market is likely to be highly efficient, e.g., the market for 10-Year US Treasury Notes, which reflects most relevant information very quickly indeed. If, on the other hand, a small number of species are competing for rather abundant resources in a given market, that market will be less efficient, e.g., the market for oil paintings from the Italian Renaissance.

The contextualism and pragmatism that Lo’s model presents aligns it with the experience of most traders, who intuitively understand that market participants are quite heterogeneous, and understand the notion of ‘table selection’ (borrowed from poker). I won’t dive too deep into Lo’s take here, but I do recommend his book, and at the very least his paper summarizing his theory.

What this means for Bitcoin and the halving

As we have seen, most markets are efficient most of the time. This is not something markets just happen to do; this is their purpose. I have discussed a few exceptions: the limits to arbitrage situation, non-free market situations, situations where behavioral biases apply, and situations where market participants may not be sufficiently motivated to surface relevant information. The question is, do any of these conditions apply to the Bitcoin markets? Right now, this doesn’t seem to be the case. We are not in a liquidity crunch. There are no apparent limits to arbitrage. In the pre-financialized era for Bitcoin (I’d say anytime before 2015), you could have convincingly made that case. There truly was no easy way for a well-capitalized entity to express as positive view on Bitcoin. But today there is.

As for free markets, Bitcoin is clearly a very free market, one of the freest on earth (since the asset itself is highly portable and easily concealable, and traded around the globe). Unlike most currencies, it is not backed or guaranteed by a sovereign, and there are no capital controls impairing selling. Participants also have the abundant ability to place large short positions on Bitcoin, so they can express a diverse set of views. So we can check the ‘functioning markets box’. Now, is Bitcoin sufficiently large for there to be a significant number of sophisticated funds devoting concerted effort to surfacing material information? At a $150b market cap, I think that’s absolutely the case. The final test of market efficiency is whether or not market-moving information is incorporated into prices right away, or with a lag. An event study covering the effect of exogenous shocks like exchange hacks or sudden regulatory shifts on price would be welcome.

The only necessary conditions for efficiency for which Bitcoin still has question marks have to do with disagreement among market participants (i.e. the lack of a shared valuation model that price setting entities converge on), and the development of more financial plumbing. There are still a few classes of entity for which Bitcoin exposure is rather difficult to obtain. Of course, surmounting these challenges will render Bitcoin’s prospects sunnier.

So is the halving “priced in” or will it be a catalyst for appreciation? If you’ve read this far, you will understand that I consider it patently absurd that a change in issuance would have been overlooked by the price-setting entities. Anyone with an interest in Bitcoin has been aware of the supply trajectory from inception. Supply was encoded in the very first implementation that Satoshi released to the world in January 2009. Long-scheduled changes in the rate of issuance do not constitute new information. Any presumed demand-side reactions to the ‘halving catalyst’ can also be anticipated by sophisticated funds who have a strong incentive to frontrun investor optimism.

Now, can Bitcoin appreciate from here onwards? Absolutely. I don’t believe appreciation, if it occurs, will be due to the entirely foreseeable changes in the rate of issuance (the forthcoming halving will take us from 3.6% to 1.8% annualized issuance), but of course I feel that there are other factors which could positively affect the price, most of which are hard to predict. Is that consistent with the EMH? Very much so. EMH permits informational shocks (for instance, imagine if we suddenly had rampant inflation in a major world currency). It’s also possible that the price setting entities are taking an overly conservative view of Bitcoin’s future, or that they are acting on a weak fundamental model. These are consistent with weak form EMH.

I’ll leave you with this parting thought. Regulated securities markets have structural barriers to efficiency in the form of prohibitions on insider trading. As Matt Levine likes to say, insider trading is a form of theft in which someone trades on information which does not belong to them. They have not discovered the information from public sources, but rather were privy to something like a merger discussion and acted on it. Since insider trading is banned, stock prices generally don’t reflect pending catalysts like acquisitions until they are publicly announced. However, in a market for a virtual commodity like Bitcoin, insider standards don’t typically apply. If a catastrophic bug is found, you can expect that this information might be incorporated into price right away. So in that sense, it’s quite possible that the market for Bitcoin is more informationally efficient than markets for U.S. equity are.

Common objections

I will consider some objections here. Odds are, your responses are covered.

I found an instance of inefficiency. This is evidence for the inefficiency of markets generally

This is a bit like throwing a baseball in the air and claiming that its temporary departure from the earth disproves gravity. Few or no finance practitioners believe that all markets are efficient all the time. If information is unevenly distributed, or information-owners lack the means to instrumentalize their views, then the prices may not reflect information. Short term instances in which markets do not apparently reflect information are just invitations to query why market participants were unable to price in relevant information. These failures aren’t evidence of the weakness of the EMH, but rather reinforce its usefulness as an explanatory tool.

Behavioral biases exist, so market efficiency doesn’t hold

A number of persistent behavioral biases have indeed been found by researchers, and I find it plausible that they systematically affect asset prices to an extent in the medium term. However the question here is whether they are relevant to the matter at hand — the putative effect of a change of the rate of supply on the price of the asset — and whether these purported biases can actually affect the price formation of a highly liquid $150b asset. You might respond: ‘well Bitcoiners have a bias which causes them to bid up the price of assets with sharply decreasing issuance rates, even if this information is already known.’ If you can prove, Kahneman and Tversky-style, that this is a universal human bias which affects asset pricing, and contradicts dominant market models, not only will you win the argument, but you will also likely collect a Nobel. In this situation I’d also refer you once again to Lo’s adaptive markets.

Efficiency is impossible in Bitcoin because there are no fundamentals

Some people hold that sentiment drives everything in crypto markets, and that fundamentals do not exist. This is a convenient fallacy. There are obvious fundamentals which everyone would agree matter. Here is a short, non-exhaustive list:

- the quality of financial infrastructure enabling individuals to get exposure to and hold Bitcoin. In 2010, it was virtually impossible to buy Bitcoin, and your only option for custody was the Bitcoin QT ‘Satoshi Client’ or a homebrewed paper wallet. Today, you can get a billion dollars of Bitcoin exposure, and you can self-custody it or rely on some of the world’s largest asset managers and custodians. This is a fundamental change

- the quality of the Bitcoin software (compare the current version with Satoshi’s first client). The protocol itself and the tooling surrounding it has been improved, refined, and made more useful

- the actual stability and functionality of the system — imagine a case where Bitcoin failed to produce blocks for a month. That would surely impair the price. If you concede this, you admit that there are ‘fundamentals’ beyond mere sentiment

- the number of individuals globally that are aware of and demand Bitcoin. This is ‘adoption’. This not mere sentiment; this is a measure of which sources of capital, worldwide, are actively seeking exposure to Bitcoin

There are many other fundamentals which I won’t cover here. Funds which trade Bitcoin seek to track the trajectory of these variables, and ascertain whether Bitcoin is too richly or modestly priced relative to their growth. This is “fundamental analysis”.

Again, if you aren’t persuaded, just think about the contrast between Bitcoin’s state in 2010 and its state in 2020. It’s many orders of magnitudes easier to use, acquire, buy, sell, and store. That is a change in fundamentals. Granted, these aren’t ‘fundamentals’ of the sort that apply to stocks with cash flows, but Bitcoin isn’t a stock. A unit of Bitcoin is a claim on ledger space which gives you access to the particular transactional utility of the network. I’ll concede that the fundamentals aren’t quite as explicit as those present in a stock. But, the notion of ‘fundamentals’ isn’t just restricted to equity or instruments with cashflows. Global macro investors consider currencies based on macro variables or assessments of political risk. Commodity traders look at production rates and the ebb and flow of supply. There are analogies here.

All of this to say that funds have meaningful market-relevant information to trade against, not just sentiment or hype. It’s just that it’s hard to obtain a precise fundamental assessment of Bitcoin.

Efficiency is impossible in Bitcoin because it is volatile

It’s entirely possible to have volatile and efficient markets. Recall that all efficiency requires is that available information is incorporated in price. Think about the value of a call option close to expiry, with the underlying fluctuating around the strike price. One minute the option is in the money, the next it is worthless. This would be both a volatile and efficient situation.

Alternatively, consider the value of Argentine government bonds in response to political turmoil. The fundamental here is the Argentine government’s willingness to honor their debts. Efficiently functioning markets would continuously reevaluate the prospects for creditors being repaid. In a period of flux the fundamental is volatile, and so too consequently is the value of the bonds.

Bitcoin’s volatility derives in part from market participants rapidly re-assessing its prospects growth, both in terms of pace and trajectory. Even small changes in future expectations of growth rates have significant effects on the implied present value. (Indeed, in DCF models for equity valuation, the outputs are very sensitive to long term growth rates.) Market participants revise their growth expectations frequently, and expectations differ (because there is no single dominant model of Bitcoin’s price), giving rise to the elevated volatility (especially against the backdrop of a inelastic supply). If future expectations of growth are the fundamental, then the rapid revaluation of those expectations creates consequent volatility in price. So volatility does not disqualify efficiency.

If the EMH were true, Bitcoin would have just started life at its current valuation

This isn’t how the world works. As I explained above, Bitcoin didn’t start life with mature, rock solid fundamentals like it presently has. It had to grow into its valuation. In its earliest days, there was considerable uncertainty over whether it would achieve any success whatsoever. It had to actually go through all these trials and tribulations to get to where it is today. So it wouldn’t have made sense for large funds to allocate to Bitcoin on day 1 (although, it clearly makes sense in hindsight), because they didn’t know it would grow, and in many cases, because they structurally couldn’t invest in it. Think about how you would have acquired Bitcoin in 2012, two years into its existence. You would have had to use something like Charlie Shrem’s BitInstant, or the (already insolvent) Mt Gox, which we know now was run shambolically. You could have mined Bitcoin, but this was a difficult and deeply technical task.

This returns us to the “limits to arbitrage” point. Many investors that wanted to buy Bitcoin from 2009 through to present day simply couldn’t, due to regulatory reasons, operational risks, and a lack of functional market infrastructure. Even if they did believe that Bitcoin would be worth north of $100b at some point, they wouldn’t have had the ability to instrumentalize that view. Moreover, investors didn’t start out with rock solid conviction. They needed to see Bitcoin work, successfully, in the wild, without being shut down, before choosing to store wealth in it. If you believe that Bitcoin’s continued success represents new information being brought to market, then you understand that the EMH does not require it emerging from the womb, fully formed, at an initial >$100b valuation.

Something which is influenced by ponzi-related buying like Plustoken cannot be efficient

I’d agree that investors in Plustoken buying (and then selling) about 200,000 BTC was a major driver of price action in 2019. However, this doesn’t impair efficiency. If it had been known in the West that Plustoken had all those coins, and were just about to sell them off, and the price of Bitcoin did not move, then I agree — there would have been questions about efficiency. However, it wasn’t until much later, after much of the coins had been sold off, that information percolated through the West about the Plustoken BTC. Remember, efficiency doesn’t require that prices never move; rather, it suggests that prices move on new information.

Small cap assets pump on by hundreds of percent on dubious news. This is evidence of market inefficiency and disproves the EMH

Again, local, or temporal evidence of perceived irrationality does not invalidate the EMH. You either believe markets are good information clearing mechanisms or you do not. Granted, many of these small cap altcoin markets are very poor, from a structural perspective. These assets may trade on unregulated or illiquid exchanges. This means the prices you see do not necessarily reflect reality. Thus temporary pumps and dumps in illiquid assets don’t prove much in either direction, aside from the poverty of the market environment in which they trade.

Generally speaking, most adherents to the EMH will concede that efficiency varies positively with the size of the asset and the sophistication of the participants. It will be very hard to find an edge in large, publicly traded stocks. Odds are, if you find some market-relevant information about Apple or Microsoft, someone else will have found it as well. But in smaller, less liquid asset classes, the returns from surfacing relevant information are far less, so there are less analysts actively inserting information into assets, meaning that opportunities may well exist. This is because large, multibillion dollar funds simply cannot operationalize strategies trading in microcap assets.

This is simply to say that there are scale effects with efficiency. Bitcoin is not a microcap; it’s a globally traded traded asset worth over $100b. This ensures that there are high returns from surfacing relevant information and expressing it in the form of trades. Thus there is a significant disanalogy between the inefficient microcap altcoins (where returns from finding information are low, and markets are weak), and a mature asset with lots of analysts looking for an edge.

When small cap cryptoassets get 51% attacked or suffer bad news, they don’t decline. This demonstrates that crypto markets are not efficient

I’ll defer to Lo here (seriously — read Adaptive Markets!). The adaptive explanation would be that small cap assets are generally held by hardcore believers, or better yet, closely held by confederates of the founding team. In those conditions, cartel-like behavior can easily emerge. You have likely seen these conversations on Reddit and Telegram: coin owners urging each other not to sell, especially not in the presence of bad news, since the crypto community is briefly paying attention to the project. Renewed buying in the face of bad news is a way that issuers seek to blunt the effect of a negative catalyst. This only works in small markets were ownership is not widely distributed, though.

Also, it’s worth considering that virtually no one holds these assets because they like the underlying technology or find that particular flavor of code ripped off from Bitcoin Core or Ethereum that interesting. Small cap cryptoassets are held in expectation of a possible future pumps. Thus, impairments relating to the actual protocol itself are not the fundamental. The fundamental is the issuing team’s willingness to procure “adoption,” or at the very least, feign adoption by securing favorable press releases and partnerships. As long as the underlying protocol doesn’t totally dissolve, the ‘fundamental’ — the ability of the issuing team to create hype — can remain intact.

Since some bitcoiners mechanically buy Bitcoin on a regular basis (think: tithing) and less new supply will exist, this will mechanically cause appreciation

This is an example of first order thinking. The EMH lives on the second order. The key insight of the EMH, to me, is that any information you have, a sophisticated market participant also has. Since sophisticated market participants are strongly incentivized to find relevant information and trade against it, you can bet that they will have expressed that information the moment they acquired it. If this were indeed a plausible hypothesis (that static buying pressure would have a positive effect on price as issuance is cut in half), then these funds have already expressed this positive view in the form of a trade. This is what is meant by “priced in.” If something material is discovered to be due to happen tomorrow, it will be incorporated into price today. This is one of the most tricky features of the EMH, and it genuinely takes a bit of effort to get your head around it.

The question then becomes, not “is this information which, in a vacuum, would move the price?” but rather “do I have information which the smartest and best-resourced hedge fund analyst does not have?” If the answer is “no,” you can expect that this information is presently incorporated into price (to the extent that it is actually material information).

Why the focus on funds? The reason is that they are specialized firms which aggressively seek out information and express it in the form of trades. They are the entities which keep price in line with the “fundamental.” You need to recall that you are not operating in isolation. You are operating in the digital equivalent of a jungle with predators lurking around every corner. These predators are skilled, fast, and well resourced.

In equity markets, we’re talking about funds that have personal relationships with CEOs and CFOs, have dinner with them, and interpret whether they are optimistic about the next quarter. Funds that have dozens of analysts crunching datasets you weren’t even aware existed. They will track corporate private jet movements to suss out whether an acquisition is likely to take place. They will run a machine learning model to assess the emotional state of Jerome Powell from his eyebrow twitches as he announces Federal reserve actions. They will take satellite data imagery from parking lots to predict whether Walmart will beat quarterly earnings guidance. Public markets are incredibly competitive. They are where some of the most talented individuals make their careers, and there’s no real restriction on being able to act on information (outside of insider trading). Anyone who believes they have an edge is free to express their view in a trade.

So if you feel you have information which is market-relevant (like this expectation that a supply contraction would drive up the price), the most sophisticated participants have it too. And they’ve already evaluated it and acted on it.

Additionally, you need to recall that markets are not democratic. They are weighted by capital. A whale can express a far stronger opinion than a minnow. Hedge funds simply have more capital (and they tend to have access to cheaper leverage!). Then, when they develop a view on some stock, they have the means to express that view. This is how the “pricing in” takes place. Thus it’s really only price-setting entities that matter most of the time.

Plustoken amassing 200k BTC (~1% of supply) and selling it was a major driver of price action in 2019. Why wouldn’t the halving (affecting 1.8% of issuance) do the same?

First of all, the rise and fall of Plustoken wasn’t anticipated. It was genuinely new information — so much so that most investors only learned of the magnitude of the ponzi until after it was mostly done selling off. Also, as far as we can tell, the Plustoken BTC wallets were liquidated over a relatively short period; about 1–2 months far as I can tell. That’s a lot of BTC for any market to absorb. The change in issuance adds up to a decline in 1.8% annualized — but that’s annualized. What it means mechanically is that ~24,800 fewer BTC will be mined every month. That’s a large number, but it’s not the same as 200,000 BTC being liquidated in a short period. And, unlike Plustoken, the reduction is known well in advance.

The halving will affect Bitcoin from the demand side, by causing excitement among investors and getting press coverage. Thus the halving will still be a positive catalyst for Bitcoin

The same logic as found in the response directly above holds here. If you look at the Litecoin case study, the price was clearly bid up in anticipation of the halving, and then it collapsed after the halving itself. This may well have been a case of investors hoping that the halving would be a positive catalyst. You can see how investors positioning themselves (making bets on how they think other investors might react) affects price. You get into a recursive game where everyone is watching everyone else, and they all try and anticipate what the other is doing. Thus even if there is a highly-anticipated demand-side shock on the date of the halving (either through press coverage or simply investor ebullience), it will have been anticipated by a price setting entity and likely incorporated into price months prior.

If markets are efficient, there’s no point investing in Bitcoin

This isn’t the case at all. There are some informational facets of Bitcoin which are entirely known and transparent, like the supply schedule. However, as I mention above, a lot of the fundamental drivers of the Bitcoin price are not easily quantifiable or even knowable. No one quite knows how many Bitcoin owners there are worldwide, for instance. If you are able to forecast these factors better than others, you will be able to find an edge. Additionally, there are plenty of un-forecastable shocks which might have a positive effect on Bitcoin in the future, such as currency crises. Critics of the EMH fail to see that it only stipulates that markets express available information. Obviously, unknown future catalysts are not available. They haven’t happened yet.